Markets Embrace the Never-Ending Story

Iran tensions linger, but markets keep leaning bullish. Plus, the U.S. consumer is in much better shape than you've been told, Warsh states his case, and charting the S&P 500.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Tuesday afternoon, U.S. Vice President JD Vance announced that he and his delegation would not be travelling to Islamabad, Pakistan for a second round of peace negotiations with their counterparts from Iran. This came after the Tasnim News Agency, which is considered to be an arm of Iran's Revolutionary Guard, reported that Iranian leadership saw no prospect for continued negotiations with the U.S. due to Washington's "excessive demands" and would not attend the talks. It should be noted that both Washington and Tehran have accused each other of violating the still-in-effect ceasefire.

Financial markets reacted to this news Tuesday as one might have expected. Crude oil traded higher, Treasury debt securities traded lower, as did equities. However, markets did not react as sharply in a negative direction as they could have with markets near all-time highs after an incredible April to date. This, despite the fact that the U.S. is moving more resources into the region to include yet another carrier strike group.

President Trump posted to his Truth Social account...

"Based on the fact that the Government of Iran is seriously fractured, not unexpectedly so and, upon the request of Field Marshal Asim Munir, and Prime Minister Shehbaz Sharif, of Pakistan, we have been asked to hold our Attack on the Country of Iran until such time as their leaders and representatives can come up with a unified proposal. I have therefore directed our Military to continue the Blockade and, in all other respects, remain ready and able, and will therefore extend the Ceasefire until such time as their proposal is submitted, and discussions are concluded, one way or the other."

There we have it. Markets have reacted well to this particular news overnight. Equity index futures have rallied modestly through the zero-dark hours, as oil has come off of its overnight highs and Treasuries have come off of their lows. For nothing? Hard to say. Headline risk is what overhangs our marketplace at the moment.

Something close to a peace deal had been priced in over the past three-plus weeks. A failure to reach a deal and a continuance of hostilities would certainly leave markets in need of some nasty repricing. Yet, markets are embracing the "never-ending" story.

As long as it appears that President Trump wants this war to be over, markets seem to believe that it is over. That's where we are financially. In a good place. Corporate earnings are running hot. Profitability is not an issue. The economy, to include labor markets, is considerably stronger than many had expected. Still... we walk on eggshells.

Speaking of the Economy...

I did tell readers ahead of time that economists were starting to expect a Retail Sales report for the month of March that would surprise to the upside. Wow. That's the only word that comes to mind.

If Americans were supposedly pulling back on spending, they certainly have reversed course. First, for the month of February, the U.S. Census Bureau revised headline retail sales growth from January to +0.7% from +0.6%. At the core (ex-autos), February retail sales were revised to +0.7% from +0.5%.

For the month of March, headline retail sales were up 1.7% from those higher February numbers. Consensus had been for growth of 1.4% from the lower, unrevised numbers. At the core, March retail sales were up 1.9% from the higher February print versus expectations for growth of 1.3% from the lower numbers. If you were about to say that it was all due to the rise in gasoline prices, you would be partially but not completely correct. Gasoline sales, not adjusted for inflation, were up 15.5% on a month-over-month basis. No joke at all.

Still, furniture was red hot in March, with sales up 2.2%. Online retailers saw a 1% pop. Electronics sales were up 0.9%. The fun index (sporting goods, hobbies, music and books) was flat. That is true, but it came after a 2.6% pop for February from January.

Bottom line? The U.S. consumer is in much, much, much better shape than you have been told. Rumors of the demise of the U.S consumer have been greatly exaggerated.

Ice Cream Man

Well, I'm usually passin' by just about eleven o'clock

See I never stop, I'm usually passin' by

Just about eleven o'clock, listen here

And if you let me cool you one time

You'll be my regular stop

Alright (one, two, three)

I got bim bam banana pops, dixie cups

All flavors and push-ups, too

I'm your ice cream man

Stop me when I'm passin' by

They say all my flavors are guaranteed to satisfy

- John Brim (Van Halen), 1976

About the Fed

Former Fed Governor Kevin Warsh (President Trump's nominee to replace current Fed Chair Jerome Powell at the helm of the central bank when his term expires on May 15) appeared before the Senate Banking Committee on Tuesday. Warsh came off as confident, at least to this Fed watcher. He was clearly championed by the majority of Republican party senators on the committee and clearly demonized by the majority of Democratic party senators on the committee.

In the most important statement of the event, in discussing independence at the policy making level, Warsh said, "The president never asked me to predetermine, commit, fix or decide on any interest rate decision in any of our discussions. Nor would I ever agree to do so." When asked about President Trump's persistent calls for lower interest rates, Warsh added, "I've heard this view on interest rates, and it sounded very similar to every other president in economic history." My opinion, as a former titled economist at three investment banks/broker-dealers, is that Warsh's claim there is 100% accurate.

Warsh now needs several steps to be completed before he would be confirmed to the position of Fed Chair. Tim Scott of South Carolina, who heads the Banking Committee will set a date for the 24-member panel to vote on Warsh. Then his nomination will be taken up by the full Senate.

The catch is that Thom Tillis, a North Carolina Republican, has insisted that he will keep Warsh from progressing past the committee stage until the Trump administration's criminal probe into Jerome Powell for budget overruns, is dropped. Powell, who can remain on as a Fed Governor into 2028, has said that he believes that he can stay on the job as Fed Chair beyond May 15 if no individual is confirmed by the full Senate to replace him. Should be fun.

Sometimes...

... You realize while being dragged through disgusting, brown, brackish river water by a puncture-resistant raft with a muffled motor that you just swallowed something you probably shouldn't have. Ahh, the waiting. Such a blast.

Marketplace

Markets gave up on an early rally on Tuesday. Things got a little homely as the afternoon wore on, but never truly ugly. At the closing bell, the S&P 500 had given back 0.63% while the Nasdaq Composite had surrendered 0.59%. The small-caps were hit as well as the Russell 2000 backed up for a loss of an even 1%.

It wasn't all bad, despite a tough day for U.S. Treasuries and a rally across the oil patch. The Dow Transports rallied again for a gain of 2.62% as the short squeeze in Avis Budget (CAR) continued. That stock was up another 17.3%. The Philly Semiconductors also rallied, albeit for a gain of "just" 0.5%, led by Advanced Micro Devices (AMD) and Marvell Technology (MRVL) .

Breadth

Nine of the 11 S&P sector SPDR ETFs closed out the Tuesday session in the red, led lower by the REITs (XLRE) and the Utilities (XLU) . Five of these funds lost at least 1% during regular trading hours. The winners were led by Energy (XLE) for obvious reasons. Interestingly, both cyclical and growth sectors outperformed defensives despite the broad market weakness. It's almost as if portfolio managers knew that the president would slap a band-aid on the problem after the close.

Losers beat winners by a 5-to-2 margin at both the New York Stock Exchange and the Nasdaq. Advancing volume finally tumbled, taking just a 37.2% share of composite Nasdaq-listed trade and only a 30.3% share of composite NYSE-listed activity for the session. Aggregate trade was up sharply. Activity grew 11.1% on day-over-day basis across Nasdaq listings, and by 10.7% across NYSE listings. Volume also popped across the membership of the S&P 500.

Go ahead, ask your question...

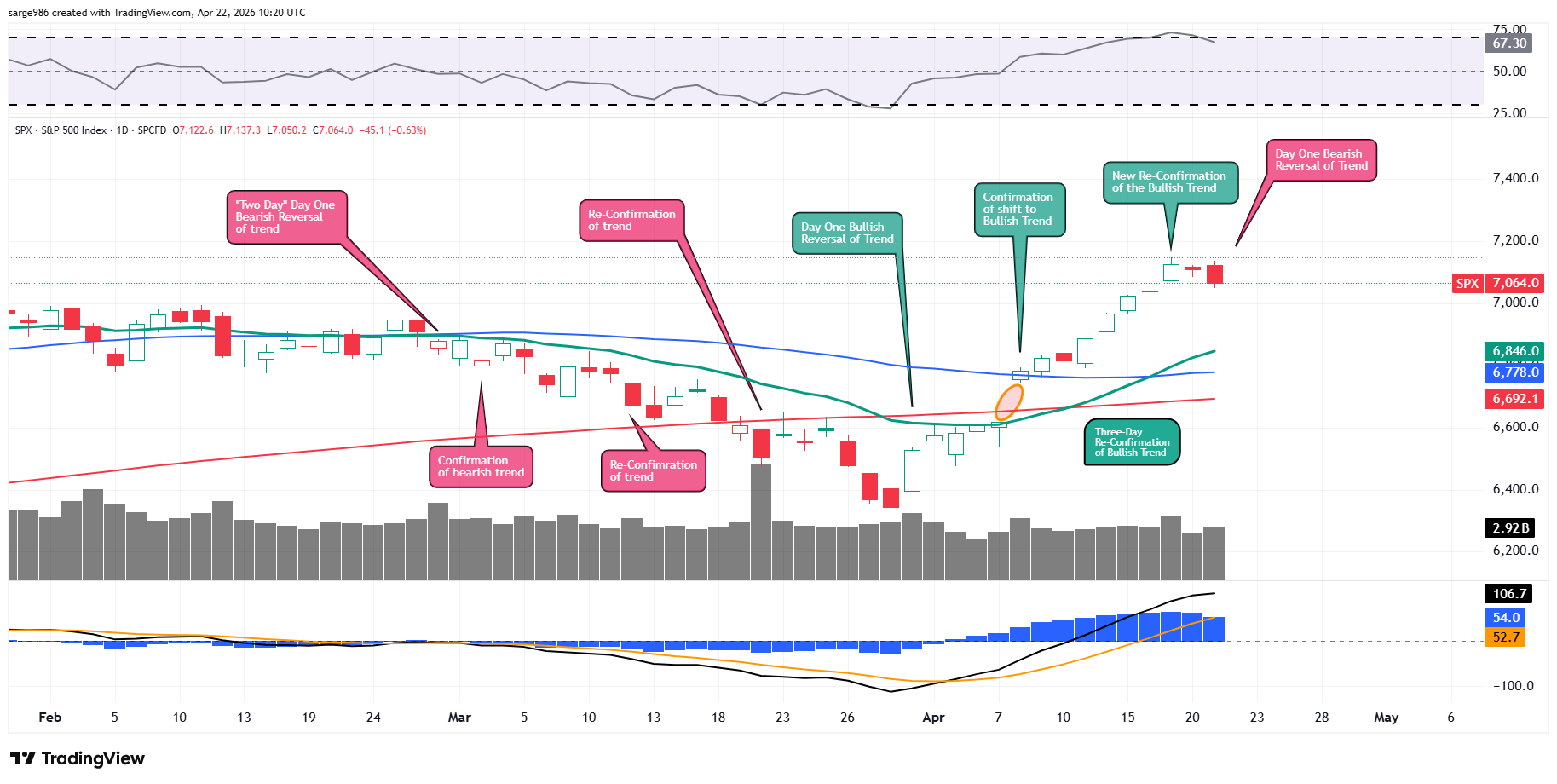

Readers will see that Tuesday does qualify as a "Day One" reversal of trend. The increased trading volume is there and now the bears look for a "pause" day or days.

The bright side for the bulls is that the trading volume reached on Tuesday was nowhere near the trading volume reached on Friday or on Wednesday, April 8, both "up" days. That could prove meaningful.

Relative Strength is now out of technically overbought territory, but still quite robust. The daily MACD is still set in rally-mode.

Economics (All Times Eastern)

07:00 - MBA 30 Year Mortgage Rate (Weekly): Last 6.42%.

07:00 - MBA Mortgage Applications (Weekly): Last 1.8% w/w.

10:30 - Oil Inventories (Weekly): Last -913K.

10:30 - Gasoline Stocks (Weekly): Last -6.328MM.

13:00 - Twenty-Year Bond Auction: $13B.

The Fed (All Times Eastern)

Fed Blackout Period.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: (T) (.55), (BA) (-.68), (GEV) (1.67)

After the Close: (CSX) (.39), (IBM) (1.81), (LRCX) (1.36), (NOW) (.97), (TSLA) (.36), (URI) (8.94)

Related: Asia's Worst Performer Slumps Again as MSCI Refuses to Remove Shackles

At the time of publication, Guilfoyle had no positions in any securities mentioned.