My Best Ideas for 2026 Will Sound Familiar ...

... But why fix something if it still works? Here's how I see closed-end municipal funds, Intel and more.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

While it might sound like a broken record, we are going to revisit two ideas from 2025, one of which was also from 2024.

From last year’s “best ideas” list:

I think you need to play this with individual stocks. I do think not only will we see money allocated to the Chip industry under Trump, it will have fewer strings attached. Since I cannot list individual stocks, I can recommend to look for who is building plants in the U.S., that is domestic, and whose stocks have underperformed. I do hold and will add more of a company that starts with I and ends with L. It has been a dog, but since I started buying late in the summer, it is ok (was briefly up). This fits my “contrarian” nature and my belief that this administration will do more for the domestic chip industry than their prior administration accomplished (though they tried, at least a little).

That company, Intel (INTC) , remains my largest single stock holding (for compliance reasons I tend to own mostly exchange-traded funds). I have been adding to this name again recently, and plan to add more for 2026.

While I like the sector as a whole (especially companies focused on domestic manufacturing), INTC continues to stand out for me. While I would like rules in place to regulate state investments, those are not really in place (and would likely be pushed to the limit by this admin, even if they were in place). I find it difficult to see a world where the government doesn’t try to support the taxpayers’ investment in this company. For full disclosure, INTC was my biggest single stock holding in 2025 and will be again in 2026. It was up 86% in 2025. Can it repeat that? Who knows, but while I think any stock in this space has potential, with those focused on manufacturing in the U.S. getting the most government support, the direct investment leads me to suspect that extra support will be given here.

Yes, even after a roughly 80% gain in 2025, I think there is more to come for this company.

For the Income Portfolio

It might seem lazy (and maybe it is), but for the third year in a row, I’m going to go with closed-end municipal funds as the largest/primary allocation in the income portion of the portfolio.

If Works, Why Fix 2024’s Best Idea?

As I said earlier, in 2024, I limited my scope to the income side of the portfolio and was adamant about owning closed-end muni funds. The closed-end muni funds I own (I do trade some, during the course of the year, based on net-asset value) had returns ranging from 3% to almost 10%, with the rough average somewhere between 5% and 6%. Better than buying iShares National Muni Bond ETF (MUB) , which didn’t quite make 1%. That's not as much as buying the high-yield corporate bond ETF (HYG) or the junk bond one (JNK) -- but it was much more efficient after taxes. Far better than treasury funds (many of which, like TLT had negative returns) and, certainly after tax, beat money market funds.

A few thoughts regarding this over allocation to closed-end muni funds:

We should continue to get rate cuts, which will keep the cost of leverage in the closed end fund space, lower. That helps returns.

I am not concerned about longer-term bond yields going much higher. There is a lot of angst out there about long-term bond yields. Yes, I could see 10’s going to 4.5% (currently 4.17%) as “bond vigilantes” get concerned about Fed independence. But, I think those concerns are overblown and underestimate the steps the admin, the Fed, and Treasury will take to control bond yields across the curve. I would not bet against 10’s getting below 4% which is Bessent’s stated objective.

We can trade closed end bond funds and enhance returns.

They move on overall yields. So you can add or shrink as you near term view on bonds changes. Currently I’m comfortable with yields so am not reducing positions here.

They move on relative attractiveness to taxable bond yields. There was a time this year where we were banging the table, even to corporate bond buyers, to buy muni’s because the after tax returns were extremely compelling. That “anomaly” has been resolved, so no longer overweight based on this metric.

The cost of the fund versus the NAV of the fund changes over time. There are opportunities to buy when the discount is very attractive or sell when it is relatively low. My “guideline” is over 10% discount is worth paying attention to and less than 5% discount is also worth paying attention to.

Sometimes the entire sector moves in tandem, but the best opportunities come when for some reason one set of funds is trading very rich relative to NAV while another set is trading very cheaply. You can rotate without changing your exposure much.

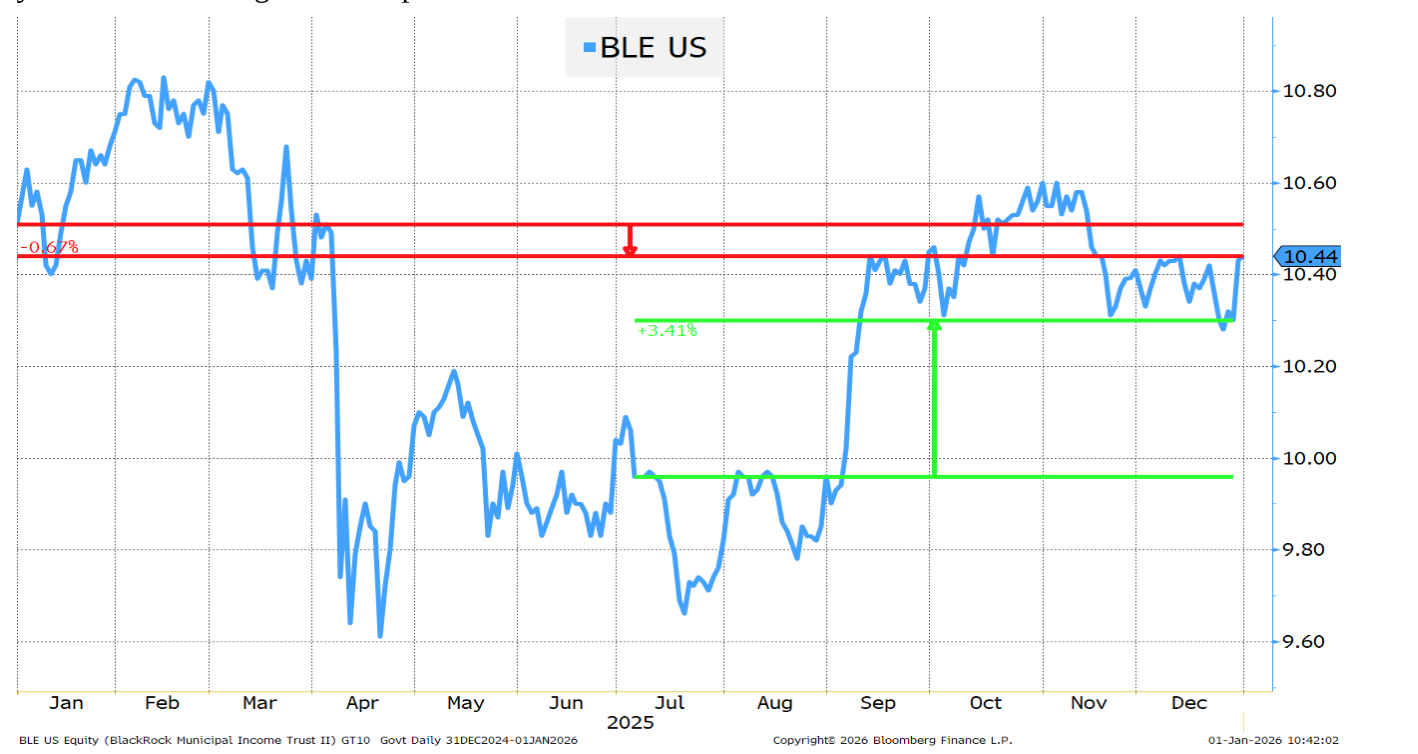

We will take a closer look at Blackrock Municipal Income Trust II. This year, according to Bloomberg) it paid 6.21% federal tax free. I like it for that reason.

It did decline 0.6% in price over the course of the year. On the other hand, if you were able to buy more this summer, when munis were trading particularly cheap and 10 year bond yields were higher, you could be sitting on a nice profit on that addition.

I did not see as many opportunities in NAV this year, as we see sometimes, but will continue to be vigilant for those as a way to enhance returns here.

Keep those closed-end muni funds heavily overweight in the income portion of your portfolio.