My Entry Strategy for Hershey After Earnings Turn Heads on Wall Street

Here's the technical setup and entry strategy for the consumer name that promises reliability for your portfolio.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Hershey (HSY) delivered a clear earnings surprise on February 5, 2026.

The company reported Q4 adjusted EPS of $1.71 (well above the consensus $1.40) and revenue of $3.09 billion (beating estimates of $2.98 billion to $3.00 billion). Even more encouraging was the 2026 guidance with adjusted EPS projected in the $8.20 to $8.52 range — significantly ahead of Wall Street’s prior models.

Wall Street Responds With Higher Hershey Price Targets

Analysts reacted quickly. Multiple firms raised price targets post-earnings, including JP Morgan (to $230 from $204, still "Neutral"), along with Goldman Sachs, Bank of America, UBS, Barclays, Bernstein, Evercore ISI, Wells Fargo, Stifel and others. The revisions were largely driven by the earnings beat and a more visible path to margin recovery in 2026.

My Position and Tactical Decision

Before the report, I had recommended starting a position in Hershey and adding on a positive outcome. The results met that bar, so I’m scaling in further now.

This isn’t about chasing momentum — it’s about positioning in a quality compounder at a still-reasonable entry point.

Short-Term Headwinds vs. Long-Term Strength

Most analysts maintained "Hold" ratings despite the higher targets, often citing near-term pressure from higher-cost inventory (tied to tariffs and cocoa) flowing through in Q1 2026. Only a handful — Goldman Sachs, Morgan Stanley and Piper Sandler — carry "Buy/Outperform" ratings.

That said, the longer-term fundamentals look solid, so it is plausible that Wall Street will change its mind. Hershey is demonstrating a credible path to margin expansion through disciplined hedging, pricing power and continued brand investment. Management expects gross margins to trend toward 41% in 2026 — meaningful progress after recent headwinds.

A Reliable Compounder, Not a Disruptor

Hershey isn’t a high-growth disruptor, and that’s the point. It’s a defensive, reliable name that, when bought at sensible valuations, can deliver better returns than cash or bonds over time while providing a cushion during market volatility.

In a well-diversified portfolio — especially one blending dividend growth with selective opportunities — it acts like a key ingredient: steady, dependable and capable of compounding quietly over the long haul.

Technical Setup and Entry Strategy

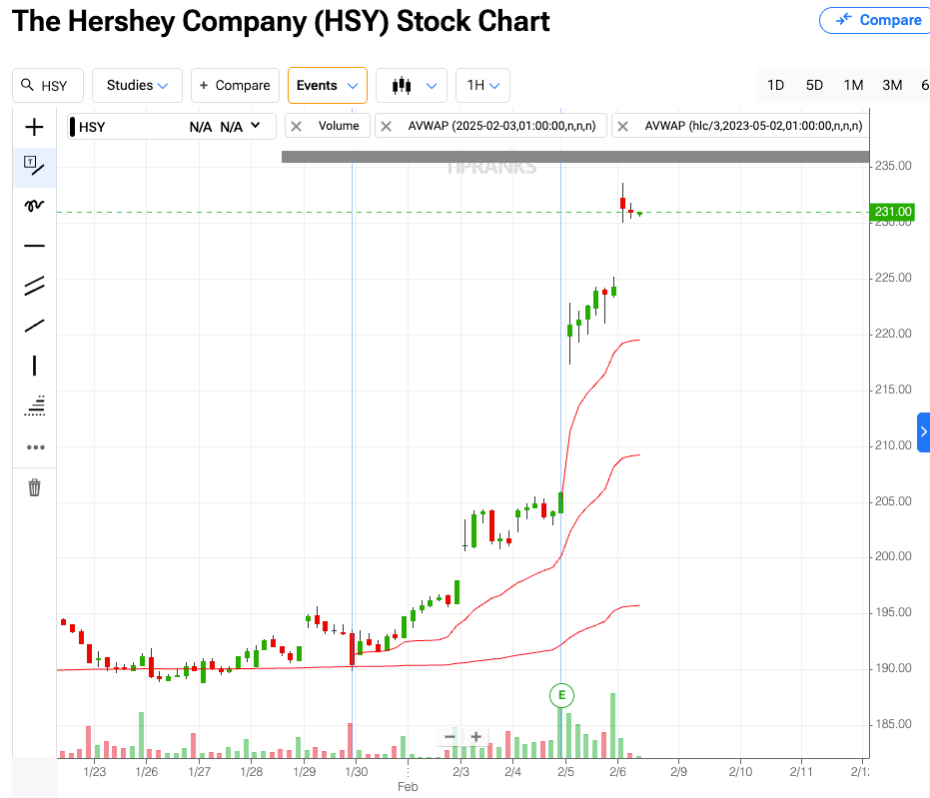

On the short-term chart, the stock gapped higher on strong volume following the earnings release, with some profit-taking near $225 before another leg up. Using an anchored volume-weighted average price (VWAP) from the earnings date — a technique I learned from my colleague thanks to Brian Shannon — shows meaningful support between $220 and $222. As of early February 6, the stock trades near $230 to $231.

For long-term investors, pullbacks are opportunities after this huge pop up in price. I’d look to accumulate on dips from current levels down to $220 to $222 (near the top of the post-earnings gap and anchored support). The longer-term trend has broken out more decisively than I initially anticipated, supported by both improved fundamentals and the wave of analyst revisions.

Conclusion: Patience Pays in Quality Names

While Q1 may bring some tariff- and inventory-related noise, the market appears willing to look past it as Hershey strengthens its brand and sets the stage for better profitability.

As long as the valuation doesn’t run too far ahead, Hershey still has room to deliver attractive long-term returns. It fits perfectly in portfolios prioritizing after-tax compounding and downside resilience.

What are your thoughts on Hershey right now.? Drop a comment below.