For This $10 Micro-Cap Stock, the Pivot Point Is Key

Let's look under the hood at a speculative automotive technology company and strategize how to play it.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

A micro-cap stock with no sales?

Why should we even care?

The name has been trending higher but is well off of its December highs. The company is not expected to drive any revenue for the current quarter and drove revenue of a whopping $11K (yes, that's a K) for the quarter ended this past September.

Obviously, this is a speculative play if it is a play at all, so let's dig in. Oh, I should also mention that this article is in response to a subscriber request. This is something we do from time to time here at TheStreet Pro under the "Stocks Under $10" and "Small-Caps" banners.

Just as a reminder, and these rules are not actually rules, they are guidelines. Large-caps are valued at more than $10 billion, mid-caps are valued at between $2 billion and $10 billion, and small-caps are companies currently valued by the market at anywhere between $300 million and $2 billion.

Then we get to really small companies. Micro-caps are valued between $50 million and $250 million, while nano-caps are valued at less than $50 million.

The stock we are going to look at today is REE Automotive Ltd. REE. Ree Automotive is an Israel-headquartered technology company specializing in the field of automotive tech and the production of platforms for electric vehicles. The company uses both x-by-wire technology to control full drive-by-wire, brake-by-wire, and steer-by-wire.

(Lack of) Earnings

For the third quarter ended September 30, REE generated revenue of $11,000, while the cost of revenue printed at $354,000, leaving a gross loss of $343,000, narrowing from a loss of $1.204 million. Total operating expenses decreased 25.4% to $18.178 million. That left an operating loss of $18.521 million. After accounting for losses from warrants being remeasured and other non-operating expenses as well as taxes, the firm's net loss printed at $38.5 thousand. This put its GAAP loss per share at $2.56, versus the year-ago comp of a loss of $2.39.

That looks fairly awful, but how were the cash flows, Sarge? Not much better. REE has generated an operating cash flow of -$54.508 million over the first nine months of the year. Tack on capex spending of $2.823 million and free cash flow over nine months comes to -$57.331 million. That's a pretty gnarly looking cash burn.

For the current quarter, though only one analyst covers the stock, a GAAP loss of $0.71 per share is expected on revenue of zero dollars and zero cents. Huzzah.

The Balance Sheet

As of September 30, REE held a cash position of $88.798 million and inventories of $1.751 million. That made for current assets of $101.503 million. Current liabilities add up to $31.639million, including short-term debt of $15.003 million. This leaves the company with a current ratio of 3.21, which is very healthy. There is some short-term debt, but there is enough cash on hand to take care of that loan, especially if the cash burn, which has been working itself lower on a quarterly basis, can continue to do so.

Total assets amount to $143.892 million, which includes nothing intangible in nature. Total liabilities stood at $86.185 million. This does include convertible promissory notes worth $9.837 million and total warrants liabilities of $30.92 million. There's enough cash on hand to, in theory, take care of the short-term debt, the promissory notes and the warrants. Of course, negative cash flows would prohibit taking care of all three, but this balance sheet is not awful.

Impressive...

For the third quarter, demand for "Powered by REE" vehicles surged as reservations grew 230% to $137 million, including long-term (post 2025) reservations for production.

The CEO

During the post-earnings conference call on December 17, CEO Daniel Barel commented:

"We are pleased to report Q3 2024 is yet another strong quarter across the board with accelerating demand for REE product line and technology from fleets and OEMs, along with the start of production of our flagship P7 truck. This milestone is supported by our strategic production partner, Motherson, and is backed by improved liquidity and strong confidence from top tier commercial banks. Having more than doubled our reservation value from $60 million to almost $140 million in one quarter, while improving our liquidity by 47%, is a testament to our continued devotion to delivering strong results in a fiscally disciplined manner."

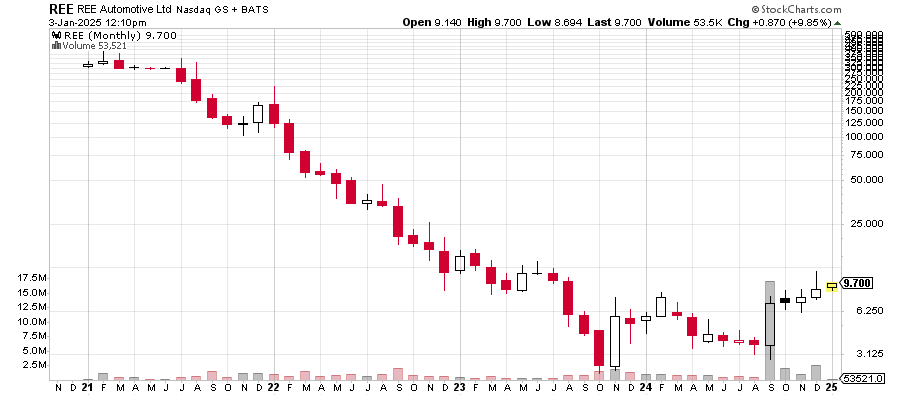

The Charts

First, I'll put up a monthly chart going back four years so readers can see how far these shares have fallen. The stock is down more than 98% since February 2021, but up 231% since mid-September.

Now, we'll zoom in a little bit:

REE has put together a double-bottom reversal pattern with a pivot point of $8.40. The stock has tried to break out and hit some resistance, but that attempt is clearly not over as the pivot has proven itself as support of late.

My Thoughts

For a short-term trade, if the pivot remains unbroken, I think $11 is very possible, at least technically. Investors have to understand just how speculative this name is and how negative cash flows, unless reversed, will rob this stock of its obvious potential.

Once one is "okay" with the risk, I would think that initiating and adding on tests of the 50-day simple moving average (SMA) from above would be a reasonable way to go about it.

Please note that due to factors including low market capitalization and/or insufficient public float, we consider several of REE to be a micro-cap stock. You should be aware that such stocks are subject to more risk than stocks of larger companies, including greater volatility, lower liquidity and less publicly available information, and that postings such as this one can have an effect on their stock prices.

At the time of publication, Guilfoyle had no positions in any securities mentioned.