Ondas Is Worth Some Speculation But Here's Where I'd Exit

The wireless connectivity firm seems worthy of a speculative investment but there's potential for a point at which I'd exit the stock.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Who? Good question. This comes at the request of one of our readers.

Ondas Holdings (ONDS) is a provider of wireless, drone and automated data solutions through the firm's wholly owned subsidiaries. The Boston-based company operates through two segments. Those would be Ondas Networks and OAS.

Ondas Networks is a provider of wireless connectivity that enables mission-critical industrial internet applications. This business unit designed, developed, manufactures and supports "FullMAX," which is the firm's software defined radio platform. This platform provides and allows for the operation of private, wide-area broadband networking services.

The OAS segment integrates drone-based solutions with a focus on high-performance, critical applications governmental and Tier-1 commercial clientele. Commercially available platforms include Optimus and the Iron Drone Raider.

The Iron Drone leverages the expertise of Airobotics in developing a fully autonomous drone system. Airobotics is a fully owned Israeli subsidiary of Ondas. In the U.S., the Iron Drone system is sold through its sister company, American Robotics, another Ondas subsidiary. This platform is a response to the needs of the modern battlefield. Not just what we have seen in the Middle East, but what we have watched unfold in Eastern Europe.

The Numbers

For the firm's third quarter, which will hit the tape on Thursday morning, Ondas is expected to post a GAAP EPS of -$0.05 on revenue of slightly more than $7 million. That would compare quite well to the year-ago comps of -$0.15 and $1.48 million. Of the seven analysts that I know who cover the stock, three have revised their earnings estimates lower since the start of the quarter, two have revised the estimates higher and two estimates were left where they were. The entire range of revenue estimates spans from $6 million to $9 million. The firm has never generated revenue of more than $6.27 million before, so this five-year public company is still really in its embryonic stage.

Fundies Going In

Obviously, we'll have more data within a day, so this information is stale at three months of age. The firm burned a little less than $33 million over the past 12 months as of June. At that time, the firm had $67.6 million in cash on the books and current assets of $91.2 million. Current liabilities added up to $31.5 million, of which $16.2 million was in shorter-term debt, but $4.3 million was in unearned revenue which is not usually a true financial obligation.

Total assets amounted to $152 million. About $52.9 million of that was in goodwill and other intangibles. At almost 35% of total assets, that might be a bit much for a company that is yet to build its reputation. Total liabilities less equity comes to $39.3 million. That includes trace amounts of longer-term debt and non-current unearned revenue. The firm's balance sheet is in good shape for now. That said, the cash burn has to slow or the cash position has to grow.

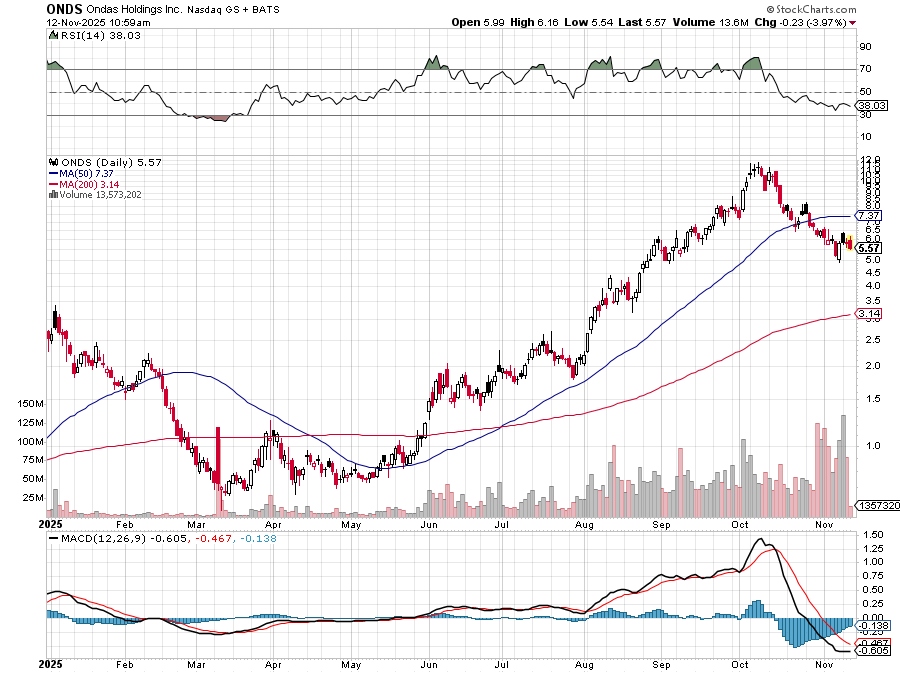

The Charts

Here, readers will see that ONDS has traded as low as $0.57 and as high as $11.70 all in calendar year 2025. One might see this as "meme stock" like activity but just 13% of the entire float is held in short positions. That's not a low percentage, but it's not ridiculous either.

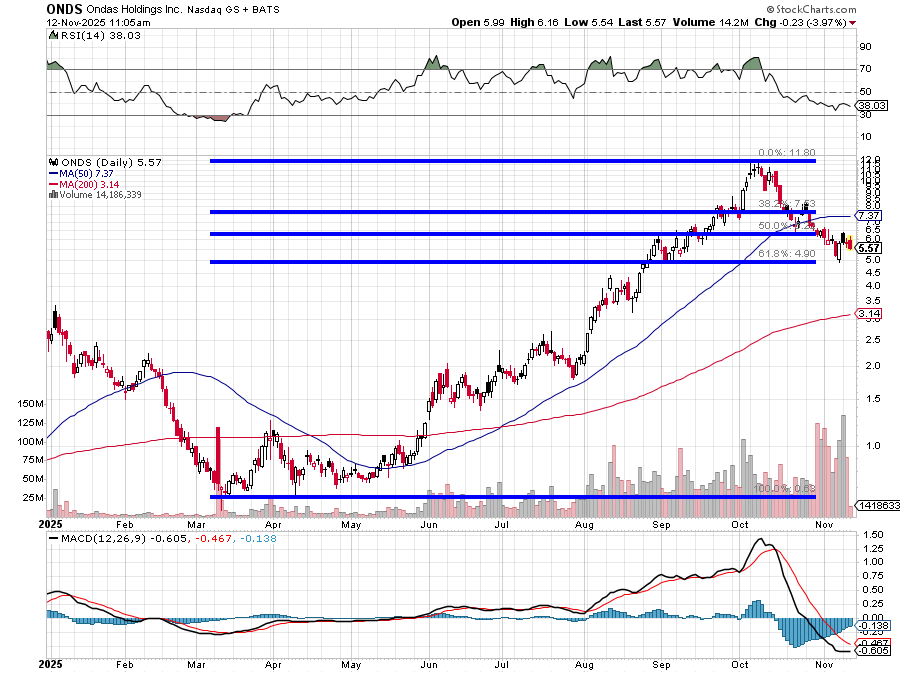

We see here that despite a weakish reading for relative strength and a horrific looking daily MACD, that the stock did find recent support at the 61.8% Fibonacci sequence retracement level of the March through October rally. What now? Head and shoulders? I don't really see it. I do see something potentially positive though:

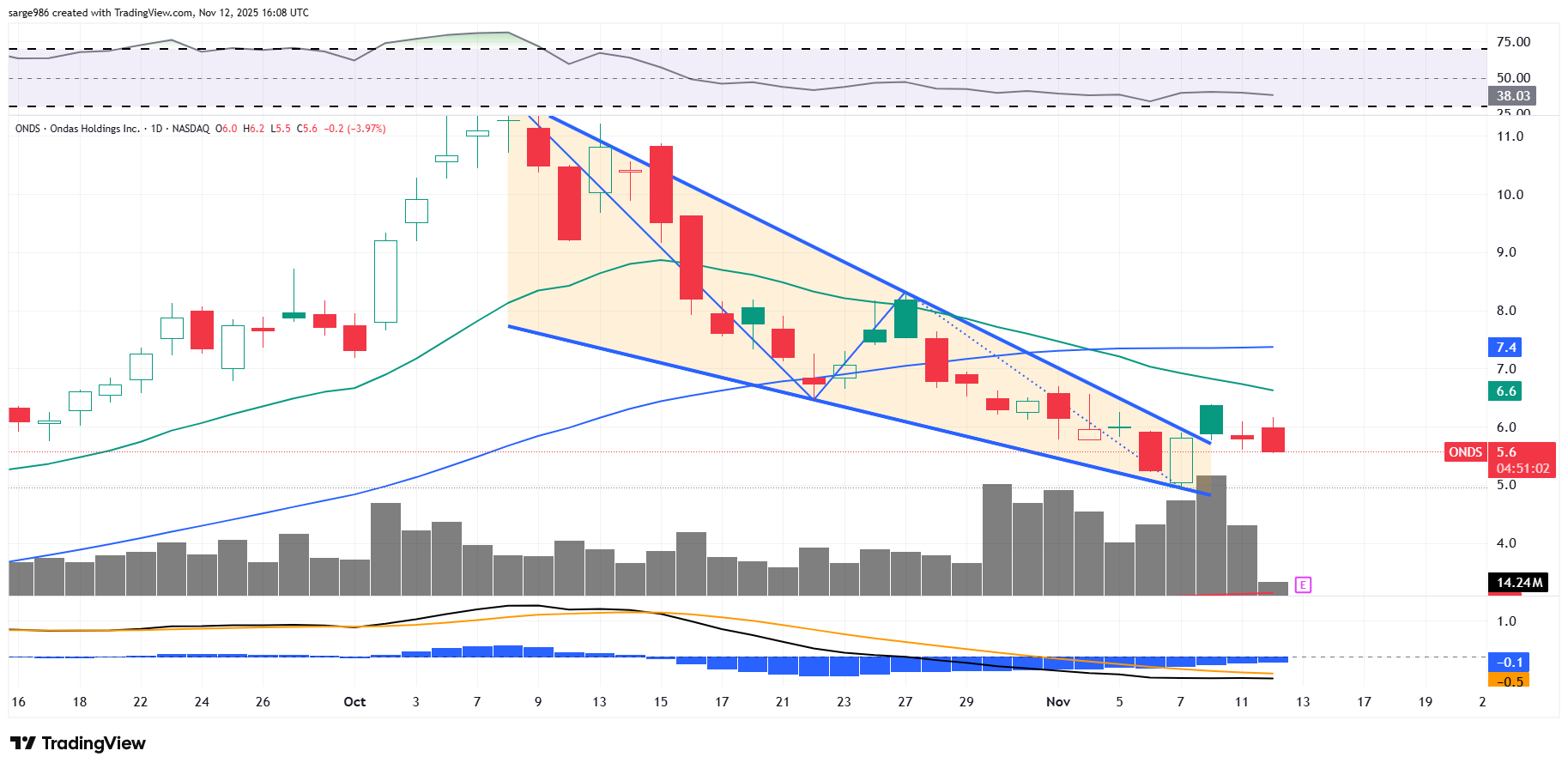

ONDS is trying to put in a floor and break out of a falling wedge of bullish reversal. On Monday, the stock broke out past the upper trendline of the model. These past two days have been spent trying to hold that line.

Is this stock worthy of speculation? Yes, in my opinion, but not with the rent money. What really matters is what ONDS can do as the share price makes a new approach on the 21-day EMA and 50-day SMA.

Why do I think it worthy of speculation? Look at the increased trading volume since late October. Somebody big defended the stock at these levels. Should the stock make a new post November 7 low, I take my football and I go home. (That means I get out of the stock.)

At the time of publication, Guilfoyle had no positions in any securities mentioned.