How Lyft Could Get a Lift as Takeover Target

Lyft fights for survival vs. Uber as Jensen Huang’s ‘ChatGPT Moment’ arrives.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Lyft

Lyft

Uber Technologies (UBER) recently announced it was expanding into the autonomous driving space. Nvidia (NVDA) and Uber are teaming up to launch a robotaxi fleet that’s expected to hit the streets next year. By 2028, the vehicles are expected to roll out in 28 cities.

Nvidia CEO Jensen Huang recently stated that, “The ChatGPT moment for self-driving cars has arrived.” If that’s the case, how prepared is Uber competitor Lyft (LYFT) for that moment?

Lyft is partnered with privately held May Mobility on its autonomous vehicle program, which currently operates in Atlanta and Nashville. The service is expected to expand to Dallas sometime this year.

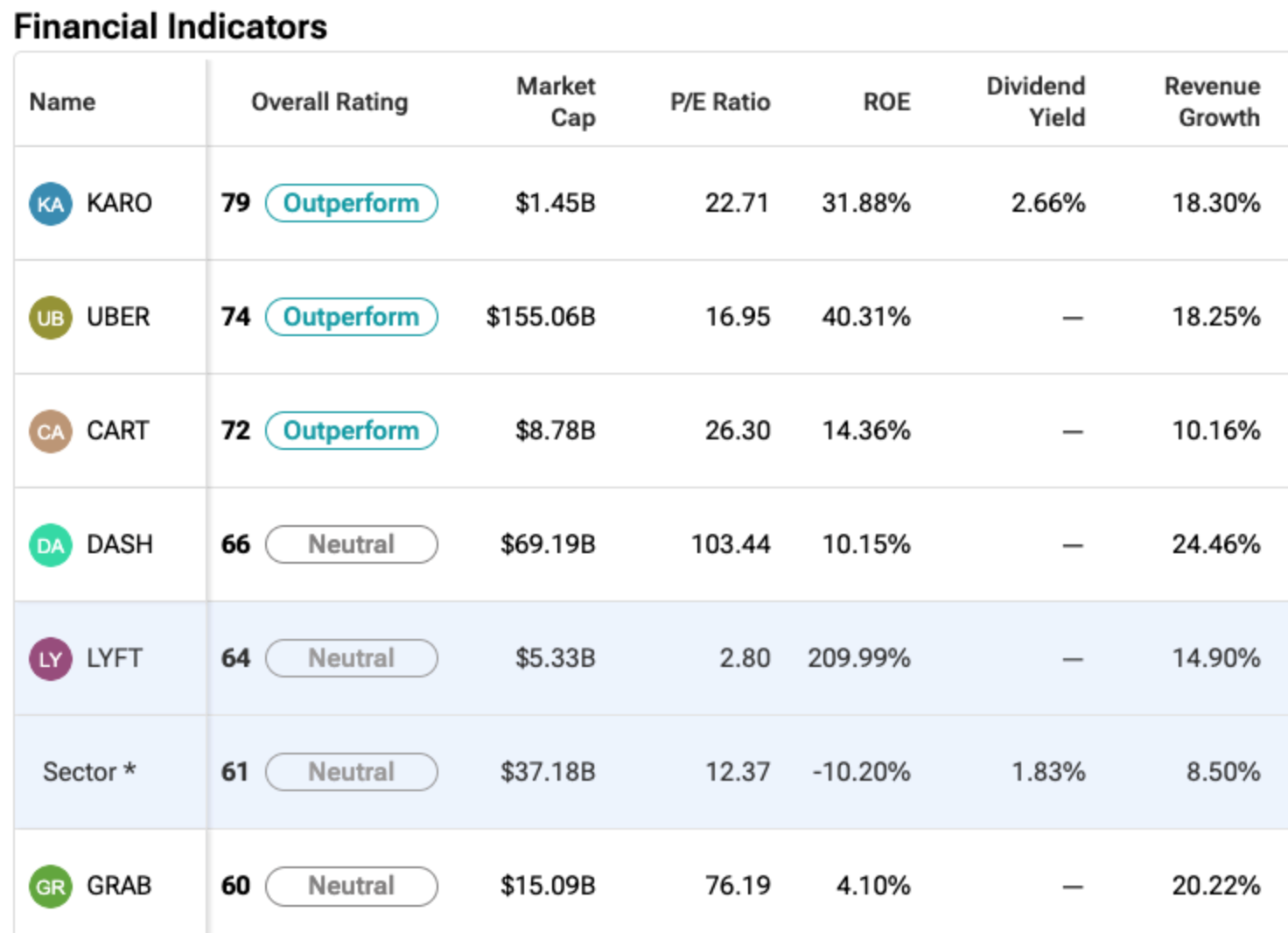

Head-to-Head Comparison

Uber has a market capitalization of $152 billion, while Lyft’s market cap is just $5.3 billion. This is a huge disparity when you consider that Lyft owns over one-fourth of the U.S. ride share market.

When it comes to valuation, Lyft is a much cheaper stock. Lyft trades at a multiple of just under three-times earnings, on a trailing 12-month basis. By that same measurement, Uber is valued at just under 17-times earnings.

Based on this metric, if Lyft traded at a similar valuation to Uber, the stock would trade near $75 per share.

Where the Rubber Meets the Road

Performance-wise, neither stock is off to a great start in 2026. Year-to-date, Uber (left chart, below) is down by 8.75%. Meanwhile, the broader market, represented by the S&P 500, which has lost just 3.6% so far this year.

However, Lyft (right chart, below) has lost nearly one-third of its value since January 1, falling 32.5% in 2026.

Why has Lyft lost so much ground, so quickly?

Here’s Where Lyft Stalls Out

Inexpensive stocks are usually inexpensive for a reason, and Lyft is no exception.

Why is Lyft cheap? In February, the San Francisco-based company reported that quarterly revenue came in at $1.59 billion for the quarter, well short of analysts’ estimates of $1.75 billion.

This marked the fifth consecutive quarter that Lyft’s revenues were lower than predicted. Also, that $1.59 billion figure marked a decline from the previous quarter’s result of $1.69 billion.

Meanwhile, Uber’s revenues continue to climb to new heights. Uber took in $14.37 billion in its most recent quarter, a new record high.

Related: 8 Key Items Shaping the Stock Market Tuesday: 'Follow Through', PMI, Broadcom, Oracle

Lyft’s Customer Base is Key

With competition set to arrive from every direction, and the stock clearly out of favor, what value does Lyft possess that doesn’t appear on its chart or in its financial statements?

The answer is Lyft’s customer base.

Lyft has a base of nearly 25 million riders. While this pales in comparison with Uber’s worldwide base of about 200 million, a significant number of consumers are already using the Lyft app.

Is Lyft a Takeover Target?

That fact, combined with its inexpensive valuation, could make Lyft an intriguing takeover target.

A company that acquires Lyft would become the second-largest U.S. ride share provider overnight. The right acquirer could leverage the recognizable Lyft name into a popular international brand, following in Uber’s tracks.

On the negative side, other than its user base, Lyft has little leverage in an acquisition negotiation. If revenues continue to stall, the stock could continue to slide.

Bottom Line

Lyft is a slow-growing company in a fast-growing space, and that’s why the stock is inexpensive right now. It's an intriguing takeover candidate, thanks to its large user base and inexpensive valuation, making it an intriguing under-the-radar pick.

At the time of publication, Ponsi was long UBER and LYFT.