New Intel Price Target After Acquisition News Turns Heads

We've got a target price and pivots in mind as the chip maker's stock reacts to the possibility of a split up.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

I'm not going to lie. I jumped in on Intel INTC as the stock sunk to its lows.

I got aggressive in the wake of former CEO Pat Gelsinger's "retirement " back in the very early days of December 2024. The stock moved lower from there. I had a few folks doubt my wisdom on this trade. I doubted my own wisdom. My thoughts? Intel had performed so poorly relative to the rest of the semiconductor space as tech dominated the financial markets over the past few years.

The underperformance of the firm goes back well before Gelsinger's run. He just became the poster boy for the firm's impotence in taking meaningful share away from their competitors in key markets, as those competitors took meaningful share away from Intel where Intel was strong.

While firms like Advanced Micro Devices AMD ate Intel's lunch in the PC market, Nvidia NVDA dominated the market center/cloud, generative AI and gaming spheres, while firms like AMD, Broadcom AVGO and Marvell Technology MRVL also played those games.

Intel even tried to restart its foundry business under Gelsinger and did land a key contract with Amazon AMZN. Still, the firm failed, even with plenty of government assistance, to take a large slice of a pie that is dominated by Taiwan Semiconductor TSM. Maybe news stories, like the one that broke at The Wall Street Journal's website over the weekend, were inevitable. Maybe other semiconductor industry players would start looking at what parts of Intel they might benefit from taking a run at, while the firm continues to limp along without a chief executive.

The Intel Headlines

On Saturday morning, Asa Fitch, Lauren Thomas and Yang Jie of The Wall Street Journal broke a story where both Taiwan Semiconductor and Broadcom had each been considering making separate runs at parts of Intel's business that might benefit those firms.

Broadcom is said to be considering Intel's chip design and marketing businesses and has held informal discussions with its own advisors concerning making a bid for those parts of the firm as long as a buyer can be found for Intel's foundry business. This is interesting because the article also claims that Taiwan Semiconductor, easily the world's largest wafer foundry for computer chips, has been studying the idea of taking over control of either all or part of Intel's fledgling manufacturing business.

The potential fly in that ointment is that Intel has taken large chunks of federal money as, under both presidents Biden and Trump, a preference has been made public for the re-shoring of chip foundry services.

As a means toward not losing the business of U.S. chip designers, Taiwan Semi has also accepted federal funds and has built out large facilities in Arizona in order to produce those chips on U.S. soil. Still, this is a foreign-owned firm, and Intel is just one of two smaller U.S. chip foundries, the other being GlobalFoundries GFS. The federal government would have to sign off on any splitting up of Intel where one side of the firm ends up under the control of a foreign owned business. It is being said that the Trump administration may be either involved or at least in the loop as far as talks between Taiwan Semi and Intel are confirmed.

Intel Earnings

Back on January 30, Intel posted an adjusted EPS of $0.13, and a GAAP EPS of $-0.03 on revenue of $14.26 billion for the fourth quarter. The adjusted print was a slight beat, but the guidance was awful.

Intel guided current quarter revenue towards a range of $11.7 billion to $12.7 billion, with consensus at the time up around $12.85 billion to $12.9 billion. The firm also projected an adjusted EPS for the current quarter of $0.00, and a GAAP EPS of $-0.27, with Wall Street looking for something more like $0.09, adjusted. So, maybe Intel is desperate. Maybe Intel does need the likes of Taiwan Semi and Broadcom to come to the rescue. One does think that if running this shop were an attractive position that we would have heard rumblings by now of someone preparing for or at least interviewing for the job and that a stronger candidate than Pat Gelsinger would have been hired last time around.

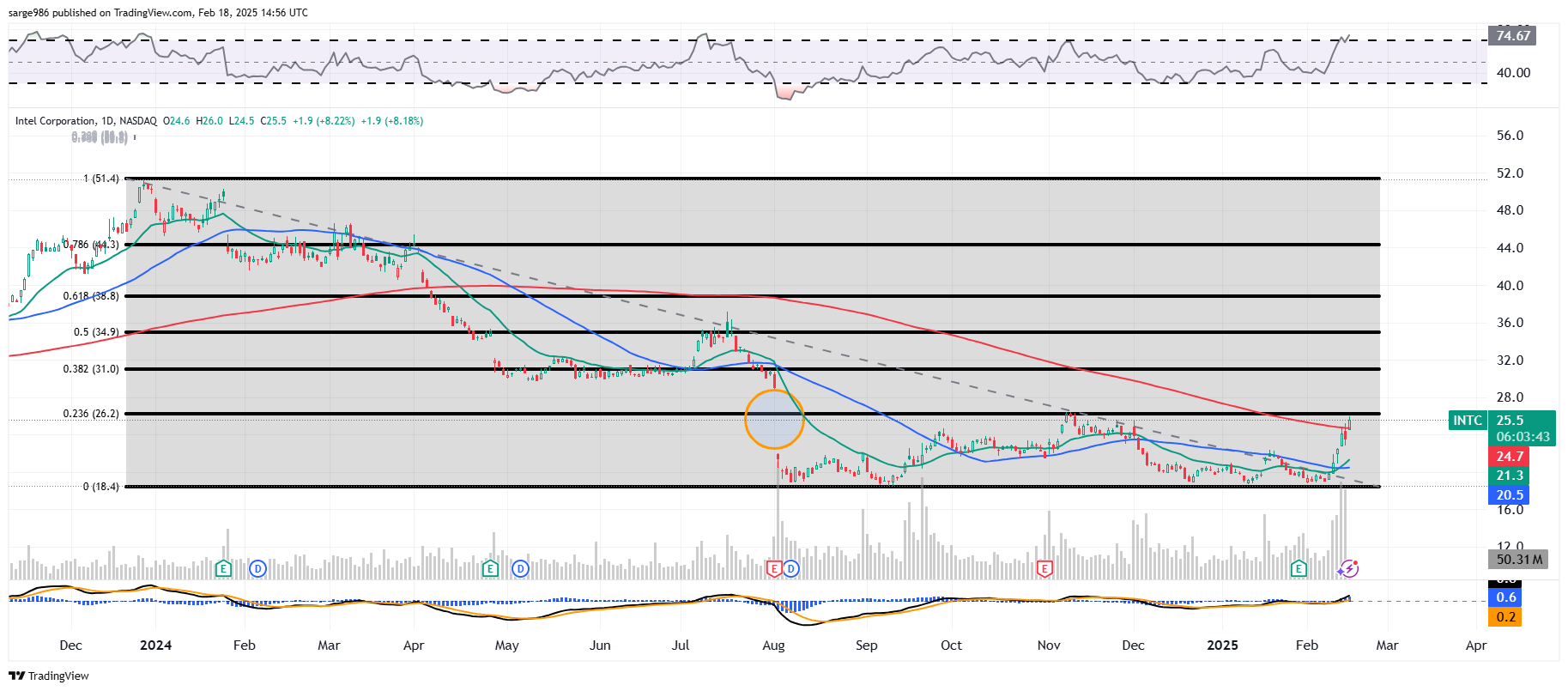

Intel Stock Charts

We all know how INTC has fallen out of bed since late 2023/early 2024. There is that unfilled gap created this past summer that still draws attention. We also have placed a Fibonacci retracement model over the stock's performance over that timeframe. The stock has found support in between $18 and $19 on numerous occasions since this past August. Now, the stock must contend with the 23.6% Fibonacci retracement level of the entire sell-off as this news brakes. Let's zoom in:

As late 2024 stretched into early 2025. INTC developed a "triple-bottom pattern" which is a bullish pattern of reversal. That was a chance to load up a bit at a confirmed support level. The pivot for this pattern had been just about $22.40, which is where the apex in between bottom two and bottom three hit the tape. A secondary pivot has arrived at the 200-day SMA. Relative strength is rather positive which is a nice change for this stock, as the daily MACD has suddenly turned bullish. Does all of this positivity fall apart if there are no deals reached? Very possibly. This is a medium-term trade, not an investment.

Intel (INTC) Target Price

Target Price: $31 (gap filled and more)

Pivot One: $22.40

Pivot Two: $24.70 (200-day SMA)

Add: Down to 50-day SMA ($20.50

Panic: New low below the triple-bottom pattern

At the time of publication, Guilfoyle was long INTC, NVDA and AMZN equity.