New Highest Rocket Lab Price Target Amid Accelerating Success

We've got a new plan for the aerospace firm following an $800 million contract announcement and a surge.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Tuesday, long-time core "Stocks Under $10" and Sarge-folio holding Rocket Lab (RKLB) rallied for a 10.1% gain to close at $86.03.

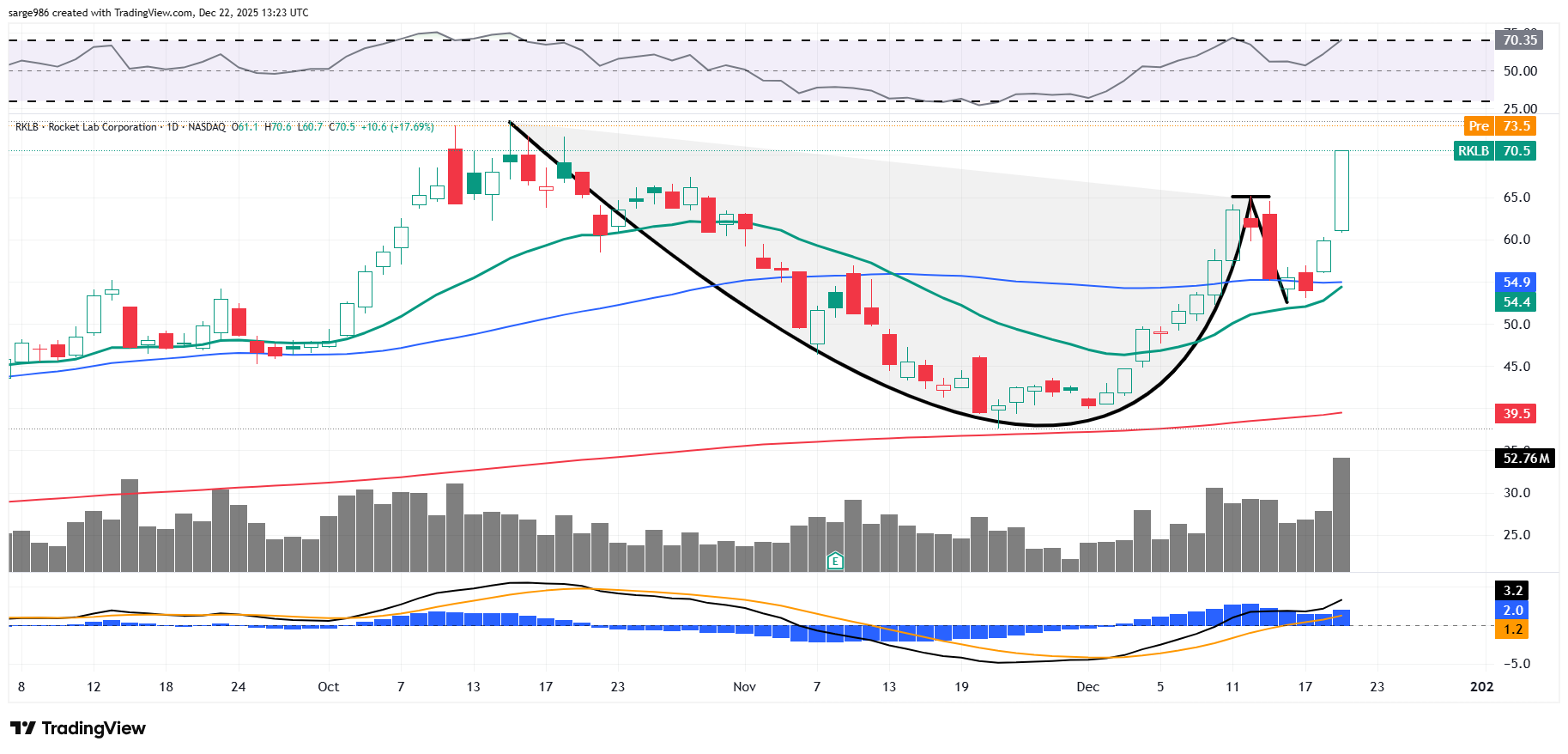

Readers may recall the $81 target price that I had put on the shares back on Monday, December 22, a little more than two weeks ago. The stock's last sale was $70.52 at the time. RKLB is up 22% since then and up 129% from its late November low. It does mean that I have to take a little something off. That's the rules. Go team.

That piece came after news had broken that the firm had been awarded a prime contract by the U.S. Space Force Development Agency to design and manufacture 18 satellites for the tracking layer Tranche 3 program under the Proliferated Warfighter Space Architecture.

That contract, which is worth $816 million, will have Rocket Lab delivering satellites equipped with advanced missile warning systems as well as tracking and defense sensors. This program will provide global, persistent detection and tracking of emerging missile threats and will be capable of detecting hypersonic weapons. The next day, analyst Ryan Koontz of Needham, who is rated at five stars out of five by TipRanks, reiterated his "buy" rating while increasing his target price from $63 to $90. This past Monday, Rocket Lab announced a planned meeting with Koontz to be held in New York City on Tuesday, January 13.

Earnings Update

Rocket Lab will not report its fourth quarter until late February, so we are a way off at this time. Currently, Wall Street is looking for an adjusted EPS of -$0.05 (GAAP EPS: -$0.10) on revenue of roughly $177.5 million. This would be a slight improvement over the adjusted -$0.06 (GAAP EPS: -$0.10) posted for the year-ago comparison on annual sales growth of 34.1%.

For the full calendar year of 2026, consensus is for a GAAP EPS of -$0.24 on revenue of $879.5 million. That would be significantly better than 2025's estimated (with Q4 still up in the air) -$0.38 on year-over-year revenue growth of close to 47%. The firm's success does appear to be accelerating.

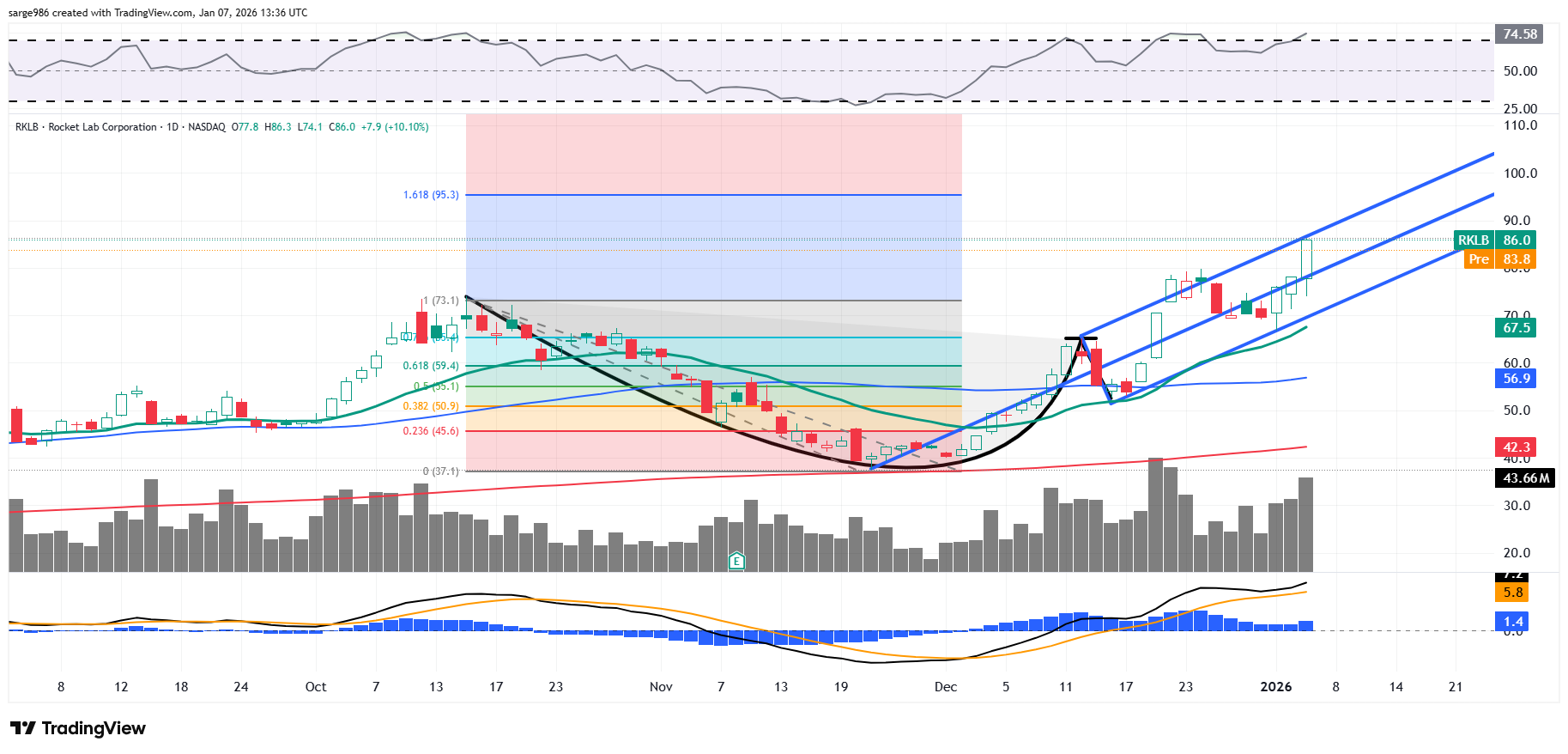

The Chart

Just a heads up: There is some profit taking going on in RKLB overnight and in pre-opening trade that will likely carry into the regular session. Let's take a look at the chart:

This is the cup-with-handle pattern that I showed readers back on December 22 that at that time was starting to produce the breakout that led to the target price that was breached on Tuesday.

If we take this breakout and apply both an Andrews' pitchfork model and a Fibonacci extension model to the chart, we see that the shares were halted at the upper trendline of the pitchfork. If this moving line is to become our new pivot, that would put my target price at $103. If I lean on the extension model, the target would be a more modest $95.

Either way, we have a reading for relative strength that is now in technically overbought territory, but it got there on elevated trading volume and the daily MACD is still about as bullish as bullish gets.

I think I am going to lean on my old friend, the Andrews' pitchfork. Quick question: Am I the last well-known kid on Wall Street still using these models? I don't know why. They have always served me well and the algorithms seem to see these lines even when we don't.

Target Price: $103 (the new high on Wall Street)

Pivot: Upper trendline of pitchfork model (currently $86)

Add: Down to 50-day SMA (currently $56.90)

Panic: Loss of 200-day SMA (currently $42.30)

At the time of publication, Guilfoyle was long RKLB equity.