Palo Alto Networks Could Be Pre-Earnings Buy After Acquisition News

With the cyber security sector offering trade war resistant demand, the firm might be worth adding.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

This is an area that I have identified as one that will not likely be seriously impacted by any trade war and an area also likely to benefit from long-term inelastic demand going forward. I had been long two names in the space for quite some time. Those names would be CrowdStrike Holdings CRWD and SentinelOne S. I consider CrowdStike to be "best in class" across the space. Everyone who reads me knows that.

That stock is my third-largest holding in terms of portfolio weighting, behind only Palantir Technologies PLTR and SoFi Technologies SOFI and just ahead of fourth place Rocket Lab USA RKLB. Yes, last week was incredible. The S&P 500 was up 4.5% last week. This book was up several times that.

That said, SentinelOne was not part of my fourth week of April rally party. That one I had jettisoned as I narrowed my book when markets started caving several weeks back. What does that mean? It means that I have room on my pad for a second cyber security stock. SentinelOne, I had thought to be an up and comer. The technology is solid, but the stock struggled, It underperformed the rest of my book. I have enough cash on hand to be flexible. Perhaps I look somewhere else for increased exposure to the space.

Palo Alto Networks

The name that I used to consider "best in class" and still consider to be right there is Palo Alto Networks PANW. This name will report on or about May 19, about 10 days ahead of CrowdStrike. Wall Street is looking for an adjusted EPS of $0.77 on revenue of roughly $2.3 billion. This would compare to $0.66 for the year-ago period on earnings growth of almost 15%.

Of the 35 sell-side analysts of all rankings that cover PANW, 28 have increased their earnings estimates since the start of the first quarter. Most readers may not recall that, back in February, Palo Alto projected Next-Generation Security ARR of $5.03 billion to $5.08 billion for the quarter about to be reported and remaining performance obligation of $13.5 billion to $13.6%. These numbers would be good for growth of 33% 34% and 19%/20%, respectively.

How these metrics print and how they look going forward will likely be as closely watched as the headline numbers on adjusted profitability and sales growth. Other than that, the firm has a very strong balance sheet and has consistently (six straight quarters) produced operating cash flow of more than $3 billion on a 12-month trailing basis.

News

On Monday morning, Palo Alto announced that the firm had entered into an agreement to acquire startup cyber security operation Protect AI. Palo Alto executive Anand Oswal commented:

"By extending our AI security capabilities to include Protect AI's innovative solutions for Securing for AI, businesses will be able to build AI applications with comprehensive security. With the addition of Protect AI's existing portfolio of solutions and team of experts, Palo Alto Networks will be well-positioned to offer a wide range of solutions for customers' current needs and also be able to continue innovating on delivering new solutions that are needed for this dynamic threat landscape.”

Terms of the deal have not yet been disclosed.

Jump in Ahead of Earnings?

Maybe. I know that sounds non-committal. It's not. Let me explain. PAWN has just experienced a "death cross" where the 50-day SMA crossed below the 200-day SMA. That does not really scare me the way it used to. That said, the stock is in the process of developing an inverse head-and-shoulders pattern while making an attempt on that very same 200-day SMA.

I know, the inverse head-and-shoulders pattern is a bit anticipatory on my behalf. That said, taking and holding the 200-day SMA could very well force portfolio managers to take on greater long side exposure. Readers will note that relative strength (above the chart) is improving as the daily MACD (below the chart), while not yet bullishly postured, is no longer bearishly postured as the 12-day EMA has crossed above the 26-day EMA.

What Am I Thinking?

I'm thinking maybe I grab some shares on momentum as the 200-day SMA is taken and held. I am also thinking that should the stock fail at the 200-day line, that the swing crowd might make a stand at the 21-day SMA and with them so shall I.

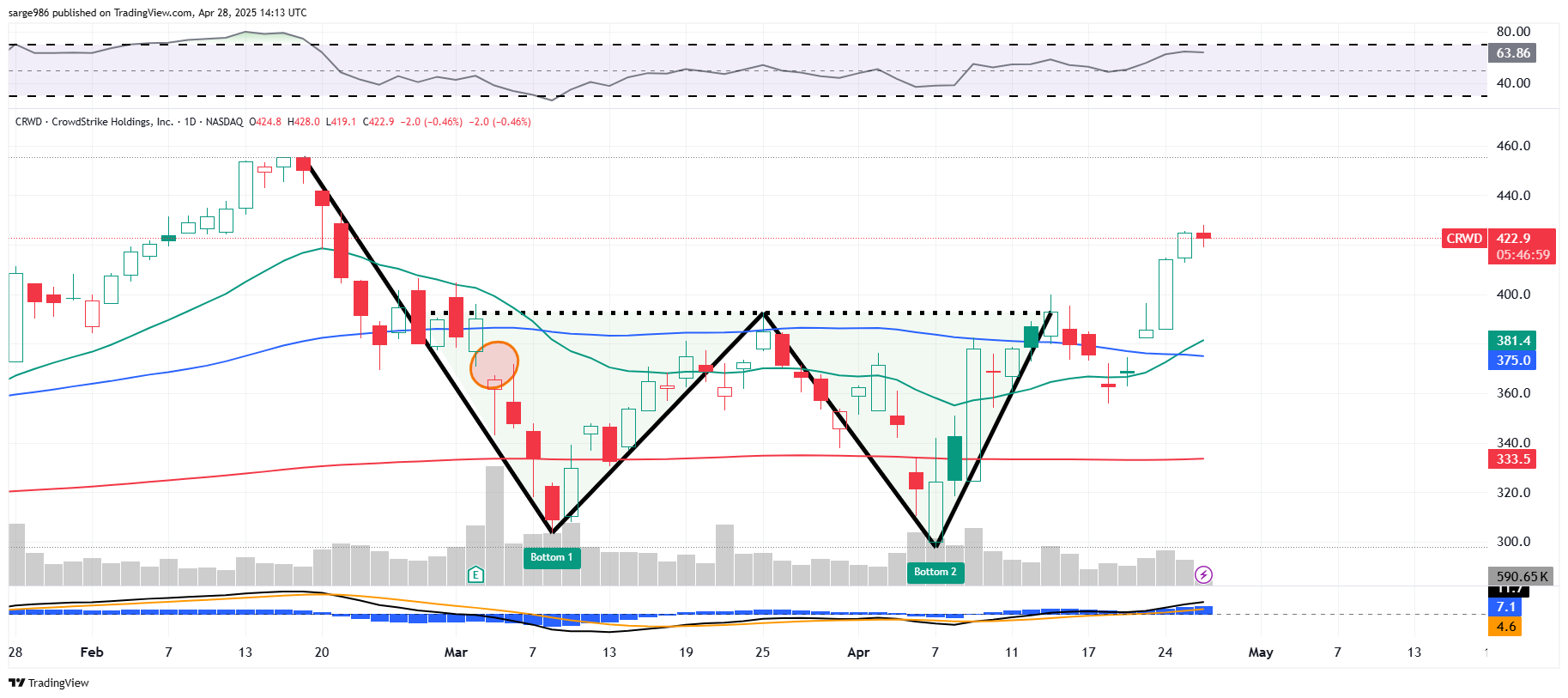

On CrowdStrike...

Look at that breakout! My $475 target price (from last Friday's "Market Recon") stands.

At the time of publication, Guilfoyle was long CRWD, PLTR, SOFI and RKLB equity.