Projecting Tesla Stock After Musk's DOGE Statement Turns Heads, Drives Pop

The electric vehicle firm is enjoying a boost after a major announcement from CEO Elon Musk about his White House plans.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

First off, for those following my overnight rental in Tesla TSLA, I took my profits (at $254.81) on that trade prior to being asked to cover Tesla's earnings, so I am flat the name. The stock has inched up after I made that sale, so, while one never looks a gift horse in the mouth, I could have done a better job in my execution.

On Tuesday evening, the EV-maker released the firm's first quarter financial results. For the three months concerned, Tesla posted an adjusted EPS of $0.27 (GAAP EPS: $0.12) on revenue of $19.335 billion. The adjusted earnings print missed badly. The revenue print missed very, very badly while reflecting a year-over-year contraction of 9.2%.

The firm suffered a decline in vehicle deliveries, partially due to the Model Y update across all four of its vehicle factories. The firm also suffered a reduced average vehicle selling price due to a poor mix, the need to push sales incentives and a negative FX-related impact. There was growth in the firm's other businesses and the firm did sport an increase in regulatory credit driven revenue.

The Real News...

Of course, the news that drove the stock higher overnight had nothing to do with the company's first quarter performance, nor the fact that the company actually pulled its fiscal 2025 full-year guidance.

It had to do with what CEO Elon Musk said during the earnings call, "DOGE work is mostly done and beginning in May, my time allocated to DOGE will drop significantly."

Shareholders all at once rejoiced in that news as from a corporate perspective, Musk's focus is needed at Tesla.

Operations

Within that total revenue that contracted 9.2% to $19.335 billion, automotive revenues contracted 20% to $13.967 billion. The Energy and Storage business produced revenue of $2.73 billion (+67%) as the services business drove revenue of $2.638 billion (+15%). Gross profit dropped 15% to $3.153 billion as gross margin fell from 17.4% a year ago to 16.3%.

GAAP operating expenses increased 9%, as operating income contracted a whopping 66% to $399 million. GAAP operating margin collapsed to 2.1% from 5.5% for the year-ago comp. After accounting for interest, taxes and other income/expenses, GAP net income printed at $409 million (-71%). That worked out to EPS of $0.12, down from the year-ago comp of $0.41. Once adjusted, net income was down 39% to $934 million. That amounts to an adjusted EPS of $0.27 versus $0.45 a year ago. Adjustments were made primarily for the expense of stock-based compensation.

Fundamentals

For the quarter reported, Tesla generated operating cash flow of $2.156 billion. Out of that number came capex spending of $1.492 billion, leaving free cash flow of $664 million. FYI, free cash flow was negative for the year-ago period. Tesla does not return capital to shareholders.

Turning to the balance sheet, Tesla ended the period with a cash position of $36.996 billion and inventories of $13.706 billion. That puts current assets at $59.389 billion. Current liabilities add up to $29.753 billion including shorter-term debt of $2.237 billion and deferred revenue of $3.243 billion. The firm's headline current and quick ratios stand at 2.0 and 1.53, which is very healthy, especially for what really is an industrial corporation. Once adjusted for deferred revenue, those ratios rise to 2.24 and 1.72, respectively.

Total assets amount to $125.111 billion, of which just $392 is intangible in nature. Total liabilities less equity comes to $44.693 billion, including another $5.292 billion in longer-term debt. The firm could easily erase all of its debt several times over, just out of pocket. This is an exceptional balance sheet.

Wall Street

Oddly enough, very few highly-rated sell-side analysts actually cover Tesla. William Stein of Truist Financial reiterated his "Hold" rating and $280 target price, while Alexander Potter of Piper Sandler reiterated his "Buy" rating and $400 target price. They are both rated at five stars by TipRanks. The four-star rated Vijay Rakesh reiterated his "Buy" rating but cut his target price from $375 to $325.

There are other well-known analysts that cover the stock such as Dan Ives of Wedbush, but his is rated at fewer than 1.5 stars out of five and I try only to cite those analysts rated at a minimum of four stars, so as to maintain the quality of my coverage for the readership.

My Thoughts

There is a lot of work to do here to restore the firm's reputation to those individuals most likely to want to purchase electric vehicles. I don't expect it to be easy. This is not a political statement, but Musk is politically aligned with an administration that most of his company's supporters or former supporters are not.

That's probably problematic and a problem that might not dissipate quickly. That said, Musk's renewed commitment to the company and less of a focus on government is welcome.

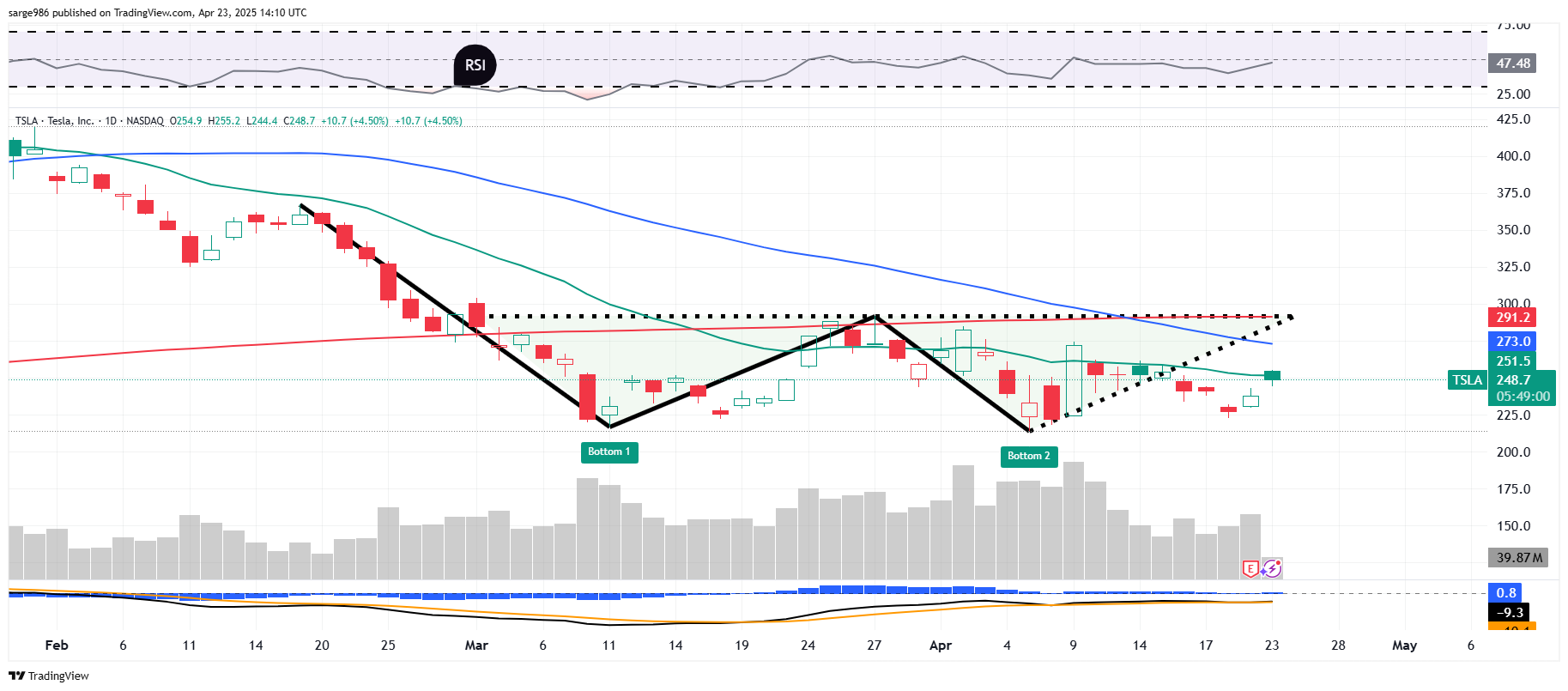

The stock is up on Wednesday but has had trouble putting together what looks like a sloppy attempt at a double-bottom pattern of reversal. The key line here is not the 21-day EMA (where the stock is now), nor the 50-day SMA, but the 200-day SMA at $291.20, which is running concurrently with the pivot that the pattern created. The pivot is 17% above the last sale.

Perhaps that should be the target, but without concrete news from the company that sounds better than what we've seen recently, that could be the higher end of the range of possibility.

At the time of publication, Guilfoyle had no positions in any securities mentioned.