Here’s a High-Quality, Low-Risk Play for Smart Investors

After years of solid growth across all major metrics not reflected at all in the current share price, this Dividend Aristocrat is poised for a great catch-up move.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Sometimes the market delivers terrific values whose low valuations defy all logic. Today’s selection, Sonoco Products SON, is a recent example of that.

Sonoco is a world leader in packaging products. Do not confuse Sonoco with Sunoco, the oil and gas company.

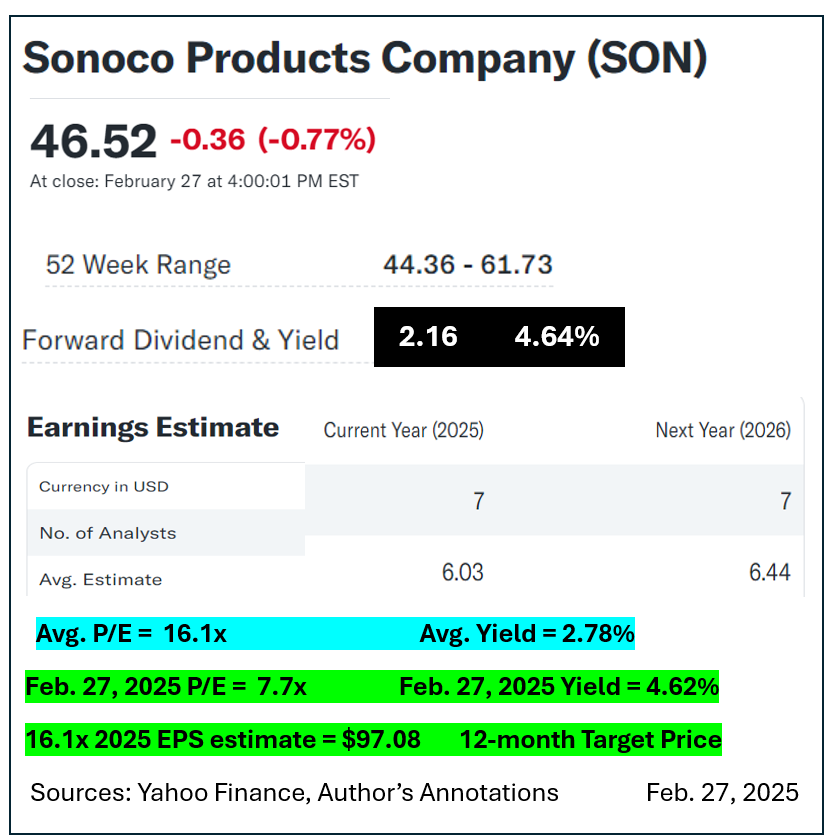

2025 figures to be a record year for Sonoco. Yahoo Finance sees EPS climbing to $6.03 [up 23.3%] versus $4.89 in adjusted earnings during 2024.

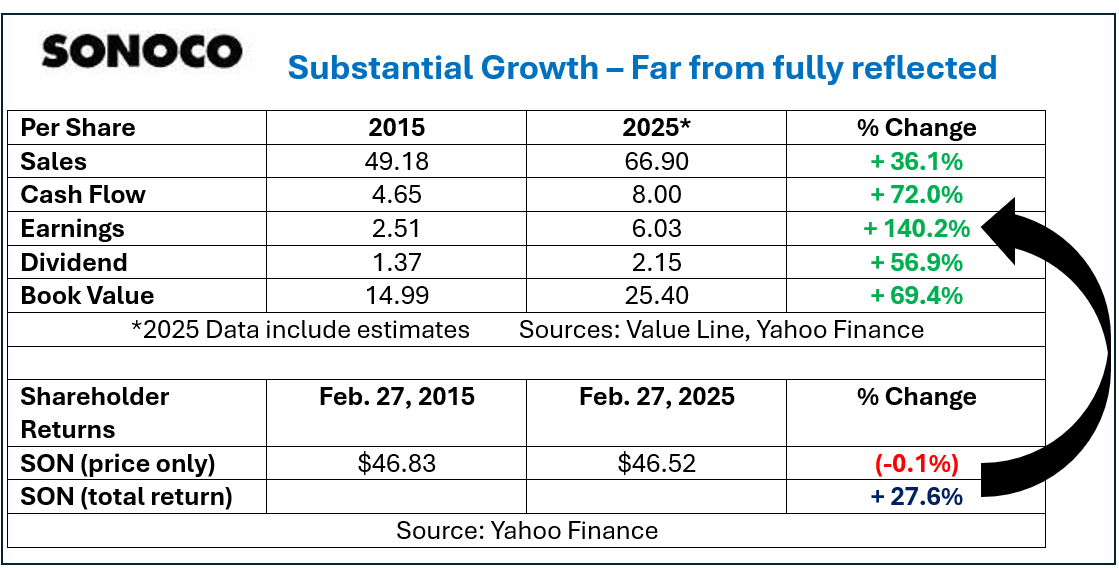

The growth table below details expected cumulative results over the most recent decade.

Ten years of solid growth across all major metrics was not reflected at all in the share price. Total return of 27.6% lagged a greater than 140% increase in EPS over that period.

The lack of progress in the share price was bad news for continuous stockholders. It represents great news for investors looking to buy in now, though.

Sonoco is a Dividend Aristocrat, defined as companies which have raised annual dividends for at least twenty-five straight years. 2025 figures to be Sonoco’s 42nd year of higher cash payouts.

At its Feb. 27, 2025 closing quote of $46.52 the forward yield is projected at a generous 4.62%. Sonoco directors typically raise the quarterly rate in the second quarter — 54-cents per share, up from 52-cents currently, appears a good bet. That would be a 3.85% bump.

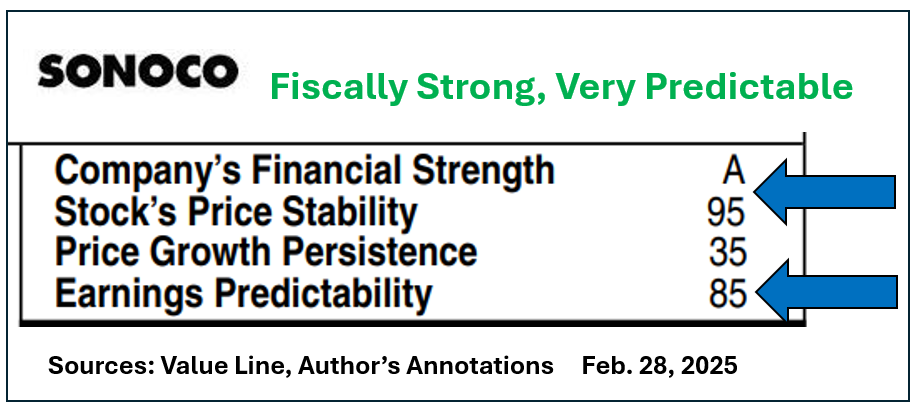

Sonoco earned fine grades for financial strength, stock price stability and earnings predictability from Value Line. Its currently low “stock price growth persistence” is a positive if you are accumulating shares at today’s low absolute price and stunningly cheap valuation.

Value Line calls SON’s 10-year median P/E as 17.0x. I calculated a 16.1x average P/E over the past decade or so.

A simple regression to the mean valuation based on year-ahead profitability suggests a 12-month target price of $97 or better appears within reach. That goal is far from an upper limit.

SON fetched as high as $66.60 per share back in 2019 when EPS came in at $3.53. That was a multiple of 18.9x. It topped out at $69.80, or 19.7x earnings, during 2021 with EPS on track to be $3.55, not the $6.03 projected for 2025.

Do not simply trust me on how cheap Sonoco Products looks right now.

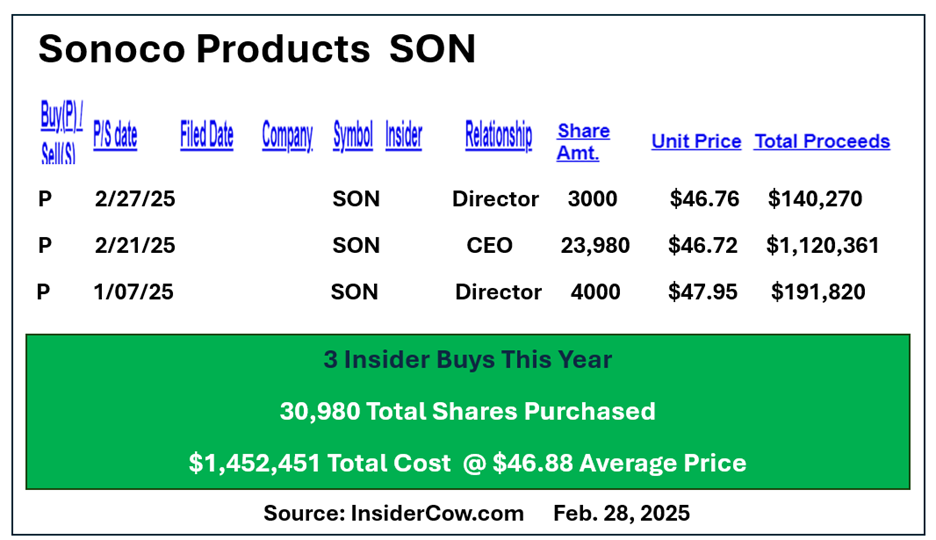

Since this year began there were two substantial dollar director buys, one each in January and February. The company’s CEO, who already owned about $24 million worth of SON shares, saw fit to add another $1.12 million in additional shares on Feb. 21, 2025 at an average cost of $46.72.

The people who know the company best think it is a great buy, seconding my own opinion.

At Thursday afternoon’s closing quote, we could now buy SON a tad cheaper than the company officers did.

SON is the opposite of a “momentum” stock. Its chart appears unappealing, so short-term traders have shunned the shares. With a forward P/E of just 7.7x Sonoco is now offered at a substantial discount to its average multiple while paying a well above average 4.62% forward yield.

Reverse engineering the current $2.08 annual rate to a more typical 2.79% generates a $74.55 per share present-day fair value for SON. Simply reaching that level would deliver a 60.25% gain from here plus any dividend income collected while waiting for the move to unfold.

Sonoco Products is poised for a great catch-up move and seems to have decidedly minimal downside risk. Insiders have been buying. What else do you need to know?

More Paul Price:

- Beware, or Profit From, Extreme Stock Market Deviations

- This Is the Single Most Important Factor in How Wealthy You’ll Be at Retirement

- What Traits Make a Great Stock Investor?

At the time of publication, Price was long SON shares, short SON naked puts. SON is one of his largest personal dollar holdings.