Digging into the Market’s Renewed Volatility

Aspects of May inflation data may surprise to the upside this week, and what that could mean for the Fed.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

In last Friday’s Weekly Roundup, we shared the following with you:

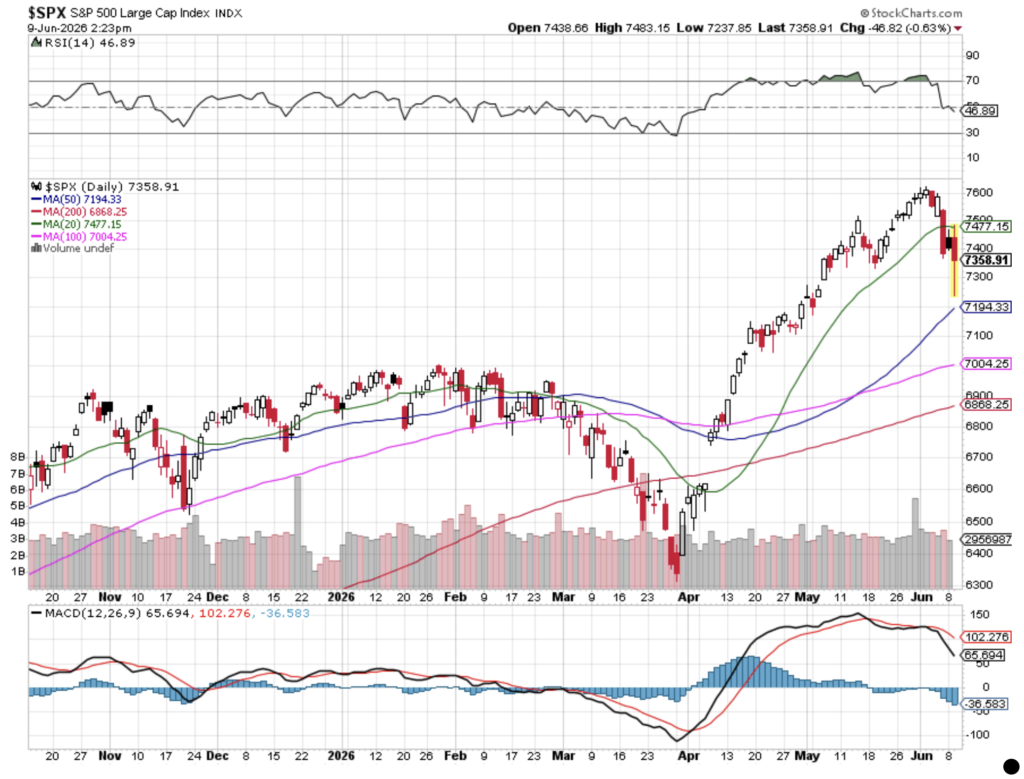

“When trading begins next week, we’ll be looking to see if support for the S&P 500 at its 20-day moving average holds. If not, the next layer of support clocks in near 7157, roughly 3%-4% lower. While that may sound painful, it would be a small decline relative to the current year-to-date performance for the S&P 500. Let’s also remember that on average, the S&P 500 experiences three to four pullbacks of 5% or more each year. Sometimes the reminder of that can be a hard pill to swallow, especially on the back of nine consecutive weeks of gains.“

As we can see in the chart below, the S&P 500 moved past its 20-day moving average with Tuesday’s slide putting the index near its 50-day moving average before recovering some of that lost ground.

Looking past those moving averages, when we look at the MACD indicator for the S&P 500, we wanted to get Bob Lang’s take, and this is what he shared:

“The MACD rolled over recently, just last week, as the relative strength is testing levels not seen since early April. Intraday, there was an extreme low reading in the S&P 500 down towards the lows from early May, not quite to the 50 MA, but the gap from May 6 was filled today. If there is a strong rally on Wednesday, then this move (reversal back up) today could be considered a good test of lower levels, with dip buyers picking up the pieces.“

We’ll keep that in mind as we get ready for Wednesday’s May CPI report and the May PPI report on Thursday. Given the comments collected in recent ISM PMI reports, our focus will be slanted more toward the PPI report given the leading relationship with the CPI but also given our concern for margin and EPS expectations for 2H 2026.

In our opening comments on Tuesday morning, we flagged that gas prices were still up more than 30% on a year-over-year basis despite the drop over the last 30-days reported by AAA. But ahead of the May CPI report on Wednesday, we wanted to make sure we have an apples to apples, or May 2026 to May 2025, comparison.

With that in mind, we went to the U.S. Energy Information Administration’s website and pulled the weekly data. What we found was that U.S. regular conventional retail gas prices (dollars per gallon) were:

May 2025: $3.02

February 2026: $2.93

March 2026: $3.48

April 2026: $3.94

May 2026: $4.29

Doing some quick math, we find May 2026 gas prices were up 42% year over year, and almost 9% compared to April and more than 50% compared to February. That alone explains the pricing action we’ve been reading in the monthly PMI reports but then, add in the flow through to other petrochemicals and current supply chain disruptions, and it brings support for the comments we shared with you on Tuesday morning from BASF CEO Markus Kamieth. It also supports our questions about 2H 2026 EPS expectations for the S&P 500.

Great Chris, but where are we going with this?

Good question!

While the market expects the year-over-year figures for headline and core CPI in May to be higher than those for April, on a sequential basis, the consensus sees the headline line print falling to 0.5% from 0.6% in April. For the core CPI, the May figure is expected to inch lower to 0.3% on a sequential basis, down from 0.4% in April.

But doesn’t the core CPI exclude food and energy?

It does, but as we all know, the average person doesn’t escape higher food and energy prices.

The message is that we could see some of the May CPI data come in warmer than expected. Following last Friday’s stronger-than-expected May Employment Report, that would be another indication that we’re likely to get more hawkish rhetoric from the Fed after its next policy meeting, even if it is the first one under new Fed Chair Kevin Warsh. If the May PPI reports bring another headline figure above 6%, the odds of that hawkish rhetoric will be even higher.

Now, this is where it gets a little tricky. The CME FedWatch Tool already shows that the market isn’t expecting a rate cut between now and the first half of 2027, which is as far out as the model currently goes. But it does show a greater probability of a 25-basis point rate hike at the end of this year than keeping the Fed funds rate at current levels.

Why tricky? Because we market watchers are seeing this, but as we’ve seen many times in the past, just because we see something doesn’t mean the herd is.

While we picked up more shares of Broadcom (AVGO) and Netflix (NFLX) on Tuesday, we have our updated set of pickup points that we shared on Monday. If you reviewed those levels, then you know Costco (COST) and Palantir (PLTR) shares are hitting those levels on Tuesday.

Should the market sell-off continue or accelerate, we’ll keep an eye on those levels and another on the technical conditions for the S&P 500. With about 9.6% of the Portfolio’s assets in cash, we have ample funds to make some moves if the opportunity presents itself and the conditions are right.

More Pro Portfolio

- Trimming This Financial Holding After Price Target Boost

- We’re Tracking 30 Signals Across 9 of Our Pro Portfolio Investing Themes

- Weekly Roundup: How We’re Navigating the Fed’s Hawkish Pivot and Iran Risk

At the time of publication, TheStreet Pro Portfolio was long AVGO, COST, NFLX and PLTR.