Where I'm Buying UnitedHealth After Trump Admin's $700 Million Gut Punch

Here's how I view the healthcare giant after a big disruption to Medicare.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Monday evening, the Trump administration proposed sharply reducing the annual increase in federal payments to Medicare insurers. The government suggested an increase to certain insurers that would amount to a dollar amount of about $700 million, or 0.09%. This would be for 2027. For 2026, federal payments to insurers that offer Medicare advantage or gap plans increased by 5% from 2025 for a dollar amount increase of $25 billion.

A similar increase had been priced in by Wall Street for 2027 and has been quickly priced out overnight. As I type, UnitedHealth Group (UNH) and Humana (HUM) are both down more than 16%, CVS Health (CVS) is down a rough 10% and Elevance Health (ELV) is trading more than 7% lower. In full disclosure, I have been buying UNH ahead of the U.S. open as close to the lows as I can, most likely for day trade, but I'm willing to play the game longer than that if need be.

The proposal is not final and will likely be altered in some way by this autumn, so there's a lot of time to go on this story. That said, of these names, UnitedHealth reported the firm's fourth quarter earnings on Tuesday morning. For the period, which ended December 31, 2025, UNH posted an adjusted EPS of $2.11 (GAAP EPS: $0.01) on revenue of $113.215 billion. While that sales growth was good enough for year-over-year growth of 12.3%, the number did fall just short of Wall Street's expectations. The adjusted earnings print just barely met what the pros were looking for.

The GAAP print? Egads. Wall Street did not expect that.

There's more than anyone could even think of shaking a stick at on the "reconciliation of data" page. From $2.77 per share in restructuring costs to $1.48 per share in adjusted tax effects to $0.88 due to cyber attacks, to $0.49 per share in net portfolio divestitures, to $0.42 per share in intangible amortization. Oh, yeah, I trust that number about as far as I can throw the baseplate for an 81-mm mortar (the Vietnam War era baseplate, not that frisbee that they use now).

Either way, $2.11 compares poorly to the year-ago comp of $6.81 and $0.01 compares poorly to the year-ago comp of $5.98.

Guidance Was Weak, Too!

For the fiscal year just started, UnitedHealth projected revenue of greater than $439 billion and operating earnings of more than $39 billion. Consensus had been for about $456 billion worth of revenue, so that was a nasty miss. The firm also sees adjusted earnings per share of more than $17.75 with Wall Street looking for $17.76. So, that number is not so bad, but it certainly did not blow anyone away.

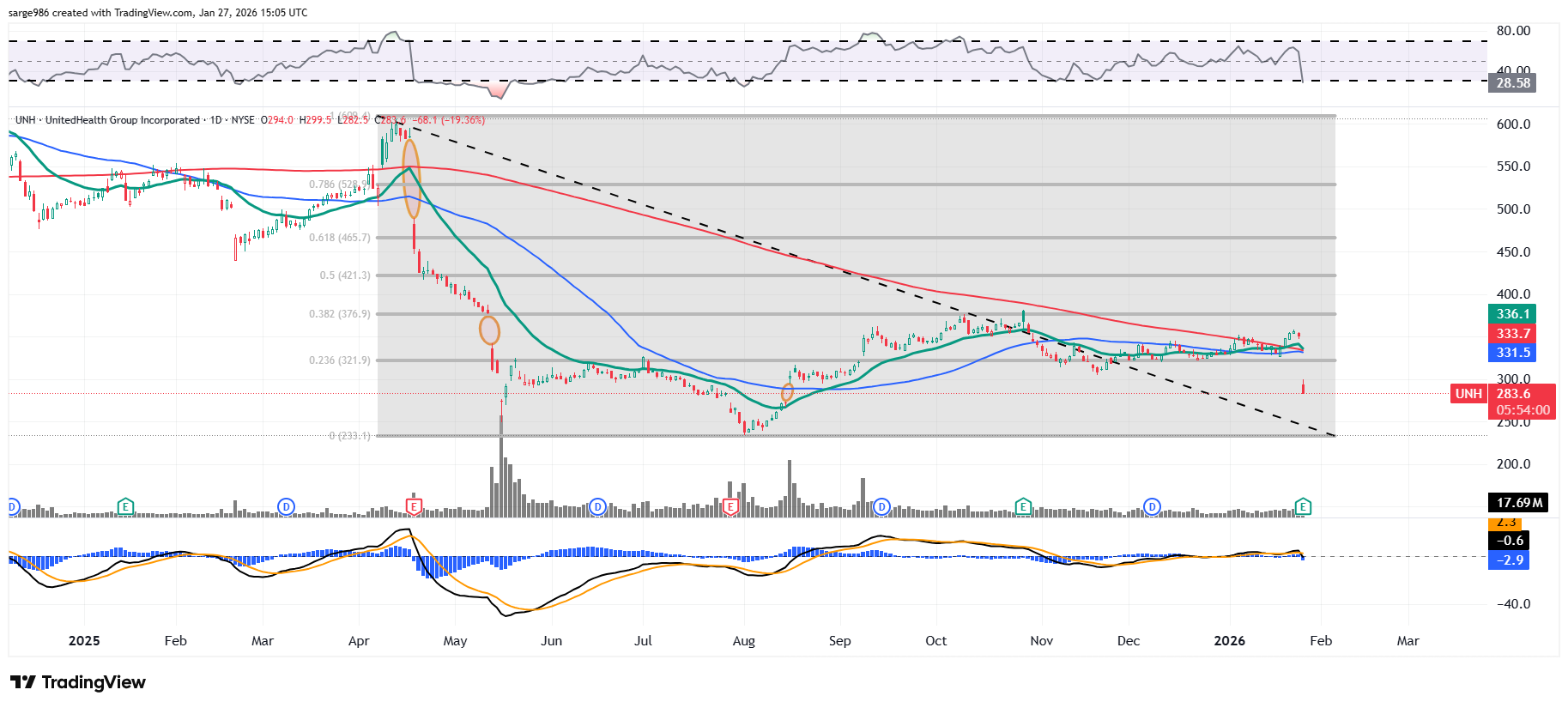

The Chart

Readers will see that, in late October, the advance of UNH shares were halted at a rough 38.2% Fibonacci retracement of the April through early August sell off.

From September up until Monday, the shares had found support at the 23.6% Fib retracement level of that same sell-off. Now, with the share price in free fall, we look to the small unfilled gap that had been left behind in mid-August.

Do unfilled gaps have to be filled, gang? No. What do we know? They usually do.

That gap would require a tick as low as $273.85 in order to fill. So, that's what I see as a potential worst-case scenario. The shares have gone a little lower since I've been typing. I can obviously not re-engage until this piece is a published work and considered to be public information. Once that condition is satisfied, I would expect to continue building a smallish, long position for a trade.

My goal would be that level that had become broken support (close to $322). Either way, I am out of these shares by the weekend. This stock is not, in my opinion, investment material.

At the time of publication, TheStreet Pro Portfolio was long UNH equity.