Google 'Turns the Tables' to Become the New King of AI

Here's how they did it. Plus, here is my top small-cap play on edge computing.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

AI isn't in a bubble, and it isn't dead. What is happening in the sector is that investors are sorting out the leaders from the laggards.

Nvidia's (NVDA) earnings report made it clear that companies that provide infrastructure and services have very different fundamentals than the hyperscalers that use their services. There is also the software AI group that is just getting started with rolling out products that use AI.

In the past week, there has been a major reshuffling in hyperscaler leadership. For quite a while, Alphabet (GOOGL) struggled versus other Magnificent Seven (MAGS) names due to concerns that AI would destroy their legacy search business. Who needs search when you have AI?

However, Google turned the tables. Its AI service, Gemini 3, is being hailed as a giant leap forward. Marc Benioff, CEO of Salesforce (CRM) , posted this weekend: "I've used ChatGPT every day for 3 years. Just spent 2 hours on Gemini 3. I'm not going back. The leap is insane — reasoning, speed, images, video… everything is sharper and faster. It feels like the world just changed, again."

In addition to this leap in technology, what may be even more impactful is that Google developed it using its own Tensor Processing Units (TPUs), to gain a significant advantage in the AI race. According to Google, its strategy is "to control the entire technology stack — from its world-class research and models (like Gemini) to its custom hardware and cloud infrastructure. By using its own TPUs, Google reduces its dependency on external suppliers like Nvidia (NVDA) , which can translate into faster scaling, higher efficiency, and lower operational costs."

This has made Google the new king of AI. I'm long and looking to add to my position.

Gaining an 'Edge'

Another AI-related play I'm looking at is at the other end of the size spectrum. Duos Technologies (DUOT). Duos is a small company with a market capitalization of just $180 million, but it has a strategic position in the growing edge data center market.

Edge computing brings data processing, analysis, and storage closer to the physical location where the data is generated, rather than relying on a centralized cloud or a distant data center. This means lower latency, which is necessary for applications such as self-driving cars and robotics that need instant feedback to operate correctly.

Duos is deploying its edge data centers in underserved markets such as schools, hospitals, and businesses that previously had to rely on distant, slow infrastructure. Duos's edge data centers are small, modular units designed for markets that lack robust digital infrastructure. They provide localized, Tier 3-level data center capacity at a lower cost (around $1.2 million to $1.4 million fully installed). This makes services like AI and high-speed connectivity accessible in new markets very quickly.

Duos is forecasting the deployment of 15 edge systems by the end of 2025, and has plans for an additional 45-50 sites in 2026. In addition to the initial cost, there is ongoing operating income each month. The company has been awarded a U.S. patent for a modular data center entryway design and signed a strategic partnership with FiberLight to expand connectivity.

In addition to the core edge computing business, Duos is generating substantial revenue from its Asset Management Division, which provides specialized operating staff, design, engineering, and support services for the deployment and operation of mobile gas turbines. This helps provide power in remote areas.

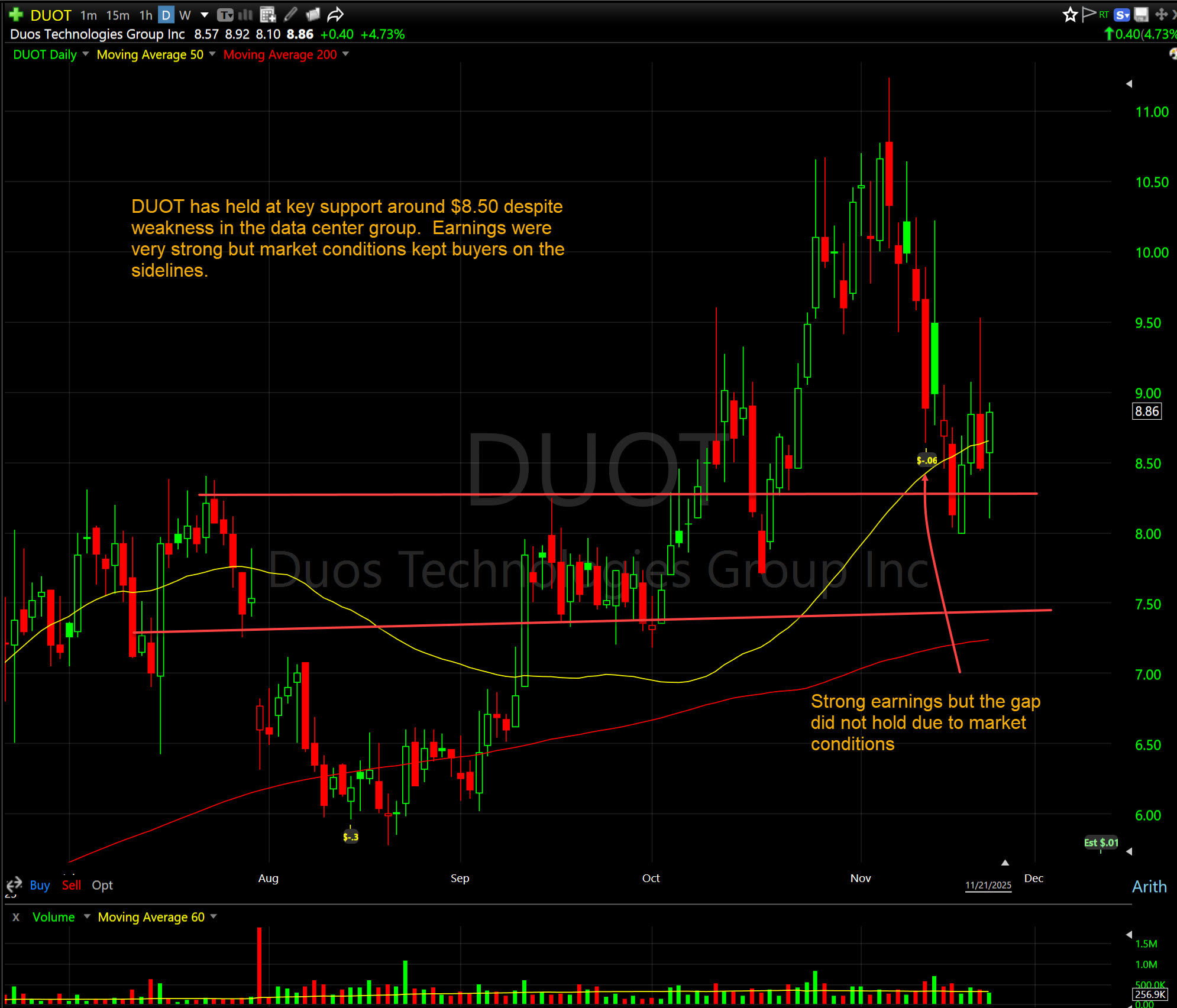

The company substantially beat expectations in the third quarter and is looking to turn profitable in 2026. There is no major analyst coverage.

Technically, the stock is sitting near support and has held up well during the recent market pressure on the data center group. As always, I am looking to trade the stock aggressively as it develops.

At the time of publication, Rev Shark was long GOOGL, NVDA and DUOS.

Please note that due to factors including low market capitalization and/or insufficient public float, we consider DUOT to be a small-cap stock. You should be aware that such stocks are subject to more risk than stocks of larger companies, including greater volatility, lower liquidity and less publicly available information, and that postings such as this one can have an effect on their stock prices.