Sticking With This JP Morgan Price Target After $2 Billion Beat

The financial services giant is proving to be a best-in-class leader.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

I came in long the shares of two of Tuesday morning's financial giants that were set to report: JP Morgan Chase (JPM) and Wells Fargo (WFC) . I have only time to write something up on one today, and I have covered Wells Fargo closely for years, so let's do JPM. Nice quarter. Rock and roll!

For the firm's third quarter, JP Morgan Chase posted a GAAP EPS of $5.07 on managed revenue of $47.12 billion or reported revenue of $46.27 billion. Either way you slice it, revenue grew 9% from the year-ago period while beating Wall Street's expectations by close to $2 billion. As for profitability, that $5.07 print crushed projections for something in the mid-$4.80s and compared very well to last year's comp of $4.37.

Net interest income across the firm was flat from the year ago period at $23.4 billion, while non-interest revenue was up 16% to $14.8 billion. Non-interest expense was up 8% to $24.281 billion, while the firm's provision for credit losses grew 9% to $3.403 billion. Return on common equity improved from 16% to 17%, while return on tangible common equity improved from 19% to 20%.

Sector Performance

- Consumer and Community Banking.. Net revenue increased 9% to $19.473 billion as revenue driven by Banking & Wealth Management grew 0% to $11.04 billion. Card Services & Auto experienced growth of 12%, partially offset by Home Lending (-3%). Net income soared 24% to $5.009 billion as the provision for credit losses dropped 9% and non-interest expense grew 7%.

- Commercial & Investment Banking: Net revenue increased 17% to $19.878 billion as revenue driven by Markets grew 24% to $10.359 billion (Fixed Income was up 21%, Equities were up 33%). Banking and Payments experienced growth of 10% (Investment Banking was up 16%). Net income soared 21% to $6.901 billion as the provision for credit losses grew 156% (to $809 million) and non-interest expense grew 11%.

- Asset & Wealth Management: Net revenue increased 12% to $6.066 billion as the provision for credit losses grew from $4 million to $59 million and non-interest expense grew 5%. This left net income at $1.658 billion (+23%).

- Corporate: Net revenue decreased 45% to $1.703 billion as non-interest expense dropped 24%, leaving net income at $825 million (-54%).

Jamie Dimon

On the firm's performance:

“Each line of business performed well. In the CIB, IB fees rose 16% as ECM and M&A activity picked up against a supportive backdrop. We continued to benefit from higher client activity and demand for financing in Markets, with record third-quarter Markets revenue of nearly $9 billion. In CCB, we ranked #1 in U.S. retail deposits for the fifth consecutive year, and we continue to acquire new accounts at a robust pace, adding more than 400,000 net new checking accounts this quarter. Additionally, in wealth management, first-time investors surpassed 43,000, setting a new record. Finally, in AWM, revenue topped $6 billion, and AUM net inflows remained strong at $109 billion, highlighting the strength of the franchise.”

On the U.S. economy:

“While there have been some signs of a softening, particularly in job growth, the U.S. economy generally remained resilient. However, there continues to be a heightened degree of uncertainty stemming from complex geopolitical conditions, tariffs and trade uncertainty, elevated asset prices and the risk of sticky inflation. As always, we hope for the best, but these complex forces reinforce why we prepare the Firm for a wide range of scenarios.”

Guidance

For the full year, JP Morgan increased guidance for net interest income (NII), excluding markets, from a rough $92 billion to about $92.2 billion. Inclusive of markets, the firm now sees NII of $95.8 billion, up from prior guidance of $94.5 billion. That's also above the $95.1 billion that Wall Street was looking for. Full-year guidance for adjusted market dependent expenses was lifted from $95.5 billion to $95.9 billion, but guidance for the firm's credit card net charge off rate was cut to 3.3% from 3.6%.

My Thoughts

Excellent quarter. Strong guidance. Very impressed with the firm's expected national investment plan revealed on Monday. JP Morgan Chase has reinforced the notion that this is the "best in class" financial institution in the nation and maybe the world. Dimon has reinforced his reputation for being the nation's top private sector banker, though Charlie Scharf at Wells Fargo is, if not gaining on him, building for himself quite a positive look.

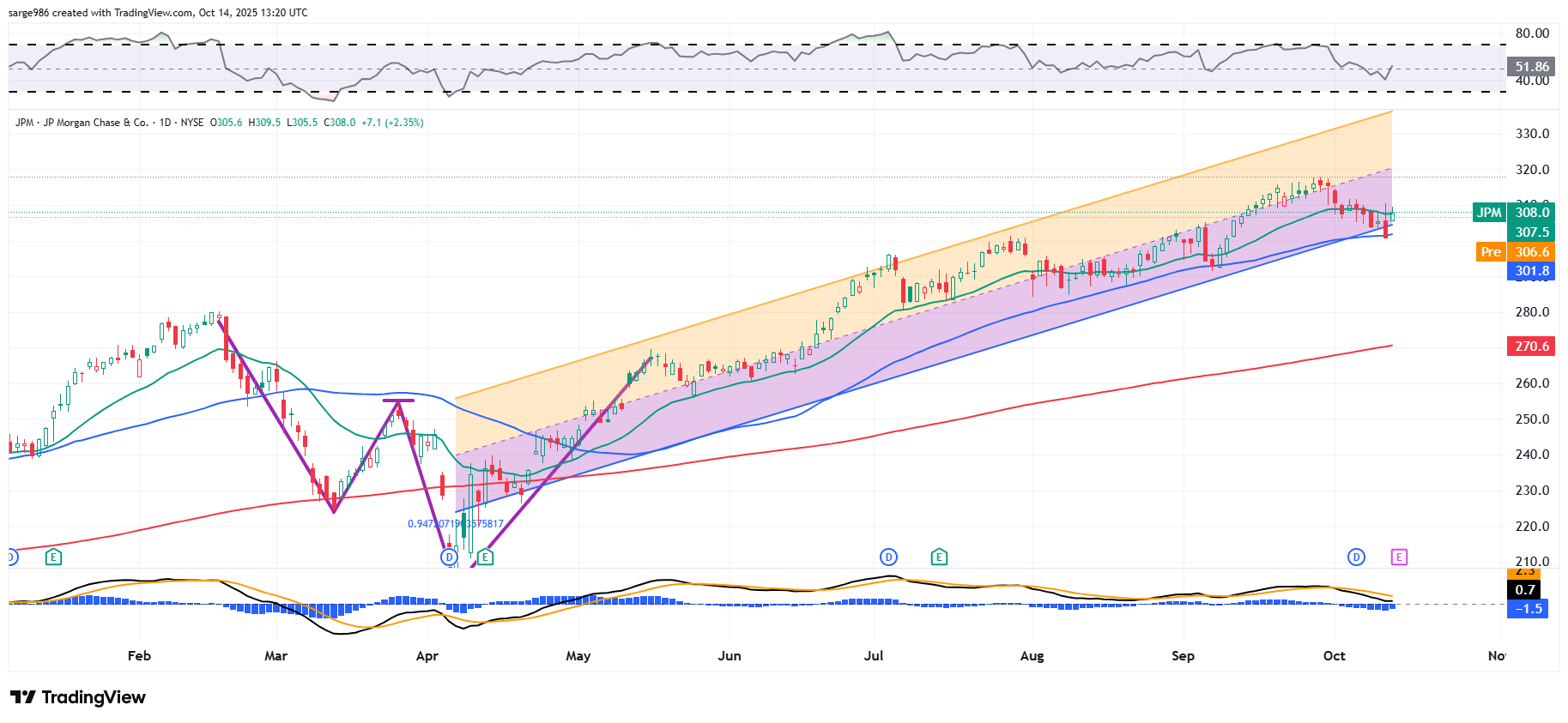

The shares of JPM are still benefiting from the double-bottom pattern of bullish reversal that we discussed in July. The stock severely tested the lower trendline of that ramp on Friday to find significant support at its 50-day SMA. On Monday, the shares rallied, but the swing crowd was unable to take the shares above their 21-day EMA after the professional crowd had defended the stock on Friday.

Looking at the indicators, relative strength is "meh," finding a home in rather neutral looking territory. The daily MACD is sending mixed to negative signals at this time. While the histogram of the nine-day EMA is now below the zero-bound (short-term bearish) and the 12-day EMA is running below the 26-day EMA (short-term bearish), both the 12-day and 26-day EMA are running above zero with the 12-day line curling upward (medium-term bullish).

I like the numbers. I don't love the chart. I am not increasing my target price at this time. Let's give it a few days to see if that recent dip turns into a head and shoulders (bearish) or a saucer (bullish).

Target Price: $320

Pivot: $256

Add: Down to 200-day SMA (currently $271)

Panic: Loss of 200-day SMA.

Note: Turn that recent activity into a saucer and I will have to increase my pivot to the recent high of $318. That would force a target price of at least $366.

At the time of publication, Guilfoyle was long WFC and JPM equity.