This Small Biotech Stock Is Still a Buy After Massive Bottom-Line Gift

This stock was a winner in 2025, and I believe it will continue to outperform this year.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Stocks are gaining some traction on Monday morning as investors digest the news about Venezuela and contemplate what themes and sectors will lead in 2026.

Small caps and big-cap technology are leading to start the week with both the Magnificent Seven (MAGS) and Russell 2000 (IWM) up about 1%. There is a good amount of speculative action with dozens of stocks jumping more than 10%. Rare earth, semiconductors, space and energy are some of the strongest themes.

One group that is lagging on Monday morning is biotechnology. I suspect this is just delayed profit-taking after the group finally had a good year in 2025. It has been a lagging sector for a long time and finally produced some profits in the second half of the year. It is a group I think will do well in 2026, so I'm watching closely for entries.

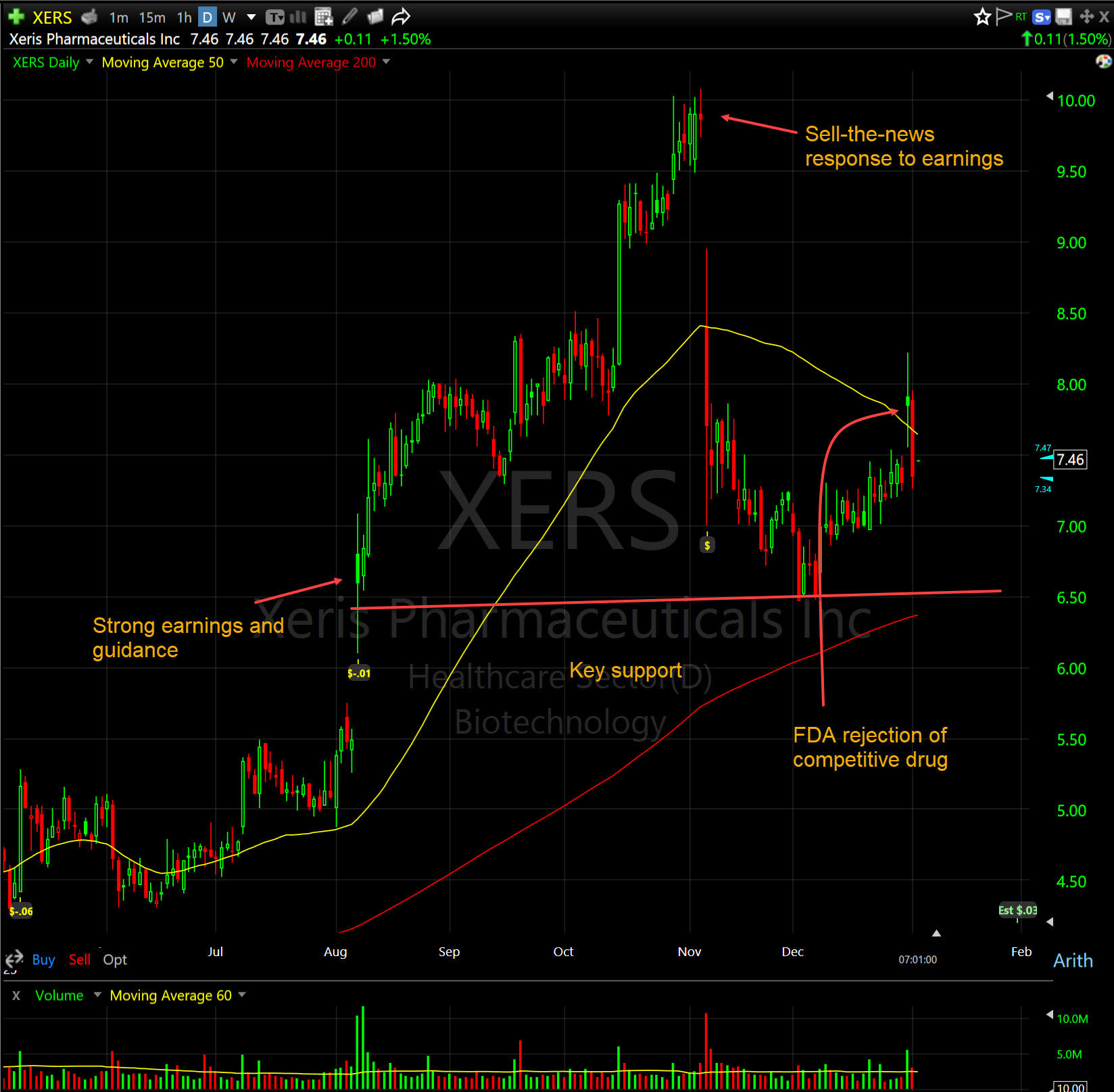

One name I want to highlight again is Xeris Pharmaceuticals (XERS) . It was a big winner in 2025, and I believe that some recent developments are creating a major opportunity for the stock. However, the sector is weak, and it appears that the market has not recognized the impact of recent news.

Xeris Biopharma is a commercial-stage specialty pharmaceutical company focused on developing and commercializing "ready-to-use" therapies for patients with endocrine and rare diseases. Based in Chicago, the company has successfully evolved from a clinical-stage, research-intensive biotech into a high-growth commercial entity that achieved its first-ever quarterly net profit in late 2025.

Xeris differentiates itself through its proprietary formulation technology platforms that address the stability and solubility issues that plague traditional injectable drugs. XeriSol is a technology that allows drugs that normally require refrigeration or reconstitution to remain liquid-stable at room temperature. XeriJect is a platform for ultra-high-concentration, small-volume injections of biologics (like monoclonal antibodies), making them easier for patients to self-administer at home.

Xeris currently generates revenue from three FDA-approved products, providing a diversified revenue base that is very rare for a small-cap biotech:

- Recorlev (levoketoconazole): A cortisol synthesis inhibitor for patients with Cushing's syndrome. This is currently the company's fastest-growing asset, with revenue up over 100% year over year.

- Gvoke (glucagon): A liquid-stable, pre-mixed autoinjector for severe hypoglycemia (extremely low blood sugar in diabetics). It competes directly with traditional kits that require manual mixing.

- Keveyis (dichlorphenamide): The first and only FDA-approved treatment for Primary Periodic Paralysis, a rare neurological condition.

Xeris is an attractive stock just based on the three current products, but the market has yet to appreciate the potential of a drug called XP-8121. This drug is a once-weekly subcutaneous injection of levothyroxine for hypothyroidism and has a total addressable market of over $1 billion. Current treatment for hypothyroidism requires daily oral pills taken on an empty stomach, which many patients struggle to adhere to or absorb properly. Xeris' product is a once-a-week injection that could revolutionize the standard of care for millions of patients. XP-8121 is currently Phase 3-ready, with the major trial expected to begin in the second half of 2026.

Xeris' stock sold off following its very good third-quarter report, partially due to the wait for further development of XP-8121 and partially due to concerns about competition for Recorlev. The company is increasing its sales force and stated that new competition would likely just help to create great recognition of the medical issue and increase the total market.

On December 31, 2025, the FDA issued a Complete Response Letter (CRL) to Corcept Therapeutics (CORT) for relacorilant, which is a direct competitor to Recorlev. The FDA requested more evidence of efficacy, potentially delaying relacorilant's entry into the Cushing's market by years. This removes major competition, and since Xeris recently doubled its sales and patient support teams in anticipation of this market battle, Xeris has a clear, uncontested window to capture market share in a sector experts believe could triple to $3 billion by 2030. Recorlev already holds Orphan Drug Exclusivity until late 2028, and this CRL removes the most immediate threat to its growth trajectory.

Xeris reported record-breaking numbers in its most recent quarter ending September 30, 2025, driven almost entirely by the strong growth of Recorlev.

Total product revenue: $74.1 million (+40% year over year).

This tremendous revenue growth has helped Xeris reach a financial inflection point, moving from a "survival-mode" biotech to a self-sustaining specialty pharma company.

Q3 2025 EPS was breakeven at $0.00. This compares to an EPS of ($0.11) in the same period last year. Net income was $0.6 million — the first positive net Income in the company's history. Adjusted EBITDA was $17.4 million in Q3, a $20 million improvement year over year. The cash position ended the quarter with $91.6 million in cash and short-term investments. Management has stated they have a stable cash runway for over three years if it maintains current cash flow levels.

Following the strong Q3 results and the expansion of the Recorlev sales force, management raised its floor for the year with 2025 revenue guidance of $285 million to $290 million (up from the previous $280 million to $290 million range). This represents roughly 42% growth over 2024. Management reaffirmed it expects to remain adjusted-EBITDA positive for the full year and going forward.

Official 2026 guidance is typically issued in March. Consensus analyst estimates now project 2026 revenue to surpass $360 million and 2026 annual EPS to reach approximately $0.18 to $0.23, marking the company's first full year of GAAP profitability.

The Corcept CRL is a massive gift to Xeris's bottom line. Xeris had already doubled its sales force and patient support teams in Q3/Q4 2024, so the infrastructure is already paid for and is reflected in the SG&A increase to $46.5 million.

With a competitor delayed, Xeris can now leverage that investment in marketing to capture more of the Cushing's market without having to significantly increase spending any further. This operating leverage is why analysts like Oppenheimer are projecting such high price targets ($18) — nearly every new dollar of Recorlev revenue now drops straight to the bottom line.

The next earnings date is around March 5, 2026, and there should be some presentations at investment conferences before then, where the benefit of the Corcept CRL will become clearer to that analyst community.

The chart is in a trading range, looking for support, and is causing some concern because of the poor price action.

At the time of publication, DePorre was long XERS.