Think the Market Prices Stocks Efficiently? A Stunning Example of Ignored Value

This company's stock price cannot get much more abominable and presents a fantastic opportunity.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Those who think the stock market is efficient in pricing securities must not be owners of Yeti Holdings YETI.

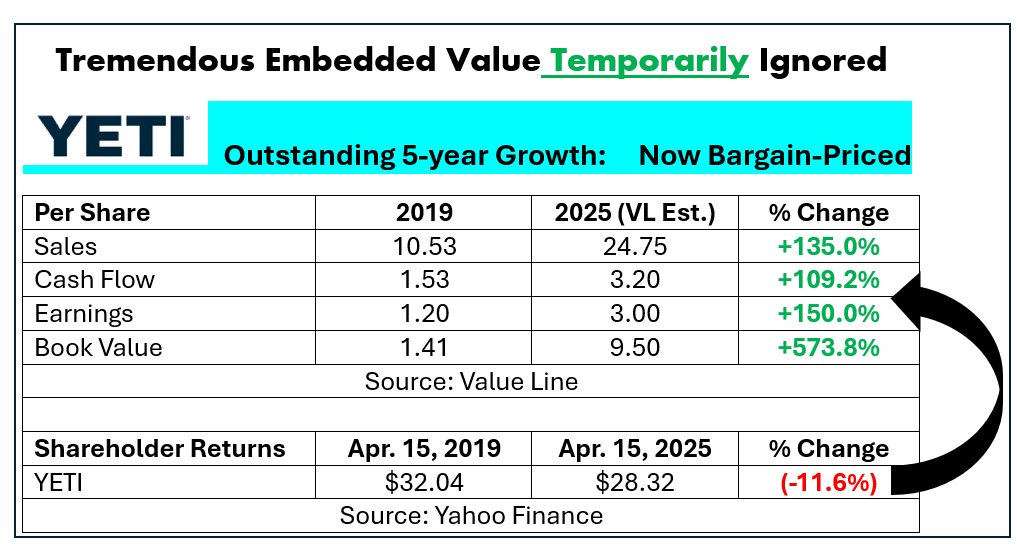

The company posted excellent results since coming public on October 29, 2018 but currently trades for less than it did exactly five years earlier. 2024’s adjusted earnings were a record $2.73 per share, up 21.3% from $2.25 in 2023.

The table below chronicles the outstanding across-the-board progress YETI made over the first full years of its existence as a publicly traded stock.

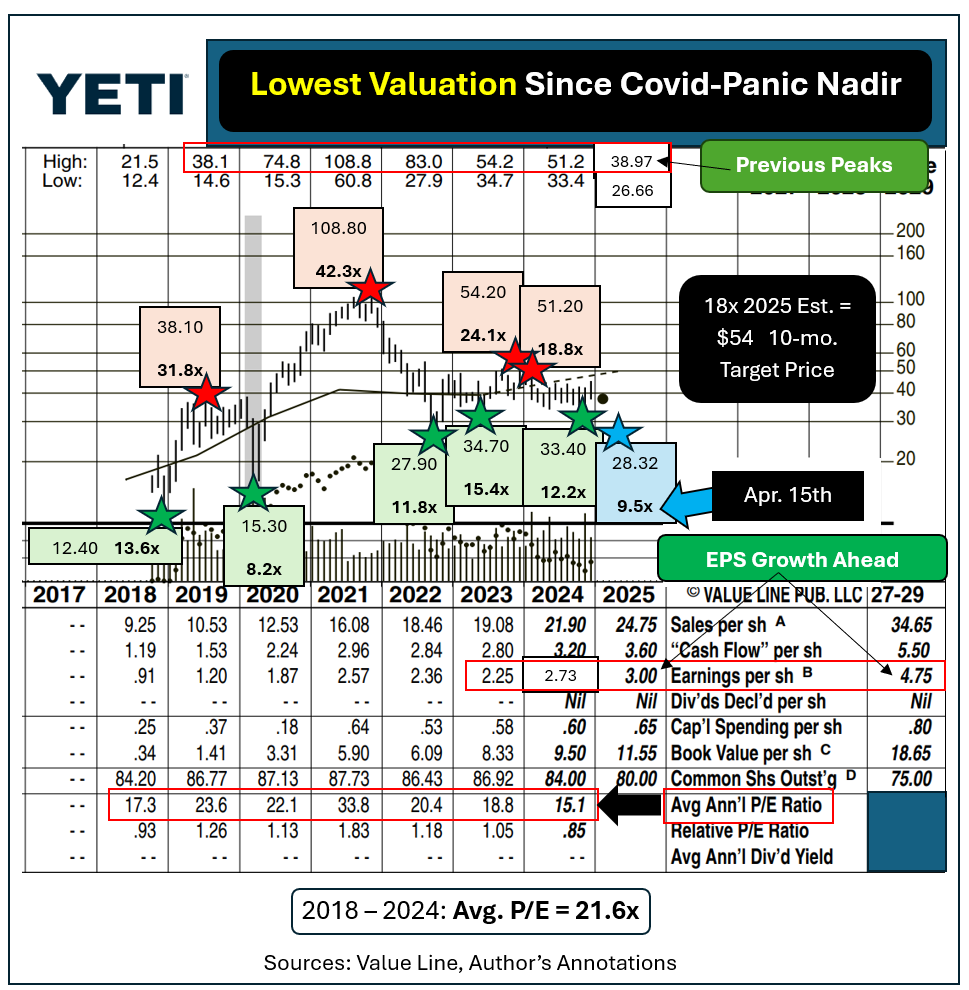

During 2019 YETI fetched 26.7 times earnings. It now trades for about 9.5 times Value Line’s 2025 estimate. Multiple contraction like that has been devastating for long-term owners but presents a fantastic opportunity for those getting involved with YETI now.

The shares were highly sought after from its IPO through late 2021. YETI peaked at $38.10 in the summer of 2019 while commanding 31.8 times that year’s final EPS tally.

The Covid panic selloff pushed the stock down, along with almost all other shares, to a crazy nadir of $15.30. At that time YETI sold for just 8.2 times its eventual 2020 EPS. Buyers at that low were rewarded with a greater than 610% surge by November of 2021.

Putrid market conditions for both stocks and bonds saw YETI drop back to just shy of $28 in October 2022. That represented a stunning 74.3% pullback from the stimulus-fueled 42.3x multiple it fetched at $108.80.

Since then YETI made a series of up-and-down progressions. It topped out above $54 in 2023 and north of $51 early in 2024. It changed hands at nearly $39 as recently as January 28 this year.

On the heels of the tariff-related plunge this month YETI made a new post 2020 low of $26.66. The stock bottomed momentarily intraday on April 15, 2025 at $27.99.

What Is YETI Worth?

Yeti's long-term average P/E has run 21.6x. Throw out the insane Covid panic bottom and Yeti has never been offered at a cheaper valuation than recently.

It surged by 207%, from $12.40 (a 13.6 P/E) in December 2018 to $38.10 in the summer of 2019.

Yeti ran wild from the Covid low (an 8.2x multiple) to its late 2021 peak. More modest but still excellent rallies from $27.90 (11.8 times earnings) to $49.80 in just four months offered a gain of better than 78%.

A pullback to $34.80 led to a rebound to $54.20, representing an almost 56% rise. Last fall’s low of $33.40 preceded the late January 2025 peak of $38.97 (+16.7%).

As I am writing YETI is offered for dollars per share below its absolute bottoms during both 2023 and 2024. That appears illogical as EPS grew in 2024 and seem poised for even better results this year and beyond.

The company is net debt-free. As of September 2024 Yeti held over $280 million in cash versus total debt of only $80.7 million. There are no preferred shares. There is no defined benefit pension to deal with either.

Management has retired shares over the past five years, dropping outstanding stock from about 87.1 million to just about 84 million, a decline of 3.55%. More authorizations for further buybacks are still outstanding. The lower quote right now makes that program more effective than it was when YETI traded much higher.

At 18 times this year’s Value Line estimate YETI could rebound to around $54, approximately double the recent quote. Based on its actual trading history that number is far from an upper limit.

What do other research houses say about YETI?

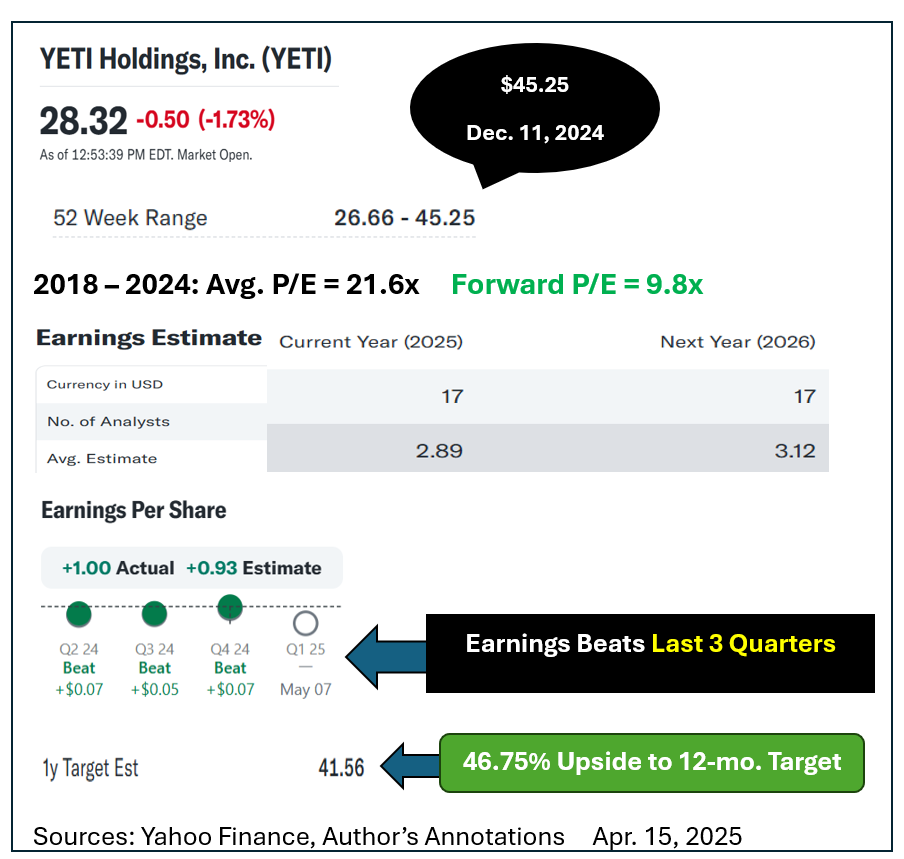

Yahoo Finance takes a somewhat conservative view. Its 12-month target price is $41.56 implying about 47% upside potential. I call that conservative as it assumes YETI will only fetch 14.4 times earnings, about one third lower than its historically average 21.6x multiple.

Note, too, that YETI changed hands as high as $45.25 as recently as Dec. 11, 2024.

The company beat analyst estimates on each its most recent quarterly reports.

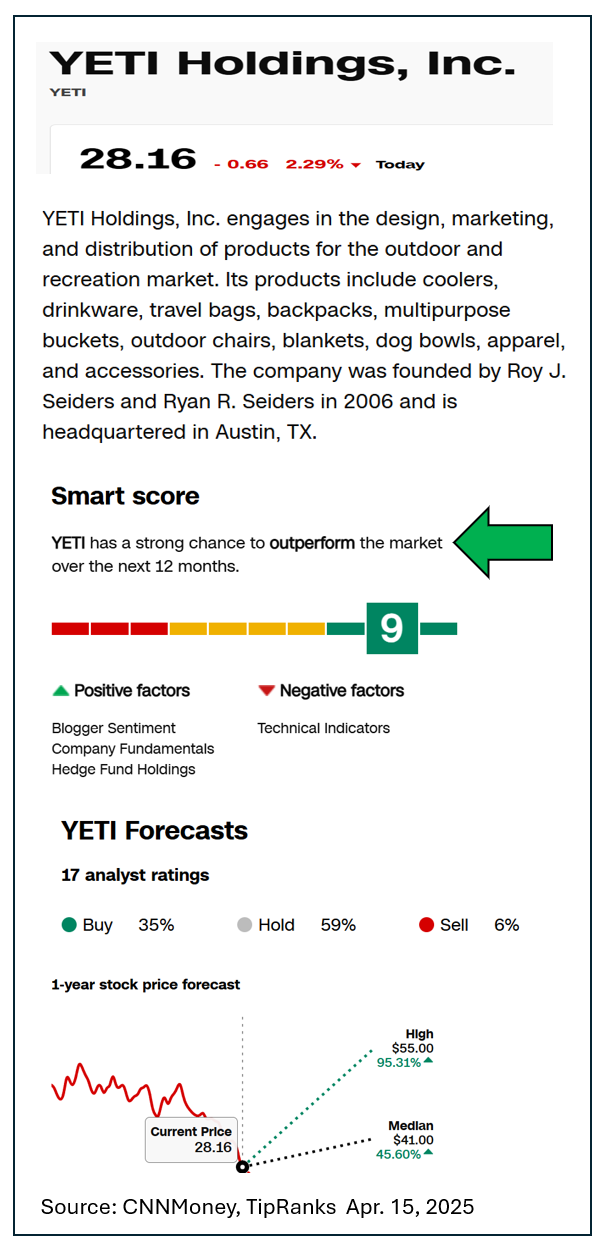

CNN Money, in partnership with TipRanks research, gives YETI a “strong chance to outperform the market” in the year ahead.

Its median forecast calls for YETI to bounce back to $41 by this time next year. Their more bullish analysts see YETI at $55 by then.

Quantitatively focused FAST graphs think 23.61 times earnings is YETI’s historical normal valuation. That is higher than my own calculation of 21.6x.

Regardless, YETI, at under 10 times earnings, appears to be a hugely discounted bargain.

Fifteen, 18 and 20 times FAST graph’s own estimate for the firm’s 2025 EPS project an end-of-the-year goal price range of from $43.95 to $58.60. Reaching any of those targets would provide excellent nine-month profits from here.

YETI has offered exits well above the current quote year after year. Peak prices during 2020, 2021 and 2022 were all at least double to triple YETI’s price right now.

What more do you need to know?

Yeti has a pristine balance sheet and a history of solid growth in fundamentals. How many things can you buy today cheaper than five years ago even though they are far more valuable now?

Upside potential dwarfs what appears to be minimal downside risk.

At the time of publication, Price was long YETI shares.