Tariff Turmoil Has Me Seeking Shelter in Biotech Trades

News around Pres. Trump's latest moves has roiled the markets and led to some lower entry points

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Every little piece of news flow around tariff policies continues to roil the markets. It almost feels like equities are being trolled at this point as tariffs get changed on the fly. Markets sold off again on Thursday thanks to these changes. All the major indexes ended significantly in the red. The Nasdaq fell over 2.5% while the S&P 500 was off nearly 1.8% and the Dow declined 1% on the day. Both oil and the yield on the 10-Treasury were relatively flat on the day.

This increased volatility has resulted in lower entry points in what was an overbought market, and to some extent still is. I have been incrementally putting slugs of the considerable amount of dry powder in my portfolio to work on down days like on Thursday. I am using covered call orders for the most part to mitigate downside as I don’t feel the market has found a bottom yet and is unlikely to do so in March.

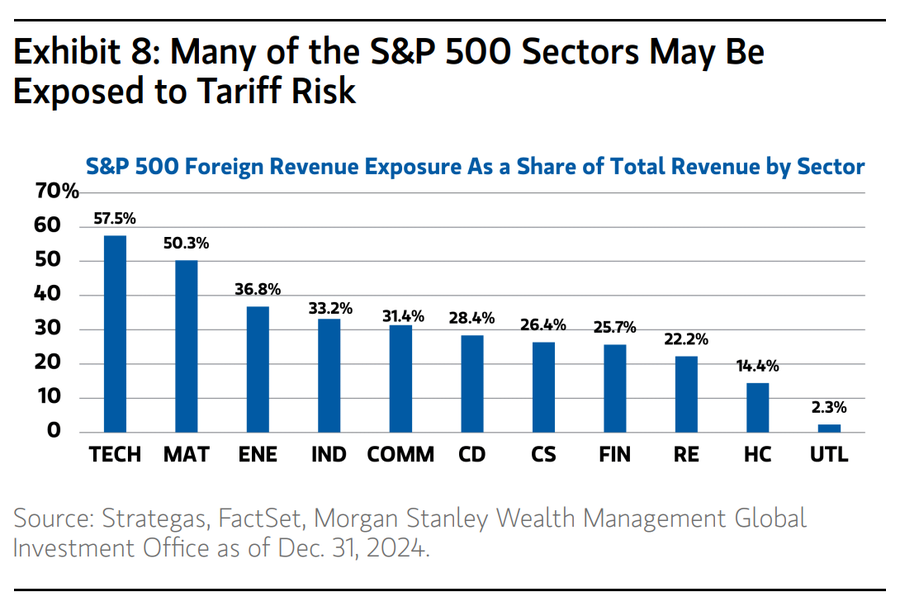

I particularly like healthcare as the sector has myriad stocks with reasonable valuations, the sector is defensive, and this area of the economy is one of the least affected by tariff policies. A simple way to increase exposure to this area of the market is to use exchange-traded funds like the iShares Biotechnology ETF IBB, whose top holdings include Gilead Sciences GILD and Amgen AMGN.

I have also been adding exposure to individual healthcare and biotech/biopharma stocks. Given the risk off nature of the market right now, I am largely sticking with names that are already profitable. I also like many in the small and mid-cap space that get little to none of their revenues from overseas, making them even more tariff resistant and with little exposure to fluctuating currencies as well.

I executed some covered-call orders against ANI Pharmaceuticals, Inc. ANIP earlier this week. This biopharma company reported fourth quarter results in late February that easily beat both top- and bottom-line expectations as revenues rose nearly 45% on a year-over-year basis, thanks largely a recent strategic acquisition and stellar growth from a core product as well. Management also boosted fiscal 2025 revenue and profit guidance. The stock is not expensive at 10-times expected unadjusted earnings per share in the current fiscal year and management has done a good job increasing operational cash flow.

I also added some additional shares in Harrow, Inc. HROW yesterday as the stock in this ocular focused biopharma company has been unfairly knocked down during the recent selloff in the overall market. I just highlighted Harrow in depth late last month.

At the time of publication, Jensen was long ANIP, HROW and IBB.