Sticking With This AMD Price Target After Market's Notable Reaction to Earnings

Here's my plan for Advanced Micro Devices as Wall Street analysts take a new look.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The good news? Advanced Micro Devices (AMD) is no longer a "top-five" weighted (in dollar terms) holding in the Sarge-folio. The bad news? I didn't sell any.

What happened, Sarge? Well, this is a story that needs some explaining, so let's get to it, gang. Pour yourself another cup of joe and have yourself a seat. Let's get on with it.

For the firm's fiscal fourth quarter, which ended December 27, 2025 AMD posted an adjusted EPS of $1.33 (GAAP EPS: $0.92) on revenue of $10.27 billion. These top- and bottom-line results both crushed what had been the consensus view, while the sales print was good enough for year-over-year growth of 33.8%.

The firm made sizable adjustments for both stock-based compensation and the amortization of intangible assets, partially offset by changes in the value of the firm's long-term investments.

CEO Lisa Su, who grew up in the same neighborhood in Queens, New York as your author (I did not know her, I am five years older), commented on her firm's performance:

“2025 was a defining year for AMD, with record revenue and earnings driven by strong execution and broad-based demand for our high-performance and AI platforms. We are entering 2026 with strong momentum across our business, led by accelerating adoption of our high-performance EPYC and Ryzen CPUs and the rapid scaling of our data center AI franchise.”

Operations

As sales grew 33.8%, gross profit grew 44% to $5.577 billion and gross margin popped from 51% to 54%. On a GAAP basis, operating expenses increased 27% to $3.825 billion, leaving a GAAP operating income of $1.752 billion (+101%). On an adjusted basis, operating expenses increased 42% to $3.001 billion, leaving a GAAP operating income of $2.854 billion (+41%).

After accounting for interest, other income and expenses and taxes, GAAP net income attributable to shareholders landed at $1.511 billion (+213%). That works out to $0.92 per fully diluted share, up from $0.29 for the year-ago comparison. After adjustments, the firm's net income attributable to shareholders printed at $2.519 billion (+42%), or $1.53 per fully diluted share. That would be up from the year ago result of $1.09.

Segment Performance

- Data Center generated revenue of $5.38 billion (+39.4%), producing operating income of $1.752 billion (+51.4%)

- Client and Gaming generated revenue of $3.94 billion (+37%), producing operating income of $725 million (+46.2%)

- Embedded generated revenue of $950 million (+2.9%), producing operating income of $357 million (-1.4%)

Guidance

For the current quarter, AMD is projecting total revenue of roughly $9.8 billion within a range spanning from $9.5 billion to $10.1 billion. This crushed Wall Street's expectations for something slightly below $9.4 billion. This includes an estimate for $100 million in sales of Instinct MI308 GPUs to Chinese clientele.

While that number cannot be counted on, it might also be conservative. If this projection were precise, that would amount to annual growth of 32%. The firm also sees an adjusted gross margin of 55%.

Fundamentals

For the period reported, AMD generated operating cash flow of $2.304 billion. Out of that number came capex spending of just $222 million, leaving free cash flow of $2.082 million (+90.8%). The firm does not return capital to shareholders.

Turning to the balance sheet, AMD ended the period with a cash position of $10.552 billion and inventories of $7.92 billion. That makes for current assets of $26.947 billion. Current liabilities add up to $9.455 billion including just $874 million in shorter-term debt. That places the firm's current and quick ratios at 2.85 and 2.01, which are quite robust numbers for those metrics.

Total assets amount to $76.926 billion. Of this, $41.831 billion or 54.4% are labeled as either goodwill or acquisition related intangibles. I don't love that number, but it does not impact the quality of this balance sheet. Total liabilities less equity comes to $13.927B, including long-term debt of $2.348B. The firm can take care of its entire debt load out of pocket a rough three times over.

Wall Street

Too many highly rated analysts opined on AMD overnight to go through them all on Wednesday morning. I want to note one, however, because he is one of Sarge's guys. By that I mean that I have tracked this individual for some time and trust his judgement.

John Vinh of KeyBanc is not just rated at five stars out of five at TipRanks, but is ranked at number 79 of the 12.0404 analysts rated by the service. Overnight, Vinh reiterated his "Buy" rating on AMD while increasing his target price from $270 to $300.

My Opinion

I like a lot of what I see. Sales are still growing rapidly. Profitability is expanding. Cash flows are on fire. The balance sheet is very strong. There's not much debt. Guidance is robust. The firm expects to make sales in China this quarter but is being intelligently cautious about it.

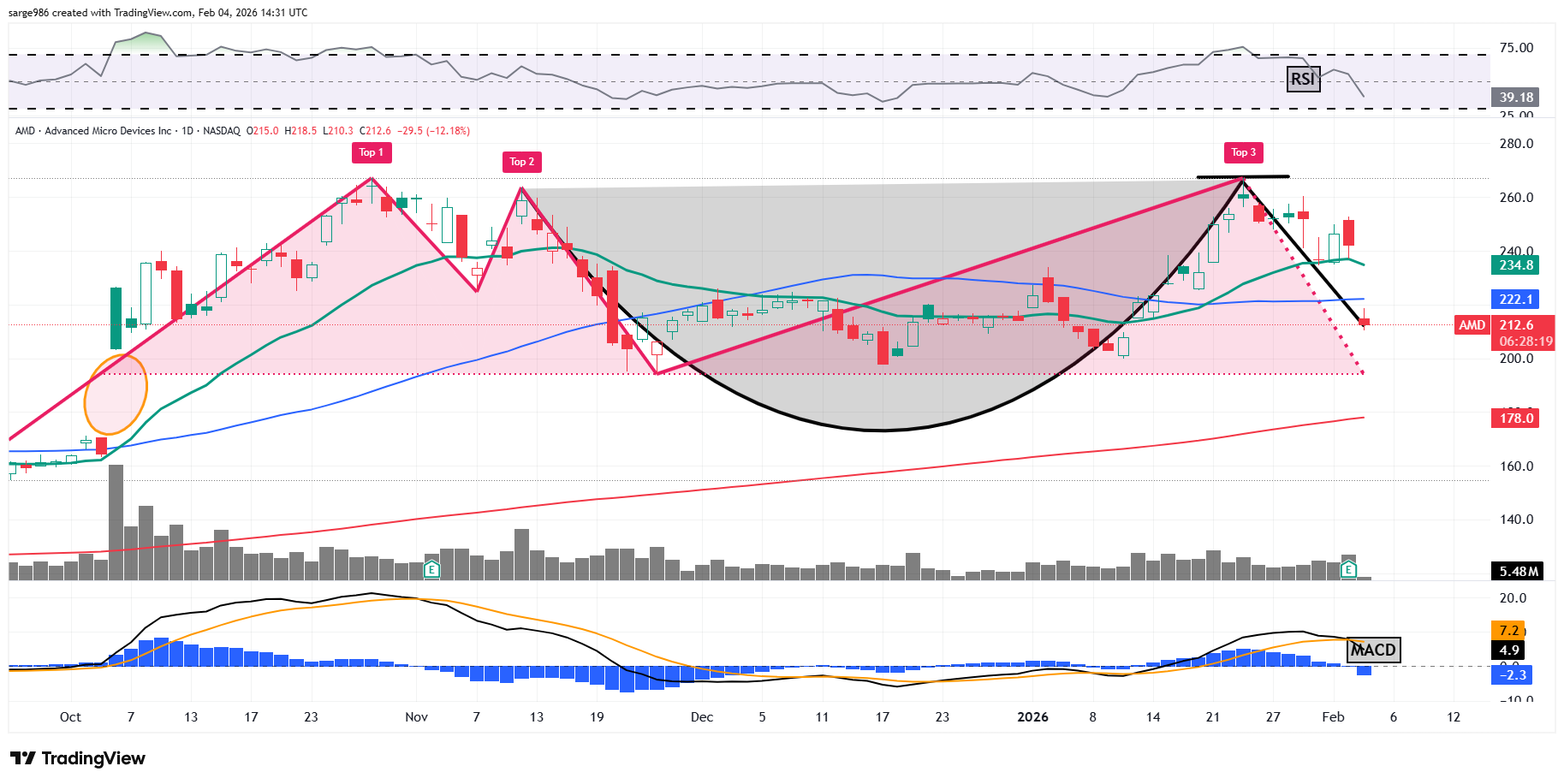

The market, though, apparently does not see AMD the way I do, or Vinh does on Wednesday morning. Let's go to the chart:

Regular readers will easily recall that just a week ago, I pointed out, on the daily chart of AMD, a cup-with-handle pattern, which is bullish, with a $267 pivot. I left that drawing on the chart for instructional purposes. I have also added the probability that the firm is now respecting what looks more like a triple-top pattern of bearish reversal more than my cup with handle.

For the bears, the downside pivot stands at $195. More importantly, the shares surrendered both their 21-day EMA and 50-day EMA at the open. This puts the unfilled gap from this past October in play. The stock would need to tick at $163.14 or lower to fill that gap. That would also involve losing the 200-day SMA, which we bulls do not want to see.

As an AMD bull who sees the firm executing at an elite level fundamentally, I need to see the stock take back that 50-day SMA either later on Wednesday or at least later this week in order to get the professionals back in line. Am I adding on this dip? Not here. I need to know that AMD is not going to make a run for that downside pivot.

I will add on a take and hold of that 50-day SMA should there be a rally later on. We do now have an upside gap to fill.

Am I changing my $320 target? Not yet. I will though, if I become convinced that the shares are developing an ascending-triangle pattern of bullish continuance. I would not yet panic on this beat down, gang. That said, if the shares do not retake that blue line by Friday, I will lighten up on my long position going into the weekend.

At the time of publication, Guilfoyle was long AMD equity.