Market Horrors: Nasty Tuesday Trading, Scary May Prices, Threatening Trump

Let’s check the nastiest day of the 3-day selloff, May inflation outlook, Trump’s Iran threats and … Nvidia earnings.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Hide and Seek

Haven’t found anyone

From the old gang.

They must be still in hiding,

Holding their breaths

And trying not to laugh.

Our street is down on its luck

With windows broken

Where on summer nights

One heard couples arguing,

Or saw them dancing to the radio.

– Charles Simic (2018)

Seeking Refuge?

Domestic equity markets have struggled for three days now. Without emitting overtly bearish signals that might foretell the very next step. Treasuries have continued to have been sold by bond traders, forcing yields and subsequently, interest rates higher. This is a reflexive and hopefully not lasting response to the warm April consumer price index print and the white-hot April producer price index print that crossed the tape last week. For those watching this data closely, May looms as quite scary. For May, the Cleveland Fed’s model shows year-over-year CPI growth of 4.18%. That would be a sharp acceleration from the 3.7% pace of April. The Hedgeye shows a base case for May even hotter than that.

So where does this market, still trading close enough to all-time highs, seek refuge? I think it quite obvious that a great deal of hope has been placed in this afternoon’s scheduled quarterly earnings release by tech giant and elite level chip designer Nvidia (NVDA). Markets see those results as a potential upside-catalyst. That said, nothing will permit these markets to make another attempt at getting back “on trend” should interest rates continue to push higher. Higher rates will suck the life out of economic activity, demand for labor, the housing market, and corporate profitability.

Corralling this reflexive response to inflationary pressures will be tricky. For, the entire ball of wax boils down to the market price for front-month crude. Markets seem to care not that these surging prices are the result of a supply shock. I think that matters, but markets are somewhat rattled. A supply shock should be rather simple to unwind, unless the infrastructure and methods of transportation supporting a return to normalcy are no longer in place or difficult to restore to conditions of normalcy. That brings us directly to the Strait of Hormuz.

On Tuesday…

U.S. Pres. Donald Trump threatened to resume military strikes against Iran in the days ahead should a deal with that nation continue to be elusive. The president told the media, “I hope we don’t have to do the war, but we may have to give them another big hit.” The president added, “Well, I mean, I’m saying two or three days, maybe Friday, Saturday, Sunday. Something maybe early next week — a limited period of time.”

In The Meantime…

The U.S. Senate signaled growing opposition to continuing the war in Iran in a procedural vote on Tuesday. The senior U.S. legislative body voted 50-to-47 for a war powers resolution that would call for an end to any hostilities. Four Republican senators crossed party lines on this non-binding vote and three other Republican senators abstained.

Even if such a resolution were to pass in the Senate in a binding vote, that does not necessarily mean that military operations in Iran’s neighborhood would automatically cease. The resolution would then have to pass in the House as well, which is also led by a small margin, by Republicans. It would then go to the president for an autograph. One could easily imagine that Pres. Trump, if the resolution did get that far, would veto any resolution limiting his own powers.

Send in the Clowns

On that note, NATO is, according to Bloomberg News, discussing the possibility of aiding ships passing through the Strait of Hormuz if that maritime passage is not reopened by early July. This idea, supposedly, does not yet have the full support of the military alliance, which will meet in Ankara, Turkey on July 7 and 8 Sarge’s translation: “Though our nations would benefit greatly from any reopening of the Strait and our nations also benefit greatly with Iran’s nuclear threat having been removed, we would prefer to let the U.S. Navy continue to take on nearly all of the risk. Once we think it’s safe, we will consider sending naval assets to help.” Isn’t NATO just adorable? With friends like this…

Markets

In my opinion, Tuesday was the nastiest day so far of this now three-day long selloff. By day’s end, the U.S. Ten-Year Note paid 4.66% (up seven-basis points), while the U.S. Thirty-Year bond paid 5.18% (up five basis points. During the regular session, the yields for U.S. Ten- and Thirty-year paper ticked above 4.68% and just below 5.2% respectively. These yields have worked their way slightly lower overnight.

WTI Crude traded just below $109 per barrel at its Tuesday highs. Overnight, that price has dropped sharply. I see the sweet stuff trading with a $102 handle overnight. This has pushed US equity index futures into the green early on.

On Tuesday, the S&P 500 gave up 0.67% as the Nasdaq Composite surrendered 0.84%. The small- to mid-cap indices all lost between 0.94% and 1.01% for the Tuesday session while the Dow Transports backed up 0.28%, but the Philly Semiconductors stabilized (+0.03%).

Breadth

Five of the eleven S&P sector SPDR ETFs closed for the day on Tuesday in the green. That doesn’t sound too bad until one realized that the five were led by Energy (XLE). Then came the four defensive sectors, which outperformed both growth and cyclicals. This could be a warning that inflation is about to leave more than a mark on the U.S. economy. Within Tech (XLK), which was down 0.64% for the day, the Dow Jones U.S. Software Index gave back 1.25% offsetting that stabilization in the semiconductor space. The semis were paced by a 4.34% gain made by Marvell Technology (MRVL) and a 2.52% run made by Micron (MU).

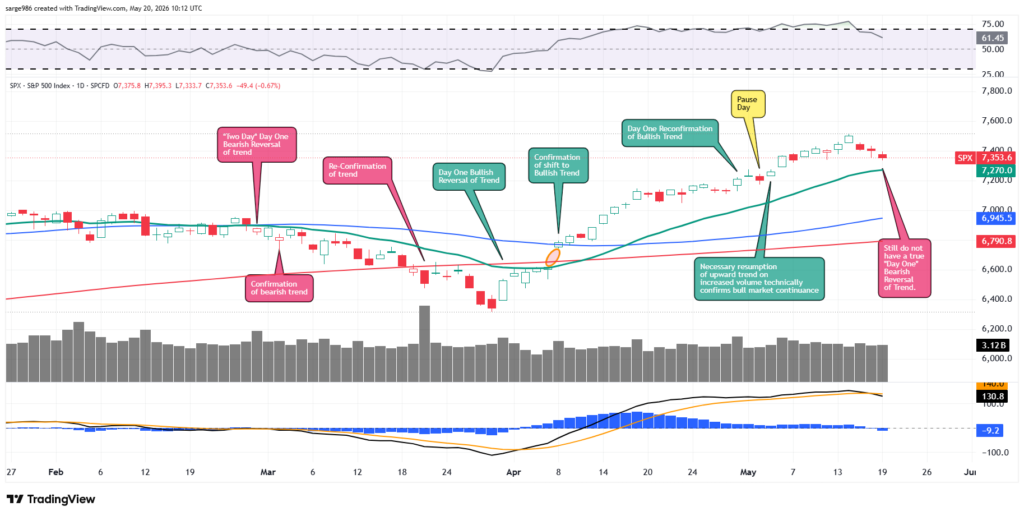

Losers beat winners by a five-to-two margin at the NYSE and by slightly better than a two-to-one margin at the Nasdaq. Advancing volume took a 32.6% share of composite NYSE-listed trade and a 39.3% share of composite Nasdaq-listed activity. So, was Tuesday, finally a “Day One” change in trend? Nope. Still no overt signal. That does not mean that we do not have a selloff. You know that we do. It means that we cannot confirm a change in trend using technical analysis.

Aggregate trading volume dropped by 4.2% on a day-over-day basis across Nasdaq-listed securities and contracted by 0.9% across NYSE-listings. Volume tailed off across the membership of the S & P 500 as well.

The daily moving average convergence divergence for the S&P 500 is the indicator to watch right now. Within this indicator, the 26-day exponential moving average has just been crossed to the downside by the 12-day EMA. That’s only mildly bearish with both of those lines running above the zero-bound. In addition, the histogram of the 9-day EMA has now crossed below that zero-bound. This is concerning for the short term but would not be the end of the world if that average can stay close to that level.

On Monetary Policy…

On Tuesday, in an interview with the Washington Examiner, Pres. Trump commented on incoming Fed Chair Kevin Warsh. In response to a question concerning whether Warsh will cut short-term interest rates any time soon, the president said, “I’m going to let him do what he wants to do. He’s a very talented guy. He’s going to be fine; he’s going to do a good job.”

Sarge’s translation: The president likely understands that rates will not be cut with both consumer- and producer-level inflation still accelerating to the upside. He probably also understands that Warsh will be but one vote among 12 at the Federal Open Market Committee and even as chair, he would lose credibility instantly if pushing for something quickly that conventional economists would see as inappropriate. He has to let Warsh find his footing early on, especially given that those members of the FOMC seen as Trump allies are badly outnumbered on this committee.

In Other News

It looks as if SpaceX has selected Goldman Sachs (GS) as the lead banker for its upcoming IPO. SpaceX could potentially make its prospectus public as soon as today after having filed with the Securities and Exchange Commission last month. SpaceX was recently valued at $1.25 trillion by its founder Elon Musk when he merged the company with his artificial intelligence company, xAI.

While Goldman will now very likely run the book on this deal, other bankers involved will include, possibly in order of prominence, Bank of America (BAC), Citigroup (C) and JP Morgan Chase (JPM). I’m just glad my days of being involved in IPOs have passed. A deal like this will definitely get you paid, but the stress would be off the charts.

Economics

(All Times Eastern)

07:00 – MBA 30 Year Mortgage Rate (Weekly): Last 6.46%.

07:00 – MBA Mortgage Applications (Weekly): Last 1.7% w/w.

10:30 – Oil Inventories (Weekly): Last -4.306M.

10:30 – Gasoline Stocks (Weekly): Last -4.084M.

1:00 p.m. – Twenty-Year Bond Auction: $16B.

The Fed

(All Times Eastern)

08:00 – Speaker: Philadelphia Fed Pres. Anna Paulson.

10:15 – Speaker: Reserve Board Gov. Michael Barr.

2:00 p.m. – FOMC Minutes.

Today’s Earnings Highlights

(Consensus EPS Expectations)

Before the Open: HAS (1.26), LOW (2.97), TGT (1.44), TJX (1.01)

After the Close: NVDA (1.78), URBN (1.14)

At the time of publication, Guilfoyle was long TJX, NVDA, MU equity.