How to Hedge Gold as U.S. Dollar Hits Bottom

Here's a trade that could short gold with a potential substantial amount of money in return.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Not everyone should speculate using options on futures, but everyone should be open to learning about the opportunities available, should they ever find themselves with a high conviction opinion they would like to express in the market with risk capital. Further, the futures and options markets were created for hedging purposes and are amazingly efficient at doing just that. The strategy outlined in this piece can be used to hedge at least some of the downside risk in gold.

The gold market is still working off the froth that was built into both the futures market and the option market. Because of relatively high volatility combined with political and economic uncertainty, the option market is offering traders an opportunity to finance bearish plays in exchange for accepting unlimited risk at much higher prices (meaning there is a lot of room for error and attractive profit potential).

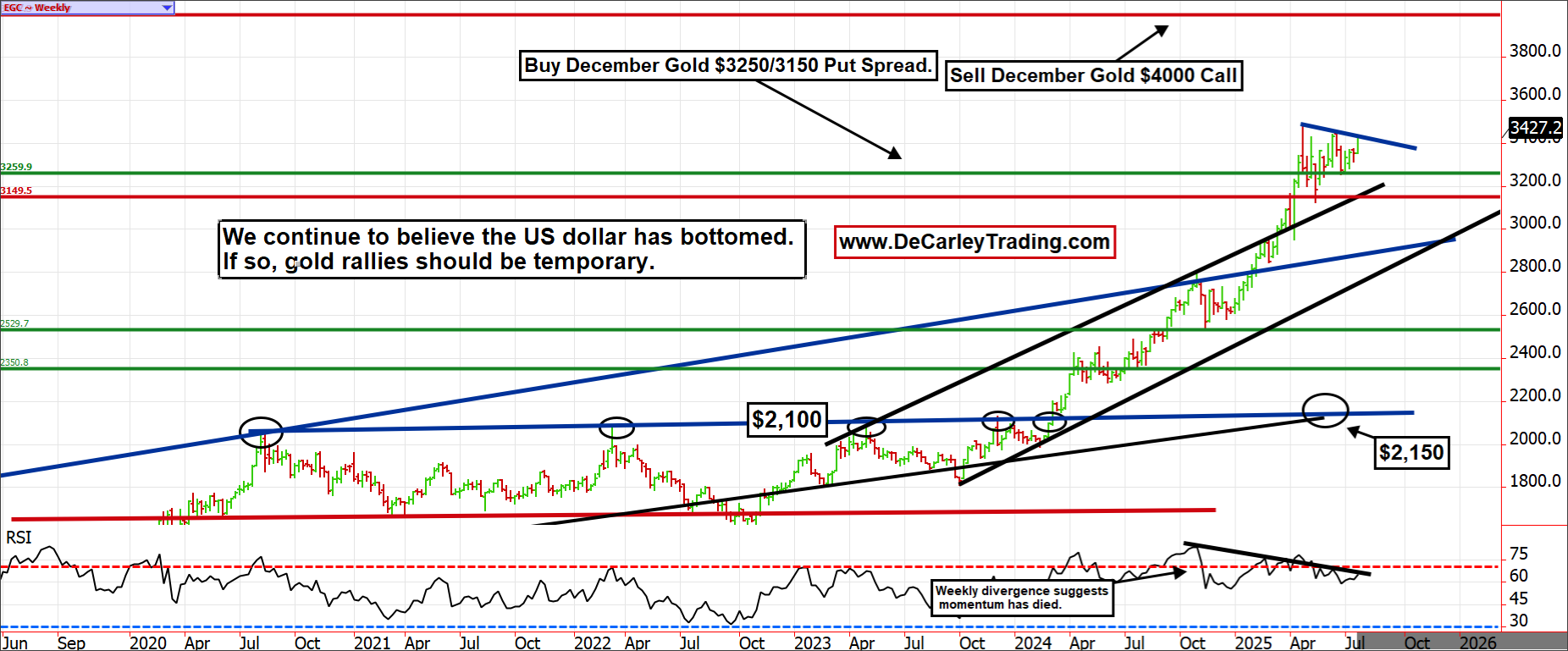

We believe the U.S. dollar has bottomed; if this is the case, gold has no business being above $3,000, but it might take the market some time to figure it out. Furthermore, when examining seasonality in gold, the data indicate a substantial shift; however, over the last five years, there has been a strong tendency for the metal to decline in late July. Lastly, the downtrend line that started at the all-time high posted earlier this year remains in effect.

If we break it, there is sharp resistance at $3,500 (the all-time-high). With these two buffers in place, we feel comfortable re-entering with a long put spread, paid for with a short call option; see the details below. As an aside, we designed the spread to allow for easy, common-sense adjustments if the market continues to rally; in that scenario, we should be able to buy back the short put leg and hold the other two legs in anticipation of the desired downward move.

The Trade

DECEMBER GOLD BEAR PUT SPREADS WITH A NAKED CALL

SELL DECEMBER GOLD 4000 CALL

BUY DECEMBER GOLD 3250 PUT

SELL DECEMBER GOLD 3150 PUT

Cost = Credit, not cost, of about $500 to $600 in exchange for unlimited risk

Margin = $5,846

Risk = Theoretically unlimited above 4000

Maximum Profit = Roughly $10,500 prior to considering transaction costs, but this is only possible if held to expiration and is unlikely. We would be elated with a profit between $2,000 and $3,000

Expiration = November 24

DTE = 125

What Does This Mean in English?

It isn't feasible to provide a complete option trading course in a short online column, but the premise of this type of strategy is to use the market's money to finance our speculations. In other words, we would like to be long a gold put, but buying the $3,250 put outright would incur a cost and risk exceeding $4,000. Even in 2025 dollars, this is a substantial amount of money.

Further, options are eroding assets that, more often than not, expire worthless. Thus, buying the put outright is playing against the odds of success. For that position to be profitable, gold would have to fall below the strike price of $3,250 enough to recoup the $4,000 spent ($3,210) and it would have to do so within the allocated timeframe (approximately 124 days).

We can cut the cost and risk of buying the $3,250 put in half by selling the $3,150 put. However, this also caps the profit potential to the spread between the two option strikes ($3,250 to $3,150) minus the premium paid of about $20, leaving the maximum potential at about $80.00 or $8,000. This probably looks good on paper to most because the risk is limited to $2,000 and the payout might be as high as $8,000, but again, this is a relatively low probability event unless your timing and analysis is precise.

We can further reduce the cost of acquiring the $3,250/$3,150 vertical put spread by selling the $4,000 call. We executed this combination on Tuesday, resulting in a credit of $500 to $700. This means we were collecting several hundred dollars more for the short $4,000 call than was required to pay for the put spread. In short, it wasn't just a free trade; the market paid us to participate. Keep in mind that these figures are rounded and exclude transaction costs; however, for educational purposes, you should get the basic idea.

Lastly, "free" is a loaded term in all aspects of life, especially in option trading. This trade doesn't require a cash outlay because we are collecting more than enough on the short options to cover the cost of our long put. However, there is a margin requirement of just under $11,000, meaning you would need at least this amount in a trading account to execute the play. I would suggest allocating $20,000 to $30,000 to this type of play for good measure. Lastly, selling the $4,000 call option exposes the trade to unlimited risk above $4,000. An easy way to think about this is that if the market goes above $4,000, it is like being short a futures contract at that price. The current value of gold is about $500 lower, so while there is substantial risk above, it is relatively distant from the current market.

As an aside, if gold moves higher, there are ways to hedge risk in an attempt to avoid catastrophe, such as buying micro futures to lower the position delta (how much the position moves relative to moves in the underlying futures market)

Again, this isn't a recommendation and shouldn't be casually traded; if you aren't familiar with commodity options and the risks that come with them, keep it to a paper trade.