Wendy’s Best Value Meal? Its Shares

When the fundamentals, analysts and insider buying are in sync that's an exceptionally good sign. At the stock's low current price, upside potential far outweighs downside risk.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Sometimes the market appears inexplicable.

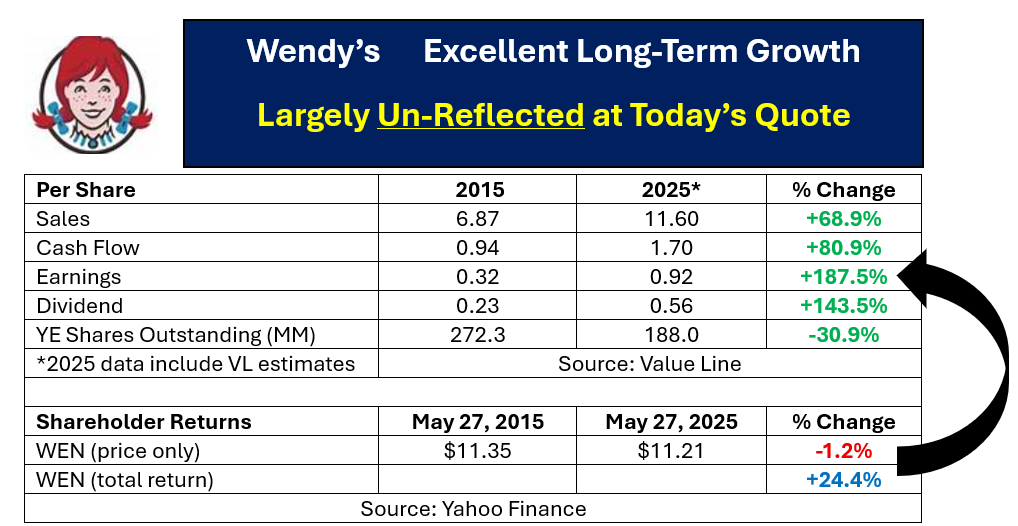

Fast food name Wendy’s WEN provides a prime example of that. Over the most recent decade Wendy’s showed fine growth across all major business metrics as denoted below.

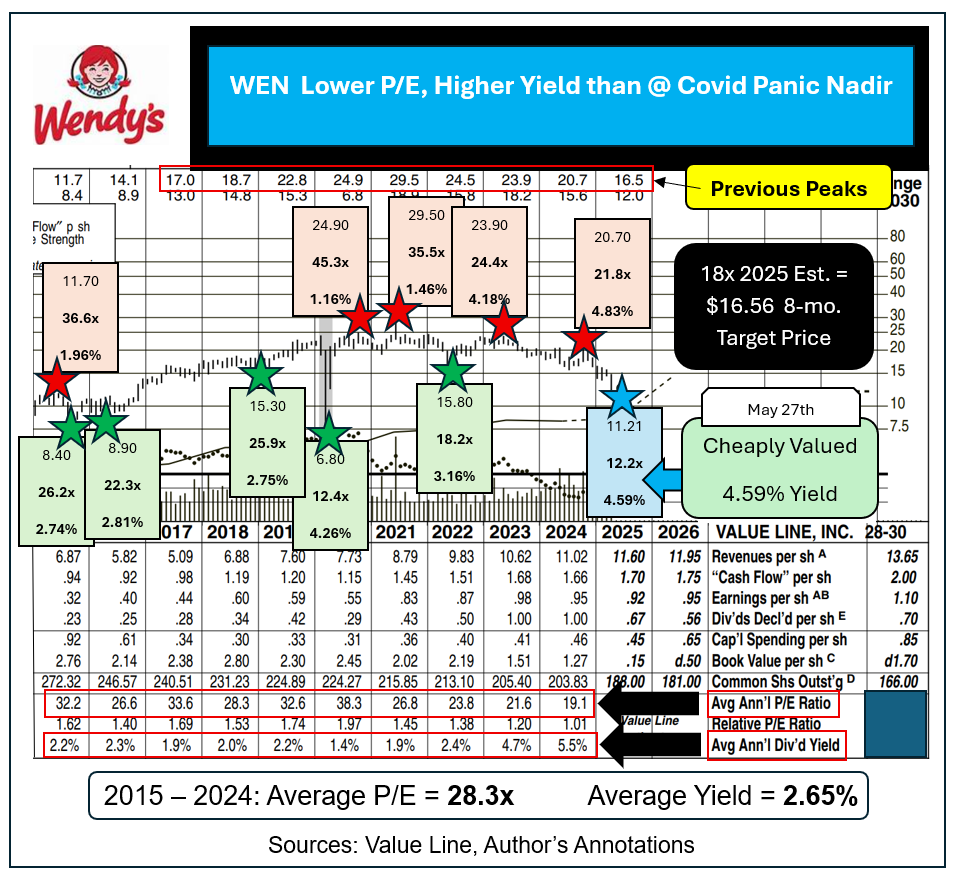

During each of the six full years 2019 through 2024 WEN peaked between $20.70 and $29.50.

Despite those fine fundamentals Wendy’s shares dipped to a new post-2016 low of $11.16 intraday on May 27, 2025.

Since 2015, the shares commanded an average multiple of 28.3x, accompanied by around 2.65% in yield.

At its May 27, 2025 price, the stock was offered at just 12.2 times its already reduced 2025 EPS estimate of $0.92, while paying a generous 4.59% current yield on a recently trimmed 14-cent quarterly payout.

Those metrics are now superior (for new buyers) to what WEN traded for at its to-the-penny nadir in the March 2020 Covid-panic selloff. Smart traders who bought back then saw the shares skyrocket by 266%, from $6.80 to $24.90, by October of the same year.

What are the shares worth?

I am not expecting WEN to immediately bounce back to a north-of-20x multiple. Assuming an 18 P/E on this year’s estimated $0.92 EPS generates an 8-month goal price of $16.56.

That implies about 48% upside by next winter plus around 3.7% from three dividend payments. Note: WEN goes ex-dividend for 14 cents next Monday. Buyers this week will earn five payments while holding just over one year.

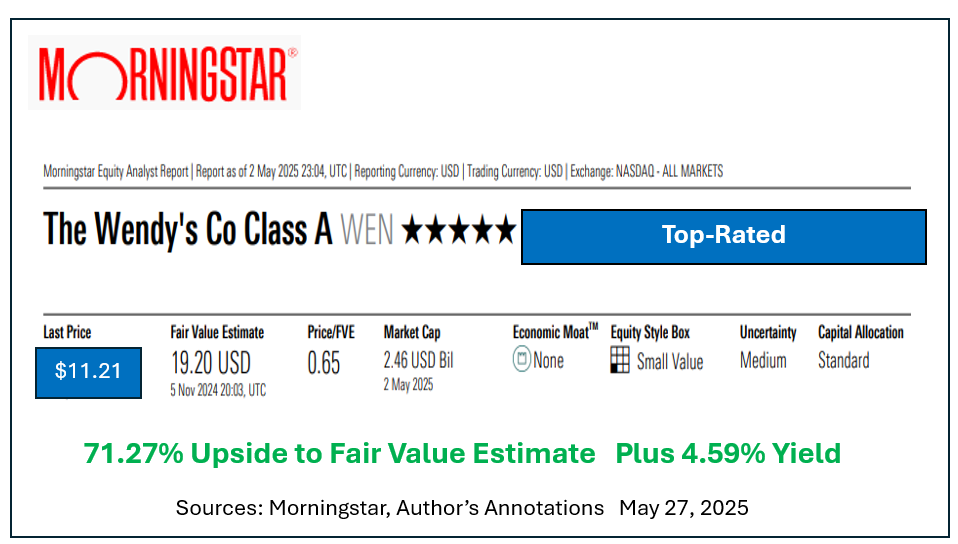

I am not alone in seeing Wendy’s substantial upside potential.

Research firm Morningstar rates WEN as a 5-star BUY while indicating a present-day fair value of $19.20 per share.

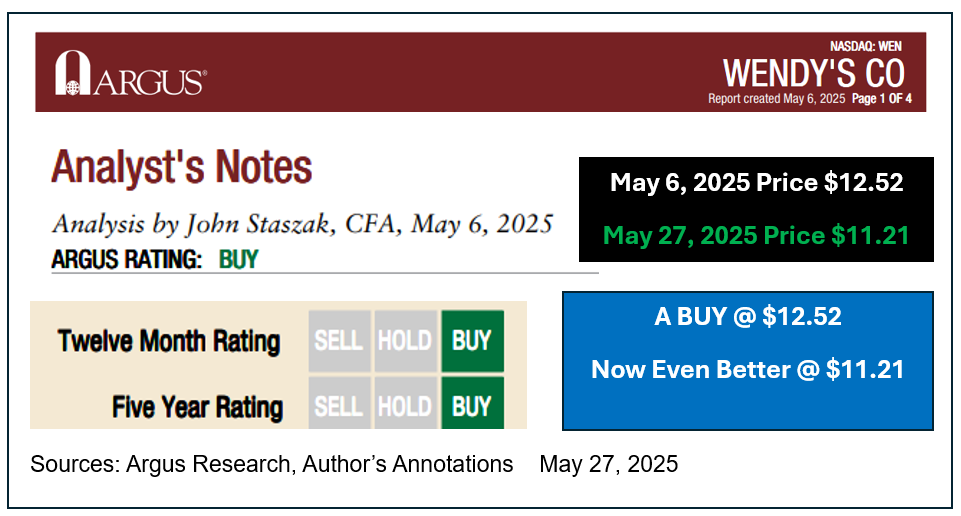

Argus Research called WEN a year-ahead and 5-year-out buy on May 6 when it fetched $12.52. It is an even better buy now, at $11.21.

TipRanks shows many more buy then sell recommendations on WEN from the 30 analysts they monitor. Their median goal price of $14 per share would deliver 25% upside within a year. The more optimistic, but not crazy, $21 1-year target price represents an over 87% gain. Neither of those figures in WEN’s 4.59% current yield.

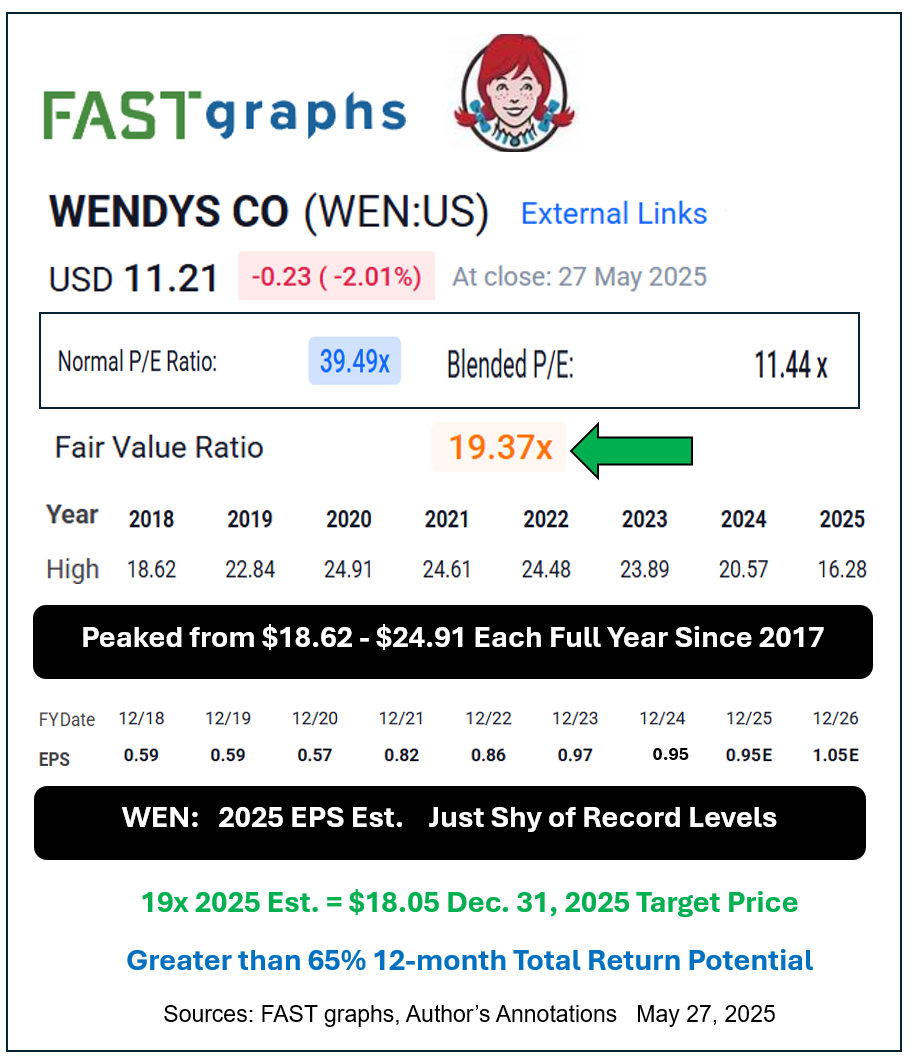

Quantitatively-based FAST graphs’ view calls Wendy’s fair value multiple as 19.37x. Reverting to near that very achievable level could easily send WEN shares back up to around $18.

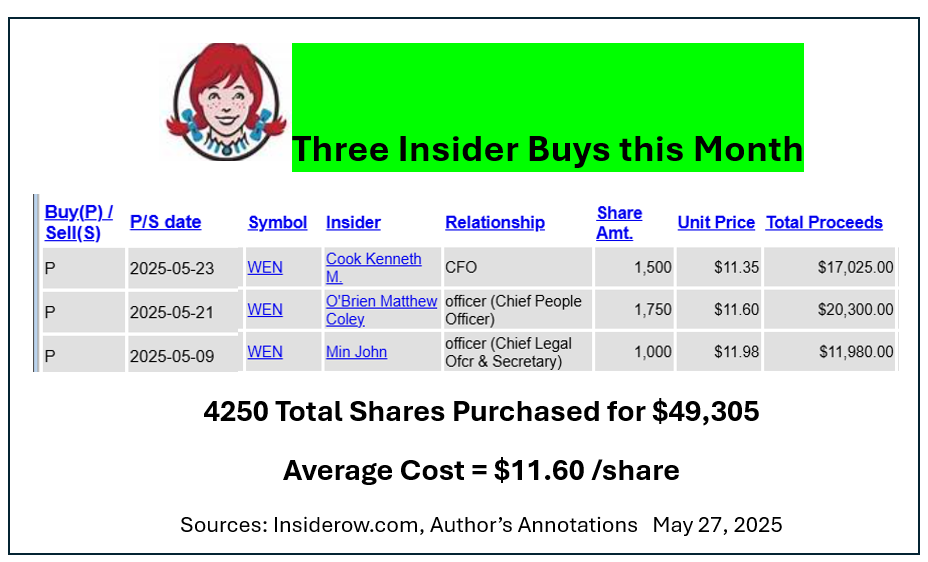

All these positive outlooks are confirmed by three insider buys in Wendy’s since May 5.

Purchases of almost $50,000 worth of stock at an average cost of $11.60 means buyers right now can own it cheaper than they paid.

When analysts agree and company officers second the motion with open market purchases, I take that as an exceptionally good sign.

From the low current entry price, upside far outweighs downside risk.

Buy some WEN shares, short some WEN puts or consider doing both.

At the time of publication, Price was long WEN shares, short WEN put options.