Why I Bought This Land Name With the Specter of Stagflation Ahead

January CPI and PPI readings this week showed inflation is becoming somewhat intractable.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The markets have held up remarkably well this week.

The tariff wars continue to seemingly escalate. More importantly, inflation is becoming more and more intractable, putting future cuts to the fed funds rate on hold. Wednesday’s January CPI reading came in significantly hotter than expected and triggered a 10 BPS rise in the yield on the 10-year treasury during the day. What is as concerning to me is that Bureau of Labor Statistics (BLS) consistently understates the true rate of inflation — unless one believes its calculation that healthcare costs have fallen 15% over the past half decade, along with a slew of other "hedonic" adjustments the government agency employs within its models. However, markets managed to close Wednesday with little damage to the major indexes.

The January PPI report came out Thursday before the opening bell. Core year-over-year PPI printed a 3.6% readout, slightly over the consensus. However, the yield on the 10-year treasury gave back its 10 BPS gain from Wednesday and average mortgage rates for the week of February 13 were at their lowest levels of 2025 to date. Equities rallied strongly with the NASDAQ leading the way, climbing 1.5% on the day.

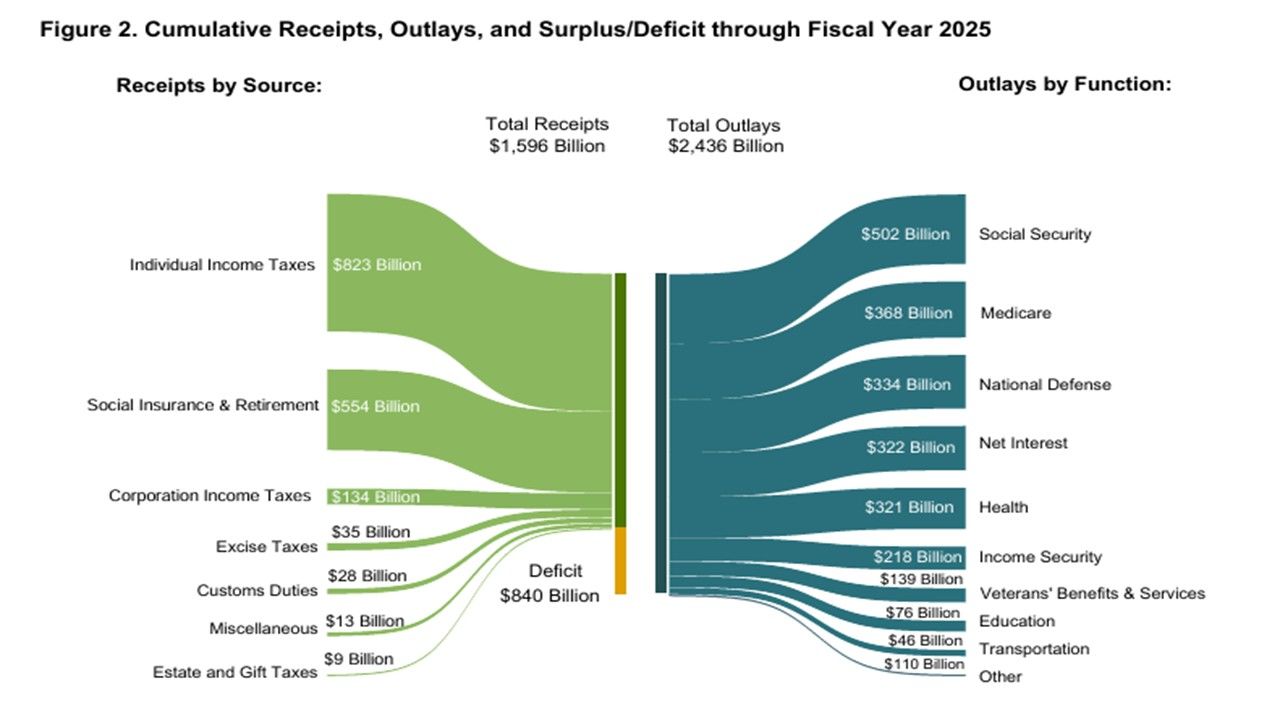

One reading that came out earlier this week that was all but ignored by the markets was the January budget deficit. Once again, it came in higher than expected. So far in the first four months of the federal government’s fiscal 2025 year, the fiscal deficit stands at nearly $840 billion. Far above the $531 billion deficit over the same period in fiscal 2024. Government spending is rising in the low teens on a year-over-year basis, which remains a headwind for bringing down inflation further.

More concerningly, government revenues are slightly down from the same period a year ago through the first third of the fiscal year. This should not be happening in an economy that is expanding. This tells me the economy is weakening. This is also confirmed from the recent downward revision on the initial read of fourth quarter GDP growth as well as last Friday’s miss within the January BLS jobs report. And stubborn inflation combined with weakening economic growth points to the specter of stagflation, which appears to be becoming a more and more likely economic scenario.

I don’t think the overall market is properly pricing in the likelihood of that economic backdrop. Hard assets, it should be noted, will likely outperform during a stagflationary environment. Indeed, gold prices have made a nice move up here in the first half of February. That has pushed the gold-related stocks in my portfolio, like Barrick Gold Corporation GOLD and Newmont Corporation NEM, higher over the past few weeks after I added to my holdings in both names via covered call orders early this year.

I have also recently established a position once again in the The St. Joe Company JOE. I am not a big fan of the housing sector here. However, the huge acreage of land the company controls in northwestern Florida is undervalued. The stock is also a nice proxy on the continued migration into the Sunshine State as well.

At the time of publication, Jensen was long GOLD, JOE and NEM.