Jacking Up the Price Target for This Small-Cap Offshore Drilling Play

Here's my plan for this 'Stocks Under $10' offshore shallow-water drilling contractor as it reports.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Early on Thursday morning, "Stocks Under $10" name and Sarge-folio holding Borr Drilling (BORR) delivered a beat in its fourth-quarter financial results. For the period ended Dec. 31, Borr Drilling posted unadjusted "earnings" per share of $0.00 on revenue of $259.4 million. That top line print managed to beat Wall Street, despite reflecting a year-over-year contraction of 1.4%. The bottom-line number also beat the Street, by three cents per share.

Operating expenses increased 18.7% to $192.1 million. That left an operating income of $67.4 million as operating margin dropped from 38.4% to 26%. After accounting for interest, other income & expenses as well as taxes, net income / loss attributable to shareholders decreased from $26.3 million to a $1 million loss. This works out to fully diluted earnings per share of $0.00, down from the year ago comparison of $0.10.

The CEO

CEO Bruno Morand said Borr's fleet contract "visibility" continues to improve as the company reduces remaining open days.

"Recent awards and extensions increased 2026 coverage to 80% in the first half and 48% in the second half, such numbers adjusted for the recently acquired rigs. Since our last quarterly report, we secured new commitments for seven rigs and expect further coverage gains in the coming months as we progress negotiations on multiple active leads."

Morand added in his statement that, "We believe the jack-up market bottom is now behind us. We see fundamentals recovering gradually as demand increases, most notably in the Middle East where multiple tenders are progressing for long-term contracts for an estimated 13 rigs. Recent industry data shows the global jack-up rig tendering pipeline is at multi-year highs, reflecting stronger customer activity and longer-dated contracting opportunities."

The Balance Sheet

Borr ended the period with a cash position of $380.7 million and current assets of $768.4 million. Current liabilities add up to $350.7 million including $129.3 million in short-term debt that will at least partially have to be refinanced. That puts the firm's current ratio at a healthy 2.19.

Total assets amount to $2.857 billion, which is mostly in jack-up rigs. Total liabilities less equity comes to $2.403 billion. This does include long-term debt of $2.021 billion, which to be honest, is more than daunting.

Opinion

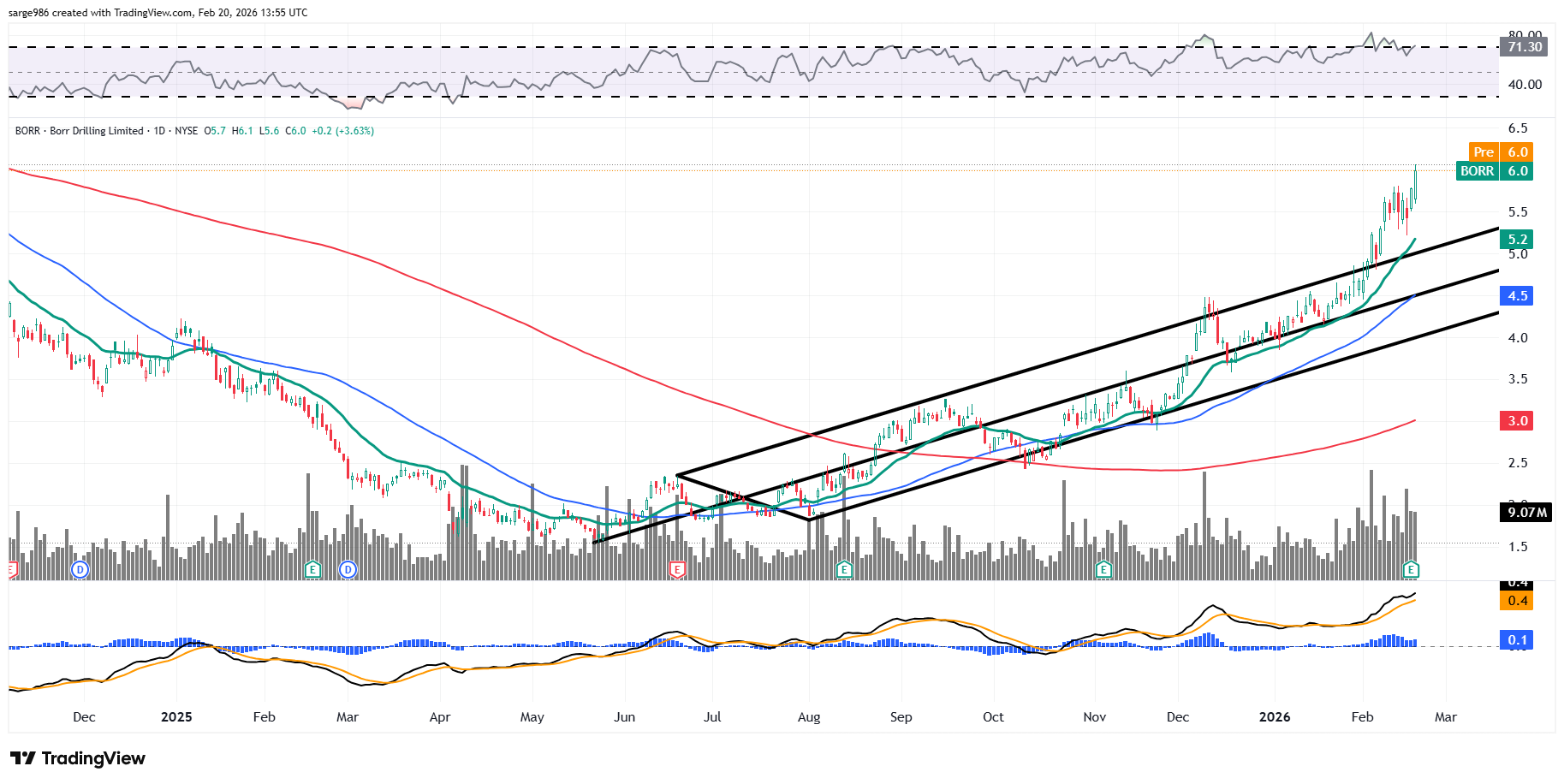

I put the "Stocks Under $10" crowd into this name back in late December with the stock trading around $4. My average point of entry is actually $3.99. Initially, I had placed a $5 target price on the stock. In late January, I revised that target price up to $5.50. In the past week and change, that target had been breached and on Thursday evening, the shares closed at $5.99. The last sale that I saw this morning is an even $6, so if one is still in the name and has not yet taken any profits, one is up 49.3%. not bad for less than two months' work. What now?

Readers will see that BORR has broken out from the Andres' Pitchfork model that I had shown you in the past. The shares are now trading well above all of their key moving averages. I would suggest taking a profit on something at this point if one has not already done so. A failure to do so is to tempt fate.

This is a Top 10 position for me in terms of weighting. Actually, BORR is No. 10. Hence, I will be taking a substantial amount off as I have losses elsewhere in my portfolio, so I need to lock a little something in here. Additionally, I don't trust the recent semi-parabolic move. Both relative strength and the daily moving average convergence divergence look a bit extended. With the balance, I will be taking my target price a little higher.

Borr Drilling Target

Target Price: $6.50 (up from $5.50)

Pivot: upper trendline (currently $5.00)

Add: Down to 50-day SMA (currently $4.50)

Panic: Loss of lower trendline

At the time of publication, Guilfoyle was long BORR equity.