Palantir Price Target After CEO Sends 'Deranged' Message to Detractors

The AI firm's balance sheet rocks, yet the stock got rocked after earnings.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Palantir (PLTR) rocks. Yet, the stock got rocked. This is that story.

The mightiest of them all when it comes to big-data-driven, cloud-based AI software, Palantir Technologies went to the tape with the firm's third quarter financial results on Monday afternoon. Palantir knocked the cover off of the ball. Really. The firm posted an adjusted EPS of $0.17 (GAAP EPS: $0.18) on revenue of $1.181 billion. The firm easily beat expectations for those top-line and bottom-line (adjusted or not) results. The sales growth print was good for year-over-year growth of 62.6%.

This was an impressive ninth consecutive quarter of accelerating year-over-year revenue generation from the quarter prior. For the quarter, the firm closed 204 deals of at least $1 million, 91 deals of $5 million and 53 deals of $10 million as the customer count grew 45% year over year and 7% sequentially. U.S.-driven sales grew 77% to $883 million. Within that number, U.S. commercial sales increased 121% to $397 million, while U.S. government sales increased 52% to $486 million.

The Rule of 40

For those unaware, the "Rule of 40" is a quick way to determine if a company is appropriately balancing growth and profitability. Simply put, if a company's annual growth rate and profit margin add up to at least 40, a stock is more or less unofficially declared a "growth stock" and, for investors, extended valuations are often overlooked.

From the press release, CEO Alex Karp commented on this:

“114% - our Rule of 40 score! These results make undeniable the transformational impact of using AIP to compound AI leverage. Year-over-year growth in our U.S. business surged to 77%, and year-over-year growth in U.S. commercial climbed to 121%. We are yet again announcing the highest sequential quarterly revenue growth guide in our company’s history, representing 61% year-over-year growth.”

More from Karp

In his letter to shareholders, Karp took a not-so-veiled shot at his firm's naysayers:

"Some of our detractors have been left in a kind of deranged and self-destructive befuddlement. It has indeed been difficult for outsiders to appraise our business, either its significance in shaping our current geopolitics or its value in the vulgar, financial sense. The reality is that Palantir has made it possible for retail investors to achieve rates of return previously limited to the most successful venture capitalists in Palo Alto. And we have done so through authentic and substantive growth."

Operations

As revenue generation increased 62.6% to $1.181 billion, the cost of that revenue grew 41.4% to $207.307 million. That left a gross profit of $973.785 million (+40.6%) as gross margin improved from 79.8% to 82.5%. GAAP operating expenses grew 24.7% to $580.529 million, leaving GAAP operating income of $393.256 million (+247.9%). After accounting for interest, other income and expenses and taxes, GAAP net income printed at $476.748 million (+219.2%). This works out to $0.18 per fully diluted share, up from $0.06 for the year-ago comparison.

After adjusting for stock-based compensation, operating income becomes $600.54 million (+118%) and operating margin becomes 51%, up from 38%. Adjusted net income becomes $528.709 million, which works out to $0.21 per fully diluted share, up from $0.10 for the year-ago period.

Guidance

For the current quarter, Palantir projected revenue of $1.327 billion to $1.331 billion, which comes to $1.329 million at the midpoint. That would be good for year-over-year growth of 61%. This easily crushed the $1.18 billion that Wall Street was looking for. Adjusted operating income is seen at $655 million to $697 million.

For the full year, the firm is expecting to drive revenue of $4.396 billion to $4.4 billion or $4.398 billion at the midpoint. That would be good for annual growth of 53% and again crushed consensus view, which had been for $4.16 billion. The firm also sees U.S. commercial revenue growth of 104%, up from guidance for 85% growth three months ago. Adjusted operating income is projected at $2.15 billion to $2.16 billion, up from the previous view for $1.91 billion to $19.2 billion. Adjusted operating full year free cash flow is now projected at $1.9 billion to $2.1 billion up from prior guidance of $1.8 billion to $2 billion. Simply put, the guidance is spectacular.

Fundamentals

For the quarter reported, Palantir generated operating cash flow of $507.664 million. Out of that number came $6.792 million in capex spending but added were $38.99 million in cash paid for payroll taxes related to stock-based compensation. This puts free cash flow for the period at $539.862 million (+24.3%). The firm does not return capital to shareholders.

Looking at the balance sheet, Palantir ended the period with a cash position of $6.438 billion and current assets of $7.586 billion. Current liabilities add up to $1.18 billion, which does include deferred revenue and customer deposits of $684.892 million. At the headline, the firm's current ratio stands at 6.43, which would make Palantir's balance sheet the envy of almost the entire S&P 500. Adjusted for those deferred revenues and deposits, Palantir's current ratio stands at an unreal 15.3. One word: incredible.

Total assets amount to $8.114 billion, which as we like, includes nothing intangible. Total liabilities less equity comes to $1.426 billion, which includes another $45.472 in deferred revenues/deposits. The firm has absolutely no debt on the books. This might be the cleanest, strongest, most professionally managed, most fiscally disciplined balance sheet that I have ever seen in my four-decade career.

Wall Street

I am not going to go through the list because just about everyone who covers the stock has increased their target price since Monday night, even Brent Thill of Jefferies who has been consistently wrong on this name since the get-go. Thill is rated at five stars by TipRanks, by the way. He is not awful at his job. He is just awful at analyzing Palantir.

The one to pay attention, besides myself and Chris Versace, on this name is Mariana Perez Mora of Bank of America, who has been right on PLTR since the beginning. Perez Mora, who is also rated at five stars by TipRanks, reiterated her "Buy" rating while taking her target price up to a (now) Wall Street high $255 from $215.

My Thoughts

What's not to like? I mean beside the stock's valuation, which is undeniably extended.

The fundamentals are the stuff guys like me dream of. Sales are running wild as are margins. The commercial business is exploding. Cash flows are not just robust, they are enormous. The balance sheet is simply the greatest balance sheet I can remember seeing. The CEO is focused and aggressive. There is nothing in the fundamentals that is even a little bit winky. Palantir is kicking the living heck out of the competition if there is anyone out there that can even be referred to as competition.

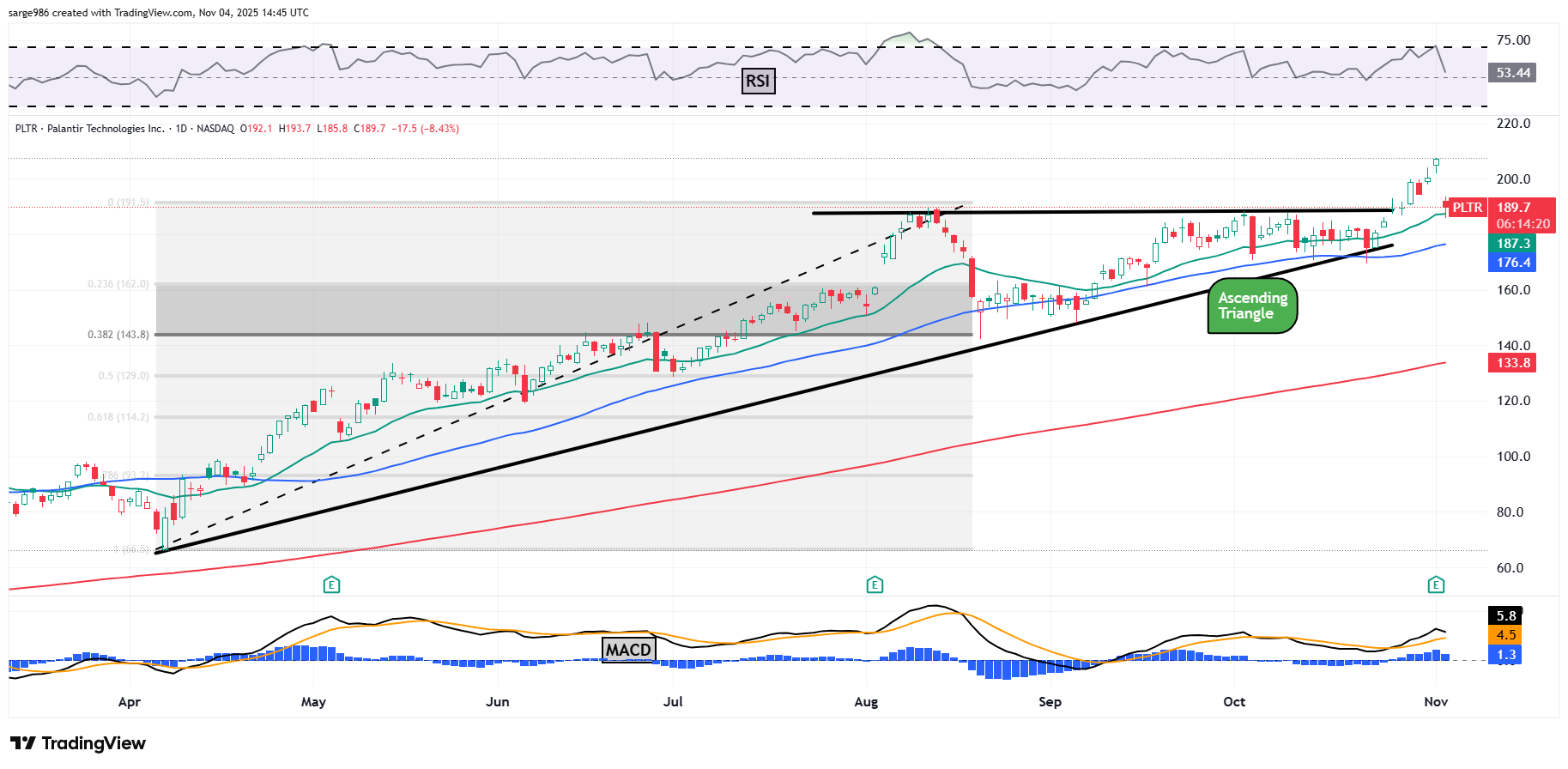

On Tuesday morning, the stock has given up its breakout from the ascending triangle pattern of bullish continuance that I showed you. Sure, Tuesday morning's beatdown feels lousy but the stock is only giving up about a week of gains. So far, the swing crowd has defended the stock where they had to, at the 21-day EMA. The 50-day SMA remains considerably lower. That's where the pros will be asked either to defend or not to defend the name.

Relative strength is still better than neutral and the daily MACD, even while sagging this morning, still has all three components in positive territory and the 12-day line running well above the 26-day line. This is all still bullish.

My Plan

I told readers on Tuesday morning that I made a sale on Monday night after the stock popped to the upside and I did. I intend to repurchase those shares shortly (after publication) hopefully more than $20 below where I sold them. That will restore PLTR to its rightful weighting on my book. The stock may need to base or consolidate. Do not be surprised if this is how the short-term future develops. Still, Karp is easily a top five CEO in the U.S., and you know that I invest in CEOs.

Target Price: $226 (reiteration. For the first time in a very long time, I am not the Wall Street high)

Pivot: $188 (still)

Add: Down to the 50-day SMA (currently $177)

Panic: Loss of the 200-day SMA (currently $134)

At the time of publication, Guilfoyle was long PLTR equity.