Target’s Selloff Now Values It Lower Than at Its Covid-Panic Bottom

Here's my in-depth take on the retailer and why it is a prime "Buy" candidate right now.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The pain of severely beaten-down share prices has a flip side. It makes for tremendous bargains for those investors brave enough to actually buy low.

How can you tell if a particular stock is down for the count or is a great rebound candidate? Analyze the facts, apply reasonably conservative assumptions, and buy stocks which appear to offer exceptional upside potential.

Here is my take on Target TGT. It is a widely held, institutional name with estimated FY 2025 revenues approaching $108 billion.

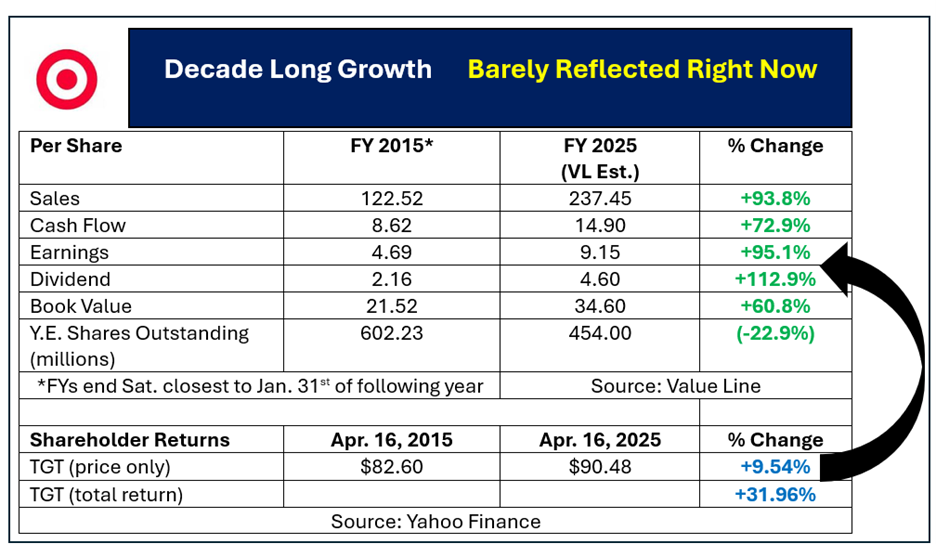

Per-share sales have never been higher. Cash flow per share is nearly as high as all prior years except for the stimulus-fueled numbers of FY 2021. Ditto for projected EPS.

The annual dividend rate of $4.48 is projected to rise slightly, to $4.60 this year. At TGT’s Apr. 16, 2025 close of $90.46 the forward yield weighs in at a juicy 5.08%.

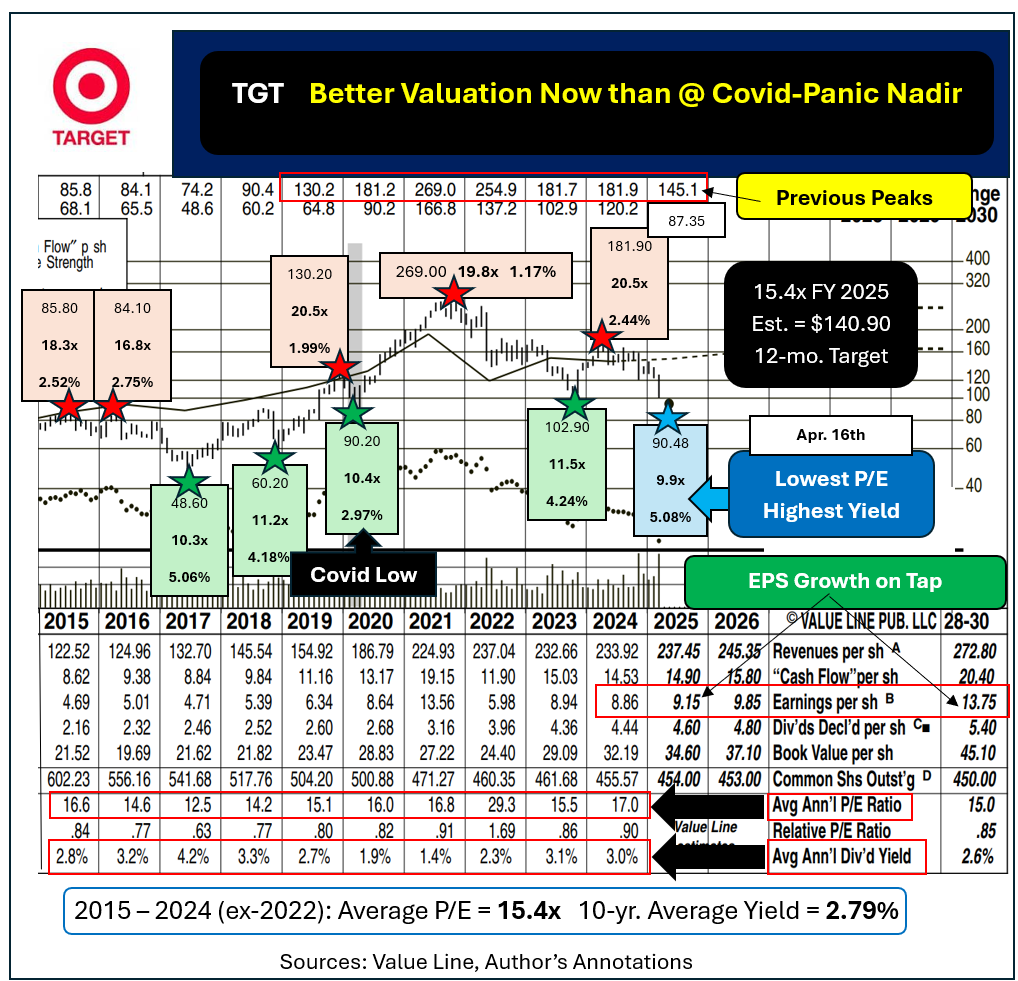

Target’s forward P/E now sits below what was registered at the to-the-penny low during the Covid panic. What happened following that crazy pullback to $90.20 (just 46 cents below where the shares closed about five years ago?)

From April 2020 through November 2021 Target shares surged from $90.20 to $269, a tidy run of +198.2% plus dividends. Bargain seekers were generously compensated for buying when Covid uncertainty was running rampant.

Today’s low price on TGT reflects tariff-related uncertainties which, like Covid’s, are likely to be resolved much sooner than most people expect.

The 10-year growth table, which follows, details Target’s solid growth across every major business metric. If this year’s projections prove accurate EPS will have almost doubled. Dividends wil have tacked on over 112%. Revenues, cash flow and book value will show solid gains too.

Another side benefit? Over the decade management will have retired almost 23% of all shares outstanding.

You would think that shareholders were well rewarded. That was true at TGT’s market peaks. Right now, though, Target's quote reflects just a small portion of the value created since 2015.

That is unfortunate for those who simply bought and held. But it is great news for traders buying in today.

What Is Target Worth?

Its average P/E multiple ran 15.4x if you throw out the artificially inflated multiple from FY 2022. A normalized yield was around 2.79%.

Previous best entry points (green-starred below) ran from 10.3x to 11.5x. Yields at those same times ranged from 5.06%, in 2017, to 2.97% at the Covid bottom.

TGT’s five “should have sold” moments (red-starred) all came at above-average multiples accompanied by less-than-average yields. The average P/E at those overpriced peaks was 19.2x. The average yield was 2.15%, about 22.8% below normal.

Target is now offered at the lowest forward multiple on the chart below while paying its highest yield ever. That makes it a prime "Buy" candidate.

Assume a rebound to a normalized 15.4x P/E and the year-ahead price target works out to almost $141 per share. That implies total return potential of about 61%.

That goal is far from an upper limit. TGT changed hands as high as $145.10 since the start of 2025. It fetched north of $181 during each of the five years from 2020 right through 2024.

Reverse engineering the current $4.48 annual dividend to an average 2.79% calculates a price target of $160.57 for TGT.

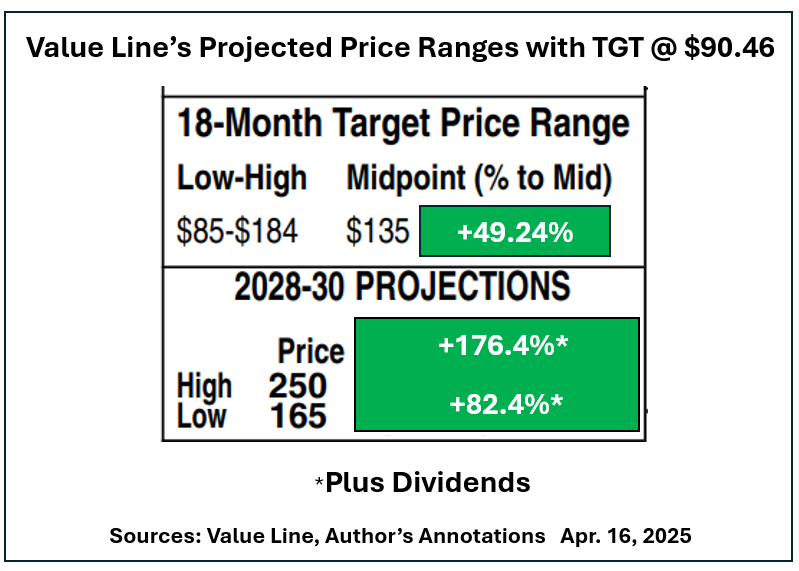

Value Line sees a rebound to about $135 within 18 months. Their three- to five-year projected price range for TGT runs from $165 to $250.

Quantitatively focused FAST graphs calls TGT’s normalized P/E as a very precise 16.46x. It notes TGT’s ‘A’ credit rating (source: S&P) high yield and low P/E.

Its FY 2025 estimate is 3 cents below Value Line’s $9.15. Assume TGT bounces back to 16.4 times FAST graphs’ estimate and the February 2026 goal price is nearly $150.

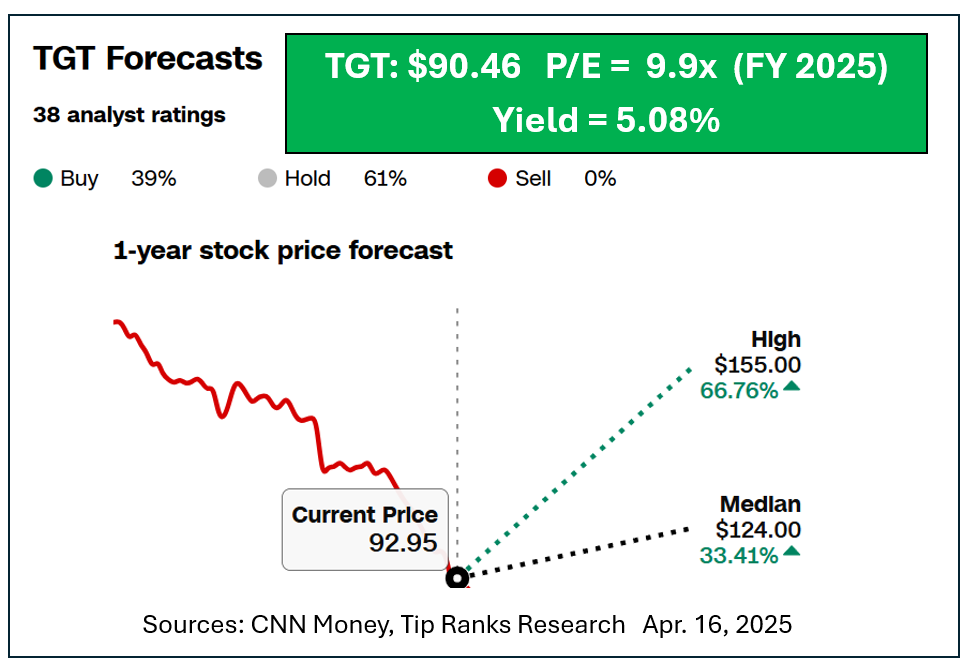

CNN Money teams up with Tip Ranks research to issue stock price forecasts while presenting analysts’ opinions.

For TGT, the thirty-eight analysts show 39% buy opinions, 61% hold and 0% sell recommendations. The median 12-month goal of $124 would generate 38.5% in total return. The higher-end goal sits at $155, implying a total return of greater than 76% by this time next year.

No matter how you slice and dice the numbers, Target appears severely undervalued.

Buy some shares, short some in-the-money LEAP puts or consider doing both. Options expirations on widely held TGT extend as far out as January 2027.

At the time of publication, Price was long TGT shares (bought this week).