An Income Generating Strategy for Gold Buyers

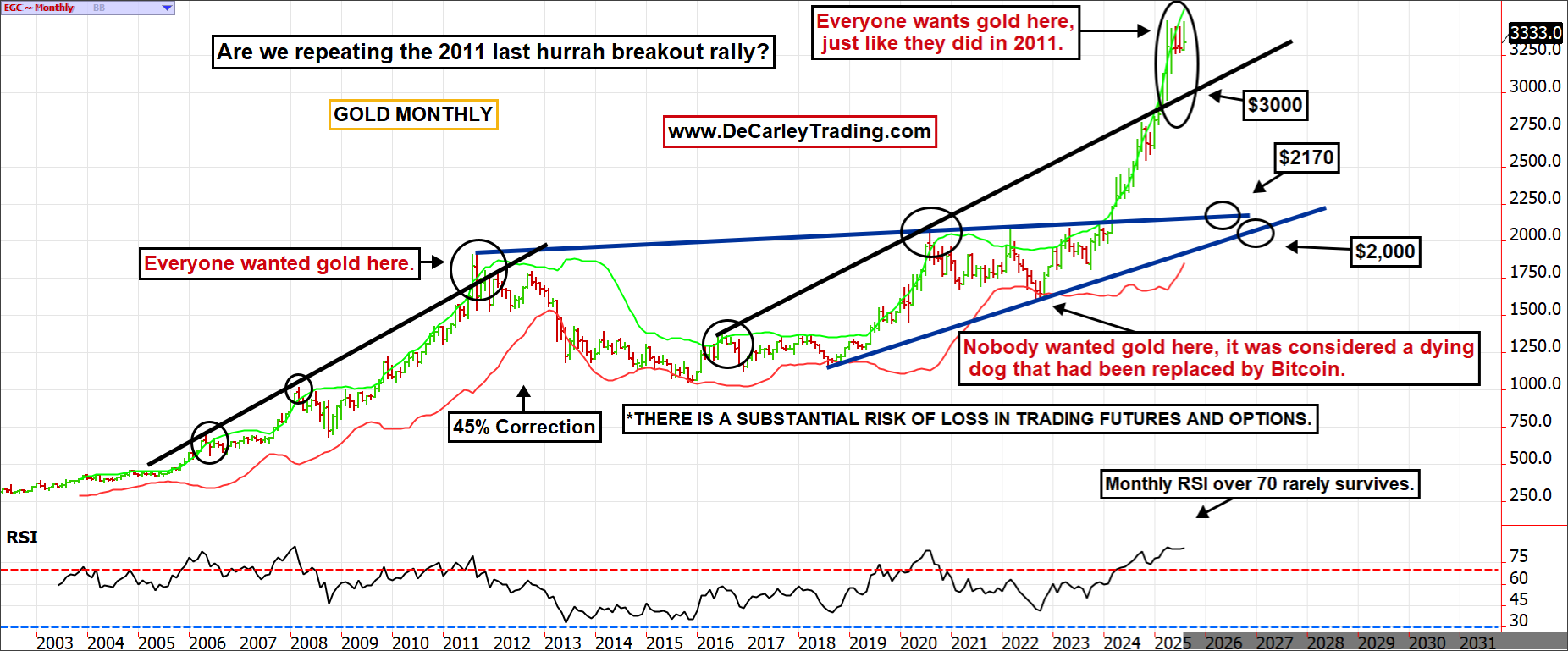

We’ve been vocal about our opinion that the gold market is repeating the 2011 blow-off top pattern.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

We’ve been vocal about our opinion that the gold market is repeating the 2011 blow-off top pattern.

This particular cycle has been bigger and better than the last because of pandemic liquidity sloshing around in the system, but that doesn’t mean the conclusion will be different. Markets often repeat themselves, or at least rhyme.

If you are looking for bearish analyst calls or news, you won’t find it. But don’t let this detract you from being skeptical. It was only three years ago that gold was trading near $1,600, and the consensus opinion was that it was a dead dog acting as a drag to portfolios. Fast forward to today, and it is considered a must-hold in those same portfolios. Just as conventional thinking was misguided then, it might be wrong today.

I’ve always said, and believed, that gold is an asset that should only be bought when nobody wants it. If everyone is buying it, it’s probably too late for anyone with a time horizon of less than a decade or longer. If there has ever been a sign that the bull market in gold has become an overcrowded trade and opinion, it is the fact that Costco has gotten into the business of selling gold bars.

In my view, this premise is even more compelling in today’s environment of relatively high interest rates. This is because those looking to put money into what they deem to be a safe haven asset are likely going to choose between U.S. Treasuries and gold. Of course, there are other choices, but the majority of such funds will flow into these two options. Safe haven dollars can purchase gold, an asset that doesn’t produce income, at an all-time high without a risk parachute, or they can buy Treasuries at multi-decade lows with a yield of 4% to 5% to cushion downside price risk. Ironically, the masses are selecting the former and passing on the latter.

However, for those who insist on gold over Treasuries to avoid the risk of a U.S. Treasury default or a U.S. dollar failure, there are a few ways to produce some income from a long gold holding.

Those holding gold bullion at home or in a safe might consider selling call options against the asset. This is far from perfect, but in an environment in which the downside risk is palpable, it is worth contemplation.

The drawback to this idea is that the short call component of the strategy must be held in a futures trading account and margined separately (as if the underlying asset didn’t exist). In short, some view this as an inefficient use of capital. Nevertheless, it allows one to produce an income stream via an asset that doesn’t have one.

Selling a call against gold bullion might look like this: If you own 100 ounces of gold coins or bars valued at roughly $350,000 with the price of gold at $3,500, you could sell a December gold $3,600 call option for about $6,700. At the time of this write-up, this option had 109 days to expiration. The sale of the call generates approximately 2% of the asset's income ($350,000 worth of gold); if annualized, a trader could produce roughly 6% of income by repeating the process throughout the year.

Of course, there is a catch, which is that the upside profit potential is capped above the strike price of the short call option. Specifically, for the next 109 days, the underlying gold asset can appreciate above $3,600 per ounce, but if it does, the losses on the short call option offset the asset gains. Even so, this would equate to a gain of about 2.8% in that time frame. Under most circumstances, this is an acceptable trade-off. It should be noted, however, that although gold is known as a safe-haven asset, it has a history of stunning corrections. For instance, the 2011 top was met with a 45% haircut that took nearly a decade to recover. Thus, the collection of roughly 6% in income against the asset compensates for some of the downside risk, it certainly doesn’t make a dent in the potential repeat of 2011.

Alternatively, one could consider holding gold in the futures market in an attempt to take advantage of the free leverage provided by the CME Group’s COMEX Exchange.

In this strategy, an investor wishing to allocate $350,000 toward gold could purchase a single futures contract at $3,500 per ounce, or whatever the current price. The standard gold futures contract represents 100 ounces, so if gold is at $3,300 and the goal is to buy $350,000 worth, a few micro-sized at 10 ounces would make up the difference. Similarly, if gold is at $3,700, one could buy about nine micros (or one half-sized mini and a handful of micros); you get the idea. To further illustrate, if you wanted just $35,000 worth of gold, you could purchase a single micro futures contract (10 ounces) at $3,500.

To purchase the desired futures contracts, it is necessary to have the appropriate margin deposited into a futures trading account. The exchange required margin occasionally fluctuates with price and volatility, and many commodity brokerages (not ours, DeCarley Trading) charge more than the exchange requires (this is called a margin up-charge).

However, assuming the margin to enter a long 100-ounce futures contract is $16,500, which was the case as I was writing this piece, a trader could theoretically buy a 100-ounce gold future in an account of that size and then deposit the remaining $333,500 in an interest-bearing account such as a money market fund, a high-yield savings account, or T-Bills. This allows someone with bullish gold exposure of $350,000 to earn an annual income of 4% to 5%, depending on current rates and holdings.

However, I’ve simplified this example. In real life, you would want to keep more than the required margin in a futures account to absorb the ebbs and flows of gold prices; ideally, one would want at least $25,000. Furthermore, even with some room for a margin cushion, margin calls might periodically require that funds be sent to the futures account to cover gold price losses. Thus, the purchase of T-Bills, which expire every three months or monthly, might be a futile exercise if the investor must break the bills to raise cash to meet margin calls. Nevertheless, if the lack of income is the only thing holding you back from buying gold in substantial quantities, there are some messy but viable workarounds.

As you have probably concluded, this strategy can be used for other holdings as well.

For instance, if you would like to acquire $32,500 worth of S&P 500 stock exposure, you can purchase a micro E-mini S&P futures contract in a relatively small futures account (the margin is $2,450) and invest just under $30,000 in a money market fund to collect interest. On a bigger scale, you could use the original E-mini S&P 500 future sized at $50 per point or about $325,000 worth of similarly allocated stock with the S&P 500 at 6,500. This gets the best of both worlds.

Yet, such aggressive and sophisticated strategies come with the inconvenience of potential margin calls and the temptation to overleverage. In short, even a disciplined investor might be tempted to buy two micro futures to be backed by $30,000 in funds earning interest elsewhere. As harmless as this might seem, it can backfire quickly if losses are sudden, such as what was experienced in March 2020 at the beginning of the pandemic.

Imagine not being able to free up cash and wire it to your futures account before being blown out of your futures, only to watch the market immediately recover without you. This is a real risk of this type of strategy.

In other words, a hands-off strategy of owning a stock index might turn into a hectic game of margin call musical chairs if you opt for the more complicated, yet higher income-producing, strategy of earning interest on cash while being exposed to the capital gain potential of equities.