Wall Street Sold IBM’s Guidance — I Bought the Stock

Big Blue's numbers beat expectations, even if guidance didn’t wow. Here's my price target and why I was comfortable going long.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Wednesday evening, IBM (IBM) released its first-quarter financial results. For the period ended March 31, the company posted adjusted EPS of $1.91 (GAAP EPS: $1.28) on revenue of $15.917 billion. These top-line and adjusted bottom-line results both beat Wall Street's expectations, while that sales print was good for year-over-year growth of 9.5%.

The shares are trading sharply lower Thursday. Why? The guidance issued did not blow Wall Street away. Perhaps they expected more. Perhaps IBM is managing expectations.

I initiated a long position in the name overnight. This is that story. Psst... I was okay with the guidance.

Arvind Krishna, chair, president and CEO of IBM, commented in the press release:

"The first quarter was a strong start to the year with broad-based revenue growth across our segments. These results reflect the integrated value of our portfolio and the trust clients put in us to improve their operations. As clients scale use cases, AI continues to be a tailwind for our global business. IBM products and services are helping clients orchestrate, deploy and govern AI across hybrid environments. Given this strong start, we continue to expect more than 5 percent constant currency revenue growth and an increase of about $1 billion in year-over-year free cash flow in 2026."

Operations

As revenue generation grew 9.5% to $15.917 billion, gross profit increased 11.4% to $8.95 billion on a gross margin that widened to 56.2% from 55.2%. After accounting for operating expenses, interest, other income & expenses and taxes, GAAP net income printed at $1.216 billion (+15.3%). This works out to $1.28 per fully diluted share versus $1.12 for the year-ago comparison. After adjustments made primarily for acquisition-related costs, fully diluted earnings per share improved to $1.91, up from $1.60 for the year-ago period.

Segment Performance

-- Software generated revenue of $7.1 billion (+11% or +8% in constant currency).

- Hybrid Cloud (Red Hat) - up 13%, or 10% in cc.

- Automation - up 10%, or 7% in cc.

- Data - up 19%, or 16% in cc.

- Transaction Processing - up 6%, or 2% in cc.

-- Consulting generated revenue of $5.3 billion (+4% or +1% in constant currency).

- Strategy and Technology - up 4%, or 1% in cc.

- Intelligent Operations - up 4%, or 1% in cc.

- Infrastructure generated revenue of $3.3 billion (+15% or +12% in constant currency).

- Hybrid Infrastructure - up 28%, or 25% in cc.

- IBM Z - up 51%, or 48% in cc.

- Distributed Infrastructure - up 17%, or 13% in cc.

- Infrastructure Support - down 2%, or 6% in cc.

Guidance

For the full year, IBM reiterated its outlook for constant currency revenue growth of 5%. This was taken poorly by the Street, but probably should not have been, in my opinion, as consensus view has been for headline revenue growth of close to 5.5%.

The company also reiterated its expectation for full-year free cash flow to increase by roughly $1 billion from the year-ago comparison. I'm cool with that too.

Fundamentals

For the period reported, IBM generated operating cash flow of $5.169 billion. Out of that came $2.565 billion in a change in financing receivables and $384 million in capex spending. This still left free cash flow of $2.22 billion, which was up from $1.962 billion (+13.2%) from the year-ago comp. Out of that number, it paid out $1.576 billion in cash dividends to shareholders. IBM did increase its quarterly dividend Wednesday night to $1.69 from $1.68 for a forward yield of 2.68%.

Turning to the balance sheet, IBM ended the quarter with a cash position of $11.828 billion and inventories of $1.476 billion. That put current assets at $31.914 billion. Current liabilities add up to $40.101 billion. That looks wonky only because of that number, $17.034 billion is labeled as deferred revenue, which is not a true financial obligation. That said, there is short-term debt of $8.655 billion, which I do not love.

IBM's current ratio stands at 0.79. Once adjusted for those deferred revenues, this ratio rises to 1.38, which, while not awesome, does pass muster.

Total assets amount to $156.229 billion. This includes $89.333 billion in "goodwill" and other intangibles. I will openly admit that labeling 57% of any company's assets as intangible is rarely a good thing.

Total liabilities less equity comes to $123.174 billion. This includes another $4.195 billion in deferred revenue, but also $57.706 billion in long-term debt, which really weakens this balance sheet if you ask me.

My Opinion

The quarter was solid. Cash flows are strong. The guidance was better than it was made out to be. I do not love the balance sheet, but with cash flows like that, that are growing, this can be addressed if the CEO has the will.

I am a little bit excited to initiate the name on this spate of weakness.

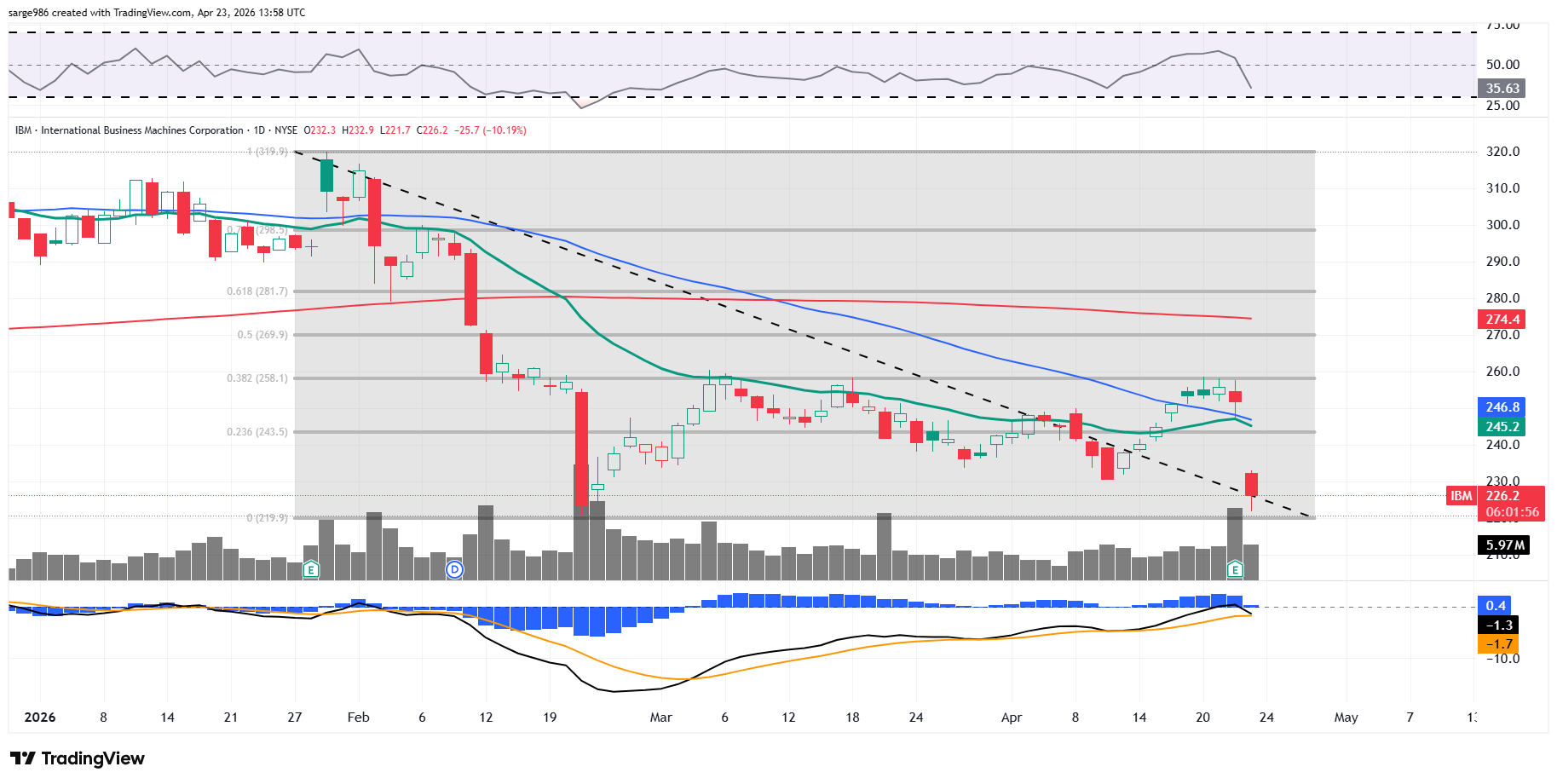

Look at this daily chart of IBM. Readers will see the selloff that ran from late January into late February. Then readers will see the stiff resistance posed by the 38.2% Fibonacci retracement level of every attempted rally since.

The stock has lost its 50-day simple moving average (SMA) and 21-day exponential moving average (EMA) Thursday morning. The rout was accelerated by portfolio managers reducing exposure in response to that lost line. Now, there's a real chance for something constructive to happen.

Watch this...

Not that I know this will continue to develop, but IBM is now in position to create what would be a Double Bottom pattern of bullish reversal with that same Fib level as pivot. I am a buyer down to $220.

Pivot: $258

Price Target: $296

Related: Bitcoin Found Its Floor. Now It’s Hunting for a Ceiling.

At the time of publication, Guilfoyle was long IBM equity.