Growth Stocks Exist Outside of Tech. I'm Eyeing Two of Them Right Now

Technology is expected to be the big winner in 2026. But it's also pricey, so I've set my target on names like these.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Despite the continued effective closure of the Strait of Hormuz, the market delivered mostly gains last week. It was not a broad-based advance; the Dow was down for the week and small caps posted minor gains. Technology continued to be the straw that stirs the drink, with the Nasdaq sprinting ahead by just over 1.6% for the week. This performance was assisted by blowout quarterly results from Intel (INTC) and Texas Instruments (TXN) .

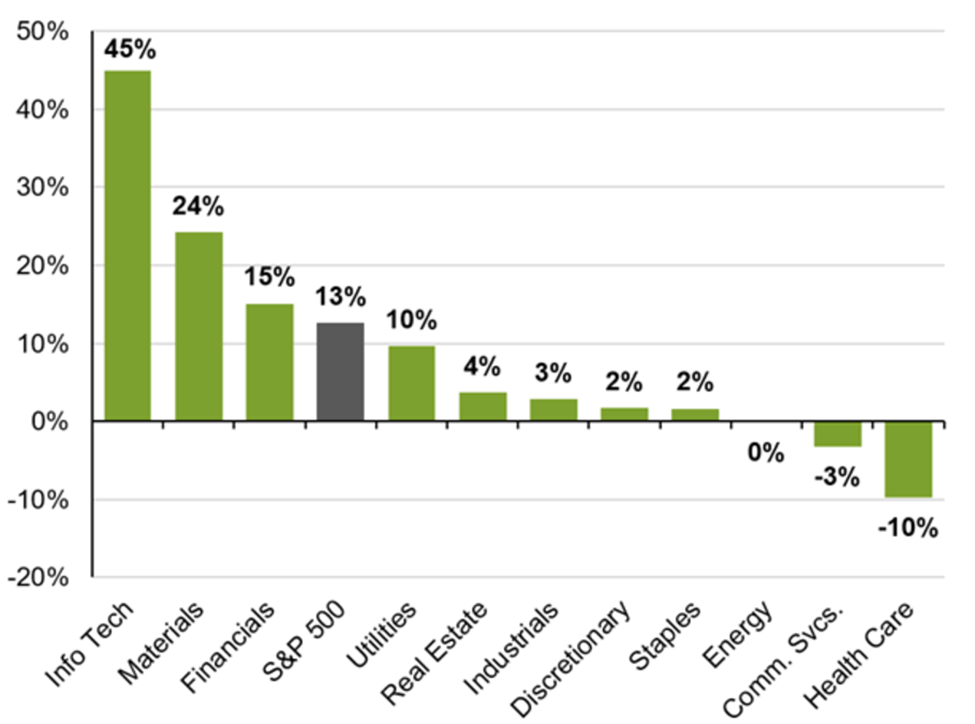

From 2023-2025, earnings growth from the Magnificent Seven averaged better than 20% annually. The S&P 493 struggled to deliver profit growth in the mid-single digits. This bifurcation has continued into 2026. Currently the S&P 500 is projected to produce over 16% year-over-year earnings growth this year. Taking just Micron (MU) and Nvidia Corporation (NVDA) out of the equation, and that estimated profit rise drops to under 10%. And if global supply chains don’t start to normalize in the weeks ahead, those projections could turn out to be too optimistic.

As you can see from the chart above, only five of the 11 S&P sectors are expected to produce 10% or better earnings growth this year. Technology is leading this charge. Six S&P sectors are expected to have five percent or lower growth in 2026. The problem is technology stocks have gotten expensive during the recent rebound. Philadelphia Semiconductor Index has been up for 18 straight sessions, the first time in history this has happened.

I continue to look for growth outside of technology. Instead, I'm looking where valuations are more reasonable. Here I'll tackle two growth-at-a-reasonable-price stocks I'm waiting to buy on the dips: Arcutis Biotherapeutics, Inc. (ARQT) and Chinese JD.com (JD) .

Related: Warsh Clears Hurdle, Earnings Bonanza Ahead, Econ Data Deluge

If we see Arcutis post a decent pull back, I'll be ready. The company’s pipeline-in-a-product, Zoryve, recently got approved for another indication (atopic dermatitis). Arcutis has rapid growth ahead of it with 30% or better sales growth penciled in over the next couple of years. Profits should come in roughly at 30 cents a year this year, but the analyst firm consensus sees earnings quadrupling in fiscal 2027 and hitting three bucks a share in fiscal 2030. The stock trades for just over $23 a share. Management believes Zoryve could see peak annual sales of between $2.6 billion to $3.5 billion. The stock’s market cap is just under $3 billion.

I will also be happy to boost my stake in Chinese JD.com via covered-call orders on any market pullbacks. The stock in this online marketplace and logistic company appear to have bottomed out and is gaining some momentum. Macquarie upgraded the stock two weeks ago on the company’s first-quarter outlook. Fund manager Michael Burry also recently added to his stake. The stock trades at just over $30 a share and the company is making a strong push into Europe. JD.Com should make just over three bucks a share in fiscal 2026, and the analyst consensus has over four bucks a share projected for fiscal 2027. Even with putting a sizable China discount on the stock, the equity appears more than reasonably valued.

At the time of publication, Jensen was long ARQT and JD.