Swapping CrowdStrike for Competitors After Disappointing Compensation Move

The cybersecurity firm saw some unimpressive results and I'm going to exit.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

I have told everyone who would listen for years now, that CrowdStrike Holdings CRWD was the "best in class" name in cybersecurity. I have stuck with CrowdStrike through thick and thin, even during that debacle over a year ago that involved Microsoft MSFT and even when more well-known pundits were touting the praises of Palo Alto Networks PANW and Zscaler ZS.

My faith in the name has, over time, paid off quite handsomely. The name has been, and remains, a top-five holding of mine, even after trading around my core position a few times and even after taking profits on a small portion of my long position last week after CRWD hit my $470 target price.

On Tuesday night, CrowdStrike went to the tape with the firm's fiscal first quarter financial performance. Overnight, a vengeful Wall Street took its collective pound of flesh. Let's dig into the numbers and see what we can see. Shall we?

The Quarter

For the three-month period ended April 30, CrowdStrike posted an adjusted EPS of $0.73 (GAAP EPS: -$0.44) on revenue of $1.103 billion. The adjusted bottom-line print beat Wall Street, but the GAAP number and the top-line number both disappointed mildly. The revenue generated was good enough for year-over-year growth of 19.8%. This amounts to a sharp deceleration in year-over-year revenue growth from previous quarters. The lion's share of the adjustment made ($1.07 per share) was for the purpose of stock-based compensation expense.

During the quarter, CrowdStrike did add $194 million in net new annual recurring revenue (ARR) ending the period at $4.4 billion. The firm delivered strong Falcon Flex deal momentum with accounts exceeding $3.2 billion in total deal value, which is more than six-times growth from a year ago at this time. Falcon is the firm's AI-native platform. Falcon Flex is a subscription model aimed at the acceleration of client adoption. This adoption is now running at a "faster pace than we've ever seen before" according to CEO George Kurz.

Operations

As revenue grew 19.8% to $1.103 billion, the cost of that revenue landed at $289.291 million (+28.5%). This produced a gross profit of $814.291 million (+17%) as gross margin dropped from 75.6% to 73.8%. Subscription gross margin dropped from 78% to 77%. Once adjusted, that subscription gross margin dropped from 81% to 80%.

GAAP operating expenses increased by a whopping 36.3% to $938.947 billion. Of that, $271.571 million was either stock-based compensation or related taxes. That's year over year growth of 37.3% and seems possibly a little excessive. Is the firm paying itself too much? That's a good question, especially when the adjusted EPS is quite profitable, but the actual EPS is deeply negative almost solely due to this compensation.

This left GAAP operating income/loss at -$124.656 million, down from $6.936 million for the year-ago comp. Yikes! After accounting for interest, other income and expenses, and taxes, GAAP net income/loss attributable to shareholders dropped to -$110.207 million from last year's $42.82 million. That works out to a GAAP EPS of -$0.44 per fully diluted share, down from $0.18 a year ago.

On an adjusted basis, net income attributable to shareholders dropped 6.1% to $184.704 million, which works out to an adjusted EPS of $0.73. down from $0.79. Color me less impressed than I thought I was going to be 24 hours ago.

Guidance

For the current quarter, CrowdStrike sees total revenue of $1.1447 billion to $1.1516 billion. This is below the $1.6 billion that Wall Street was looking for. Adjusted operating income is projected at $226.9 million to $233.1 million and adjusted net income at $209.1 million to $213.8 million. That would put the adjusted EPS at $0.82 to $0.84, which is a beat of the $0.81 consensus view.

For the full year, CrowdStrike sees total revenue of $4.743.5 billion to $4.805.5 billion. This pulls the midpoint of the range below Wall Street's expected $4.79B. Adjusted operating income is projected at $970.8 million to $1.0108 billion and adjusted net income at $878.7 million to $909.7 million. That would leave the firm's adjusted full year EPS at $3.44 to $3.56, which at the midpoint, is a beat of the $3.45 consensus view.

Fundamentals

For the quarter reported, CrowdStrike generated operating cash flow of $384.107 million. Out of that number came capex spending of $85.751 million, internal use software and website development costs of $17.437 million, $1.459 million in the purchase of deferred compensation investments and $45,000 in the proceeds from the sales of such investments.

That left free cash flow of $279.415 million, which is down 13.4% from the year-ago comparison. The firm did not return capital to shareholders during the quarter, but did announce a new authorization to repurchase up to $1 billion worth of common stock. My guess is that commoners holding the shares might have preferred a cash dividend. These guys sure do like to pay themselves.

Glancing at the balance sheet, the firm ended the quarter with a cash position of $4.614 billion and current assets of $6.071 billion. Current liabilities add up to $3.283 billion including an impressive $2.747 billion in deferred revenue, which is not a true financial obligation. That puts the firm's current ratio at a robust 1.85. Once adjusted for those deferred revenues, this ratio rises to a Herculean 11.33.

Total assets amount to $8.72 billion, including $1.039 billion in goodwill and other intangibles. At less than 12% of total assets, this is no cause for concern. Total liabilities less equity comes to $5.229 billion, which includes another $1.024 billion in deferred revenue and just $744.355 million in long term debt. That's something the firm could take care of more than six times over out of pocket. This is an exceptional balance sheet.

Wall Street

Since these earnings were released, I have found 19 highly-rated (four-plus stars at TipRanks) sell-side analysts who have opined on CRWD. Among those analysts, after allowing for changes, are 14 "buy" or buy-equivalent ratings and five "hold" of hold-equivalent ratings. One "buy" rating and one "hold" rating elected not to set a target price, so we have just 17 of those to work with.

The average target price across the remaining 17 analysts now stands at $501.76 with a high of $550 (Andrew Nowinski of Wells Fargo) and a low of $440 (Peter Levine of Evercore ISI). Once omitting those two as potential outliers, that average rises to $502.67. Because you were curious, the average buy rating set a $512.69 target, while the average hold rating set a target of $466.25.

My Thoughts

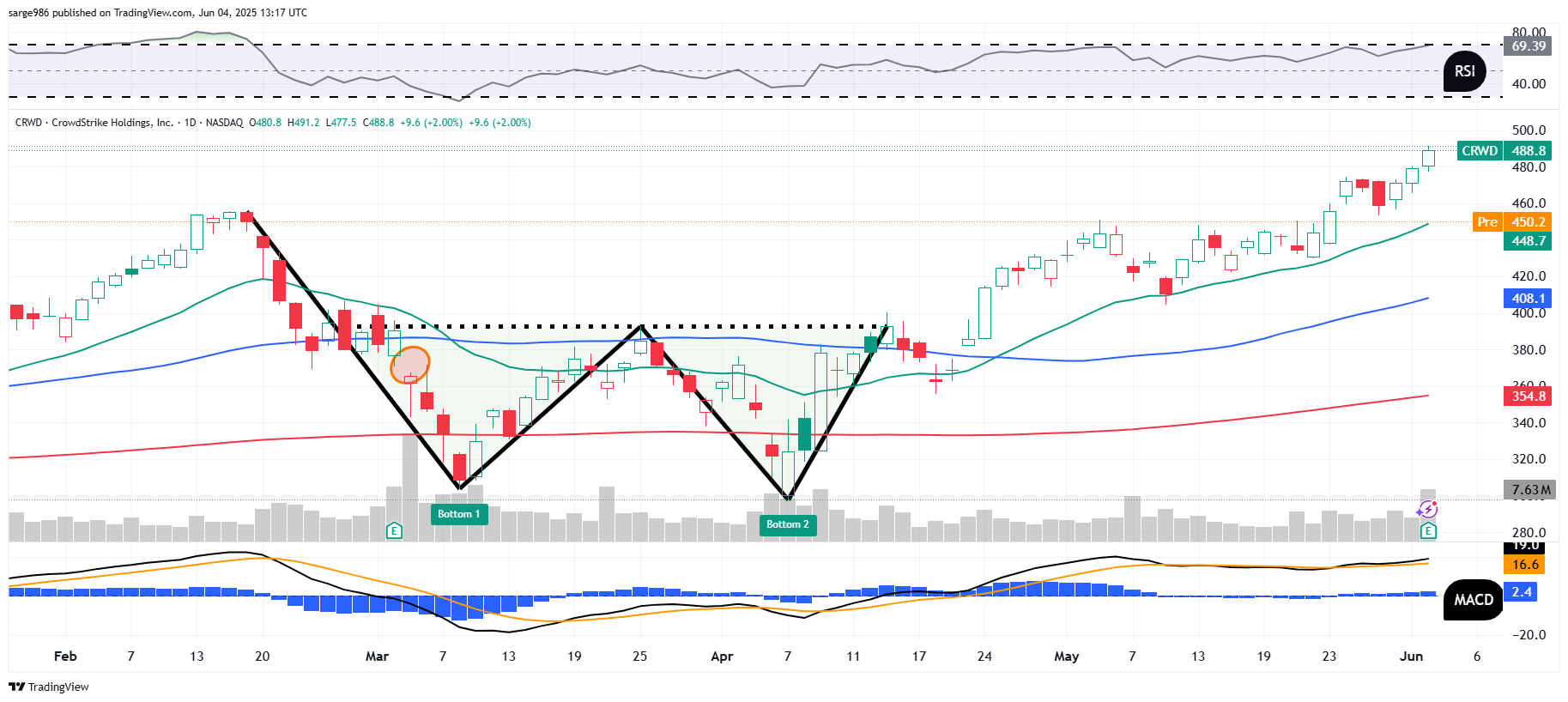

Obviously, this is still a well-run company, and the firm is still executing at a high level. Cash flows are still strong even though they are decelerating. The balance sheet is fortress like and enough to stay invested in the stock on its own merits. That said, I am disappointed in the size of the firm's stock-based compensation expense and a little bit in the repurchase authorization as well. Let's take a look at the chart:

On April 25, in a Market Recon column, I gave you this double-bottom pattern of bullish reversal with a $470 target price. At that time, the shares were trading with a $14 handle. On May 6, while subbing for Doug Kass, with the share trading with a $41 handle, I reiterated that target. Readers can see here that the stock went out on Tuesday night with a $88 handle and is last trading in the low $450s after this report and this somewhat less than hoped for guidance.

Readers know that I jettisoned SentinelOne S some time ago. This has been my only cybersecurity name ever since. I do think that I have to stay invested in cybersecurity. I am not ready to give up on CRWD. That said, I no longer believe that this name deserves a place in my top-five holdings and after having sold some last week at target, will be selling more on strength when strength arises in order to diversify my holdings in the space.

Current candidates would be, you guessed it, Palo Alto Networks and Zscaler. My target price of $470 stands.

At the time of publication, Guilfoyle was long CRWD and MSFT equity.