Where to Buy Meta After Blowout Earnings Turn Heads on Wall Street

The big tech firm posted an excellent quarter where everything worked to near perfection and there's a chance for traders to profit.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Wednesday afternoon, Meta Platforms META released the firm's first quarter financial results.

For the three-month period ended March 31, Meta Platforms posted a GAAP EPS of $6.43 on revenue of $42.314 billion. While the top-line print was good for year-over-year growth of 16.1%, both of these numbers simply crushed Wall Street's expectations coming in. The EPS print beat consensus, while the revenue print beat by almost $1 billion.

Family (of apps) daily active people (DAP) was up 6% to $3.43 billion, which is truly impressive given the saturation of the social media marketplace. Ad impressions across the family of apps were up 5% year over year, while average price per ad was up 10%.

Meta Operations Up Sharply

As revenue generation popped 16.1% to $42.314 billion, costs and expenses increased 9% to $24.759 billion. This left a GAAP operating income of $17.555 billion (+27%), as operating margin improved from 38% to 41%. After accounting for interest, taxes and other income and expenses, GAAP net income increased a stunning 35% to $16.644 billion. This works out to EPS of $6.43, up sharply from the year-ago comp of $4.71.

Meta Segment Performance Detailed

- Family of Apps: drove revenue of $41.902 billion (+16.1%), producing an operating income of $21.763 billion (+23.2%). This easily beat expectations for both sales and profitability.

- Reality Labs: drove revenue of $412 million (-6.4%), producing an operating income/loss of -$4.21 billion (-9.5%). This sales print fell short of the mark, but the loss was far smaller than feared.

Meta Sales by Region

- U.S. and Canada: generated revenue of $18.259 billion (+18.2%), easily beating expectations

- Europe: generated revenue of $9.527 billion (+14.4%), narrowly missing expectations

- Asia-Pacific: generated revenue of $8.224 billion (+12.1%), narrowly missing expectations.

- Rest of the World: generated revenue of $5.382 billion (+19.1%), narrowly missing expectations.

Meta Stock Fundamentals

For the period reported, the firm generated operating cash flow of $24.026 (+24.6%). Out of this number came capex spending of $12.941 billion and payments on the principal of finance leases of $751 million. These two items combined were up 103.9%, which bodes very well for AI-infrastructure providers such as Nvidia NVDA. That left free cash flow of $10.334 billion. The free cash flow print was down 17.5% year over year due to the increased capex spending but managed to crush expectations.

Turning to the balance sheet, Meta Platforms ended the quarter with a cash position of $70.23 billion and current assets of $90.227 billion. Current liabilities added up to $33.89 billion, which included no short-term debt. This put the firm's current ratio at a very healthy 2.66.

Total assets amount to $280.213 billion, which includes goodwill of just $14.092 billion and no other intangibles. That's impressive. Total liabilities less equity comes to $95.184 billion including long-term debt of $28.829 billion. This is something that the firm could handle a rough 2.5 times over, out of pocket. This is one heck of a strong balance sheet.

Meta Post-Earnings Guidance

The firm projected second (current) quarter revenue of $42.5 billion to $45.5 billion, matching Wall Street's expectations at the midpoint. What I found interesting was the firm's increase in their full-year outlook for capex spending from $60 billion to $65 billion, to $64 billion to $72 billion. This reflects an increased commitment to staying with the firm's strategy in developing its generative AI programs and has to be considered a positive for high-end chip designers like Nvidia NVDA and Advanced Micro Devices AMD.

Wall Street's Outlook on Meta

Since these earnings were released, I have come across 17 highly-rated (four-plus stars at TipRanks) that have opined on META.

All 17 rate META as a "buy" or their firm's buy-equivalent rating. Two of these analysts did not set target prices. Of the remaining 15, after allowing for changes, the average target price is $667.93 with a high of $750 (Andrew Boone of JMP Securities) and a low of $600 (Brent Thill of Jefferies).

Once omitting these two as possible outliers, the average target drops very slightly to $667.62.

My Plan on Meta After Blowout Quarter

This was an excellent quarter for Meta. In fact, this was a blowout quarter where everything worked almost to perfection. Did I miss the boat on getting long this name? Maybe. The guidance is impressive as are cash flows and the balanced sheet. Let's take a look at the charts:

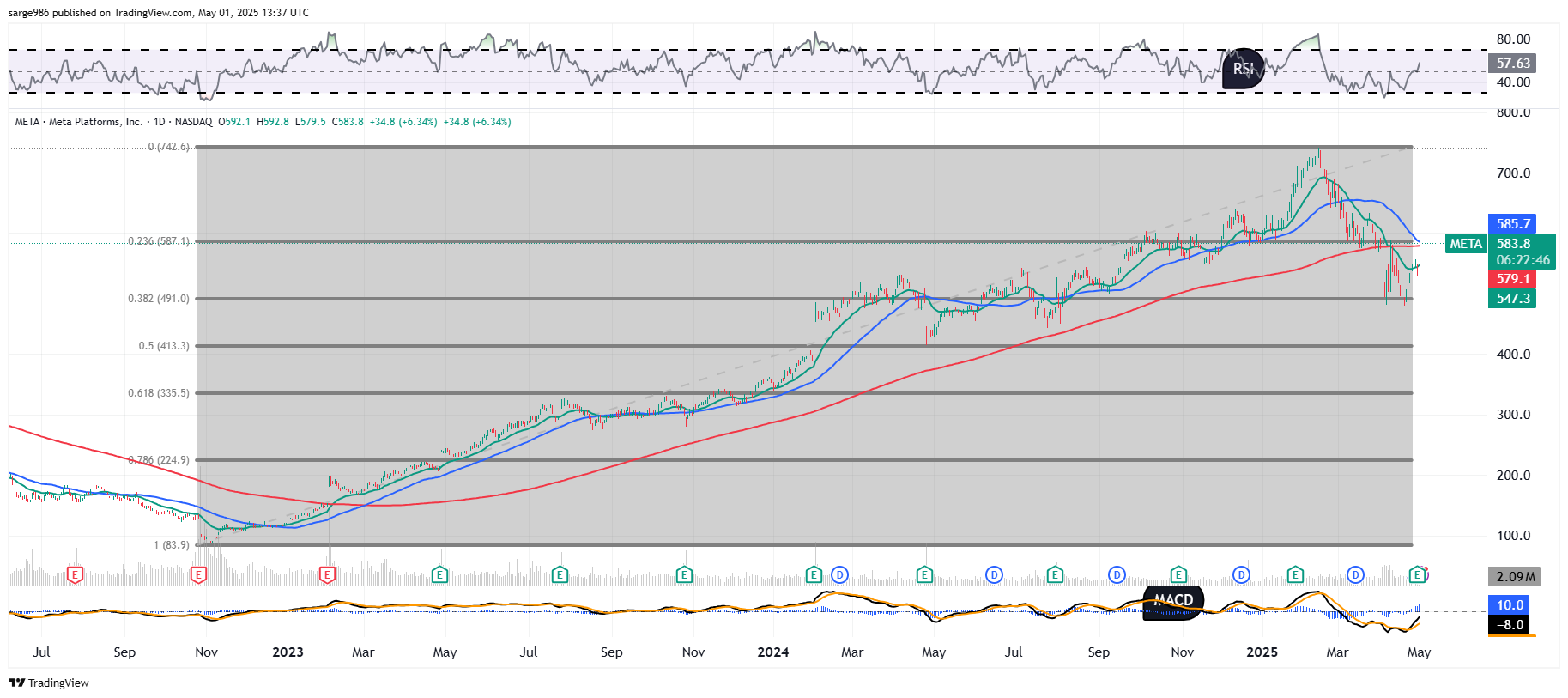

Just look at that support that showed up at the 38.2% Fibonacci retracement level of the late 2022 through early 2025 rally. That, too, is impressive and was our first clue to get long the equity on that dip, which I missed. Now, let's zoom into 2025:

Readers should note that META is breaking out from a double-bottom pattern with a $588 pivot. On Wednesday morning, the stock is trying to take on that pivot point as well as both its 200-day and 50-day SMAs. Should META close above all three of these levels that span from $576 to $588, there will be a rush among portfolio managers to increase exposure to the stock.

What I think I'll do is initiate should the shares fail here and retreat to their 21-day EMA, or purchase some on momentum with the crowd when those levels hold. Nothing in between.

The purchase below would be more of an investment. If I end up buying it with the crowd, it would be a trade, and my intent would be to puke the shares out to the stragglers. Kind of what the algos try to do to us every day.

At the time of publication, Guilfoyle had no positions in any securities mentioned.