Projecting a New Oklo Price Target as Nuclear Energy's Time May Have Come

I'm likely to buy into the energy name after a quarter of Department of Energy progress.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Regular readers know well that I like Oklo (OKLO) CEO Jacob DeWitte.

I've met the man. He comes off as a regular guy. Nice guy. Let me correct that: a regular, nice guy with an incredibly high IQ. I knew within about 10 seconds that I was "in beyond my depth."

Regular readers also know that, in the not distant past, we did an excellent job of trading this stock. Oklo went to the tape on Tuesday night with the firm's third quarter financial results. The numbers weren't pretty. Oklo posted a Q3 GAAP EPS of -$0.20, which was a huge miss.

Revenue hit the tape precisely where we expected, at $0 and zero cents. The stock has come a long way since the last time we talked about it. Is it time to redeploy capital toward this name? It's still a three-figure stock with no earnings and no revenue, but it is a terrific concept. Can one invest in a great idea, whose time may have come? Before you know for sure that its time will come? I can.

That said, let's dig in...

For Those Who Have No Idea

Oklo designs and deploys advanced fission power plants, For the most part, the plan is to manufacture and deliver small nuclear reactors that will provide almost limitless clean, reliable and affordable energy to data center users and the traditional grid as well.

Operations

For the period, Oklo ran up operating expenses of $36.309 million, leaving the firm with (you guessed it) an operating income/loss of -$36.309 million. The firm did recognize a $7.118 million gain in the fair value of simple agreements for future equity interests. That brought the firm's net income/loss to -$29.722 million, which works out to a GAAP EPS of -$0.20, down from -$0.08 for the year-ago comp.

That Said...

Oklo was selected during the quarter for three Department of Energy pilot program projects. The firm also has construction already underway at the Aurora facility as well as under the Atomic Alchemy Pilot Project. Fuel assembly flow testing is also underway, so far, successfully.

Fundies

For the quarter, Oklo generated operating cash flow of -$48.745 million. Out of that, capex spending of $6.255 million brought "free" cash flow to -$55 million. Obviously, there is no capital to return to shareholders.

Moving on to the balance sheet, the firm ended the quarter with a cash position of $921.6 million and current assets of $931.779 million. Current liabilities add up to just $13.803 million. You do know that a current ratio of 1.0 is traditionally considered adequate, right? This is a current ratio of 67.5. I kid you not. Even with the cash burn, Oklo can do this all year long, for many years.

Total assets amount to $1.246 billion. Too small of an amount of this is in intangibles for me to give a darn. Another $261.9 million of this is in marketable investments that could add to the cash position in an emergency. (So, the real current ratio is actually even more muscular.) Total assets less equity comes to $40.633 million.

There is no debt load of any kind anywhere on these books. I may be biased, because he impressed me, but DeWitt and his wife, co-founder Caroline DeWitt (the COO), may really be on to something. These two geniuses met at MIT in grad school where they both studied nuclear engineering. They are operating on another level.

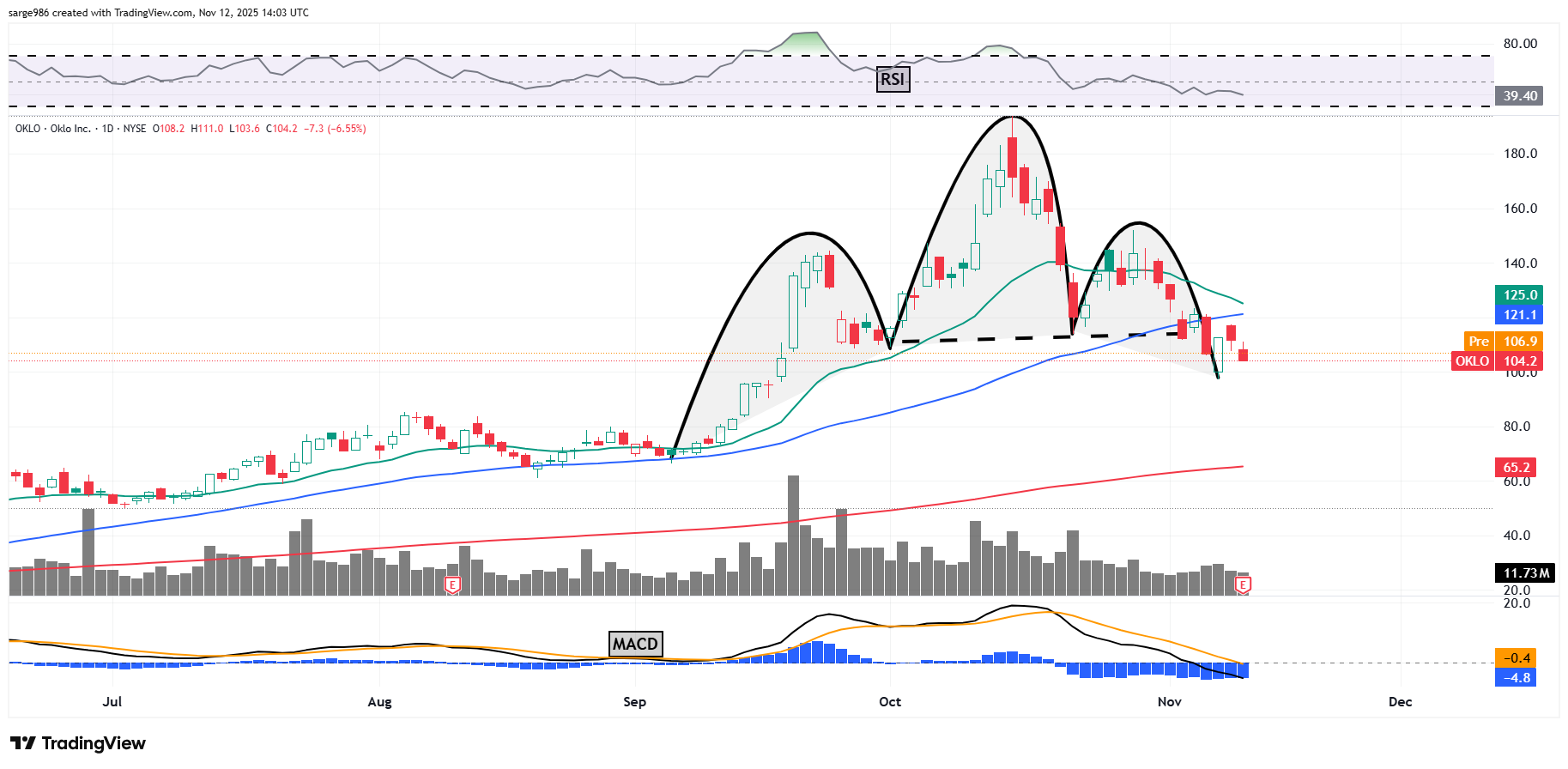

The Chart

What you see below will determine how you feel, technically, about this stock. Do you see a head-and-shoulders pattern of bearish reversal?

If you do, the pivot would have been $114. This stock bottomed a few days ago at $97.06. My downside target coming out of that pattern would have likely been in the low- to mid-$90s. The indicators are already in awful shape. Relative strength is weak. The daily MACD looks like it was beaten severely with the "ugly stick."

My thoughts? There could be more downside. The firm still has no sales, but what they do, I believe, will become more of a necessity than a luxury. I see a different pattern developing as the above-mentioned head-and-shoulders pattern ages. Take a look:

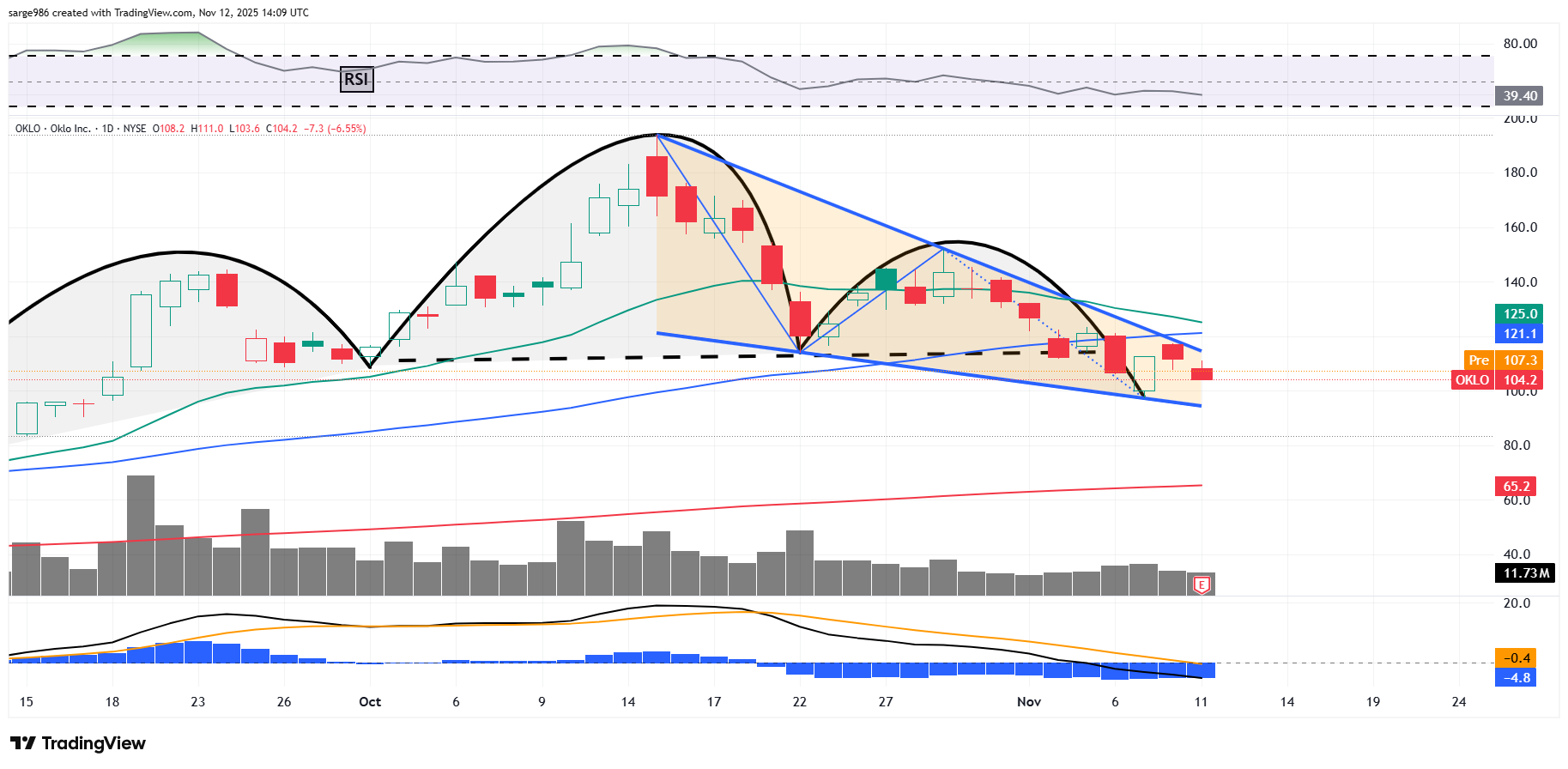

Has the second half of the head-and-shoulders pattern of bearish reversal given birth to a falling-wedge pattern of bullish reversal? I think it very well may have. Buy the shares on Wednesday? I may initiate with something small. The real trigger for those of us who make our living off of these markets will be if the stick can break out of this pattern.

The upper trendline of the falling wedge currently stands at $114. I kid you not. The 50-day SMA stands at $121. Either or both of these could act as upside pivots. That means that they could show up as either resistance or act as an upside accelerant.

That would put my target price, if I initiate, which I am likely to do, up around $136, conservatively. I could make a technical case for $151.

At the time of publication, Guilfoyle had no positions in any securities mentioned.