Eyeing Palantir's Price Target, Bad Case of Mondays on Tuesday Morning, CPI Alert

Let's see what to expect from the consumer price index, chart PLTR as it trades below $183, check on Nvidia and China, and look at some misadventures in the Sargefolio.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Tiny Tim? No. The long-haired, ukulele-playing Herbert Khaury left us a long time ago. The Monday session on Wall Street did remind me of his 1968 hit song, though. There was indeed some light profit-taking on Monday. Not much, though. The air carried just a hint of risk-off style tension up and down Wall Street ahead of a potentially significant market catalyst. That could have been expected. I suppose.

This morning, the Bureau of Labor Statistics, yes that Bureau of Labor Statistics, will release its results for July consumer-level inflation when the latest addition of the consumer price index hits the tape at 08:30 ET. Expectations for July's core CPI have ticked up to an annual pace of growth of 3%, while the headline number lags slightly behind at 2.8%.

Will a 3 handle for core inflation pose problems for policy makers trying to persuade Fed Chair Jerome Powell to back a rate cut in mid-September? We may know more about the market's thoughts on this in just a few short hours. We'll know more about what Powell actually thinks of that late next week from Jackson Hole, Wyoming.

Regardless, the bulls got out of the way on Monday around lunchtime and let the bears have their way for the rest of the regular session. Still, the activity was light in nature, and there was very little to be taken away from the session as those of us who do try to ready the tea leaves go about our business.

Marketplace

There was some early strength on Monday. News that Nvidia NVDA and Advanced Micro Devices AMD had agreed to fork over 15% of Chinese chip sales driven revenue to the federal government was better received than I might have thought. Sticking with tech, investors also seemed to respond well early to news that Dell DELL was collaborating with Nvidia to create Dell's new AI Data Platform. Equity prices sort of eroded from there, while Treasury debt securities largely froze in place.

For the session, the S&P 500 gave up 0.25%, but did manage to post a high high and a higher low for a sixth straight session. This is despite the fact that three of those six sessions have been red candle days. The Nasdaq Composite lost 0.3% for the Monday session despite putting together a similar streak and despite setting a new all-time intraday record early on. The Dow Transports, at -1.03% suffered the worst session of all of the major to mid-major equity indexes. This was largely due to a beatdown across the maritime shipping space that impacted both Matson MATX and Kirby KEX.

Breadth

Eight of the 11 S&P sector SPDR ETFs closed out the Monday session in the red, led lower by Energy XLE and followed by Tech XLK. Communication Services XLC led the winners. It does need to be said, however, that no single fund among the 11 even came close to moving a full 1% on Monday from where it went out on Friday afternoon.

Losers beat winners by a rough five-to-four margin at both the NYSE and the Nasdaq. Advancing volume took just a 38.1% share of NYSE-listed trade, but a surprisingly high 59.4% share of Nasdaq-listed activity. Aggregate trade was lower on a day-over-day basis across the realms of NYSE-listings and the membership of the S&P 50), while activity actually expanded for Nasdaq-listed securities.

Going Into the CPI

As we all roll into Tuesday's main event, the Cleveland Fed's Nowcasting model is currently projecting a headline July CPI of 2.72% year-over-year on a month-over-month print of just 0.16%. That might sound encouraging, but the same model shows a core July CPI of 3.04% on month-over-month growth of 0.24%. It may be worth noting that with June headline CPI having printed at 2.67% (rounded to 2.7%), our beloved Hedgeye Nowcast shows a slight pullback from that pace in July. Markets would likely react well should that be the case.

Looking further down the road, the Cleveland Fed also released its quarterly "

Survey of Firms' Inflation Expectation." This survey probes CEOs and other corporate executives for their thoughts on where not just inflation broadly, but the headline CPI specifically will be over the next 12 months. These executives, in aggregate, for the Q3 survey now see the CPI peaking at 3.5% within a forward looking year. While that might sound a little scary, this is down from 3.9% from the Q2 survey which was conducted in April.

Extended Truce

The existing "trade truce," which is something far less than a "trade deal" between the U.S. and China was to have expired today. Aug. 12, already? My, doesn't time fly. On Monday, Pres. Trump told reporters that the truce had been extended for another 90 days while the two sides continue to work toward something more concrete.

In other China-related headlines, Bloomberg News is reporting that Beijing has apparently sent notices to a range of firms meant to discourage the use of Nvidia's H20 processors. The letters warn not to use the chips for government or national security related purposes specifically. Has Nvidia lost the opportunity that has been in front of the firm before the temporary ban on those less advanced but still AI-capable chips had been implemented?

Perhaps. That would put at risk not just the huge sales that Nvidia and AMD had missed out on earlier this year and even taken charges against those inventories. That would also put at risk the 15% sales tax that had been created solely for these kinds of sales by the two firms capable of designing these chips at scale.

On that note, on Monday, Pres. Trump indicated that he might actually allow Nvidia to sell a "not quite top of the line" version of Nvidia's Blackwell architecture designed chips to Chinese customers. The question becomes, what does the U.S. get in return? Negotiations will continue.

Trading

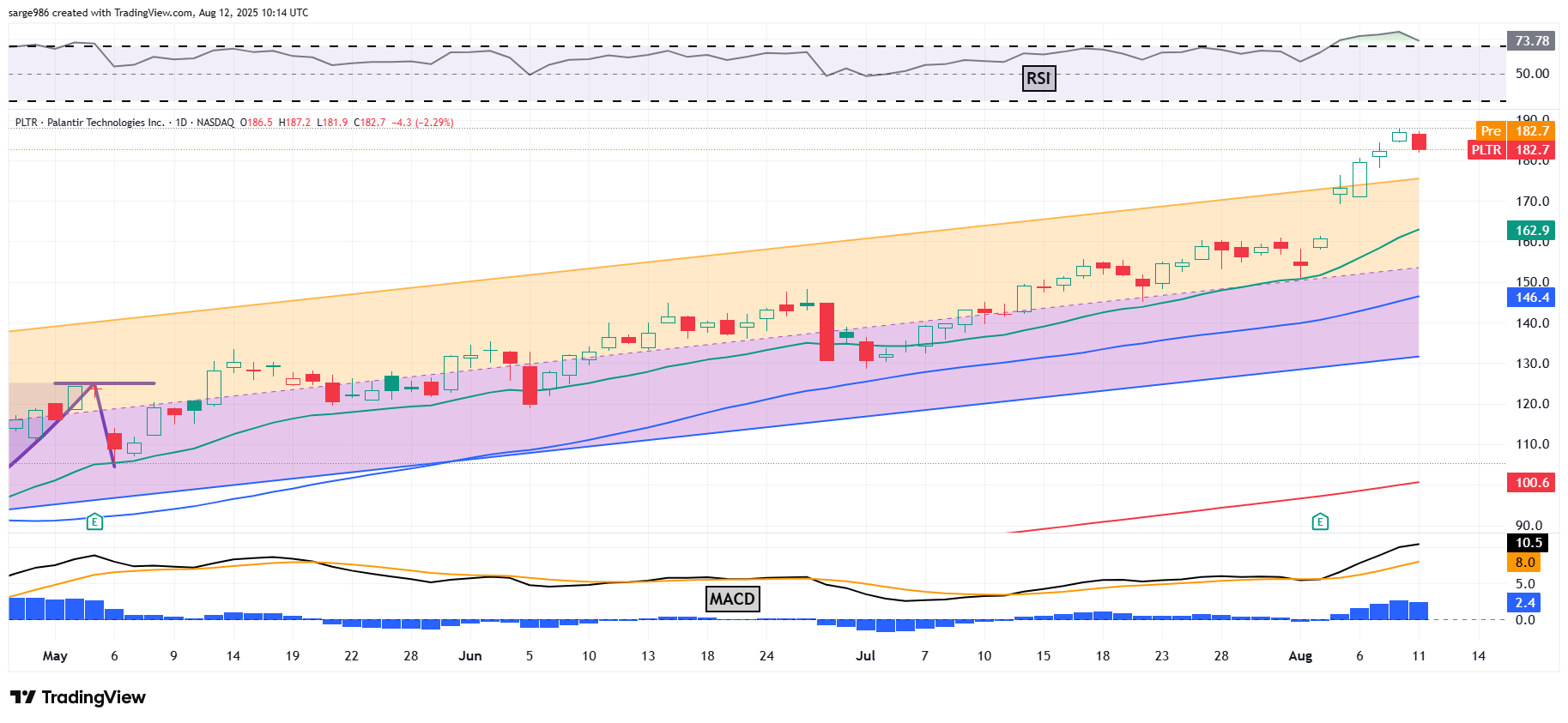

- When I wrote to you last week to increase my target price on Palantir Technologies PLTR from $181 to $205, the stock was trading with a $171 handle. This morning I see the shares trading just below $183 after peaking just below $188 on Friday.

The stock has tried to break out from our Raff Regression model and is trying to find support above the upper trendline of that model. This is the stocks' first attempt to break out from this model since mid-February and this is crucial. Holding the level would create an algorithmic reason to chase. (Yes, the algos can see the patterns that we talk about, because the kids who write the algorithms hire guys like me to read the charts for them.) A failure to hold this level? Our beloved Palantir needs to suffer a 11% drop in price just to test its 21-day exponential moving average and a jaw-dropping 20% just to test its 50-day simple moving average.

Fishing

My recent fishing expeditions are not yet going as well as one might have expected. Regular readers know that I have waded into the abyss saber unsheathed and gotten myself involved in the recent meltdowns at The Trade Desk TTD and Monday.com MNDY. At the moment I am down 3.4% and 5.3% respectively on those two positions. In my defense, I had to freeze my position in MNDY for more than three crucial hours on Monday morning as I worked on the article as I had to wait for my piece to become public information. I'll keep readers up on these two (mis) adventures.

Economics

(All Times Eastern)

06:00 - NFIB Small Biz Optimism Index (Jul): Expecting 98.6, Last 98.6.

08:30 - CPI (Jul): Expecting 0.2% m/m, Last 0.3% m/m.

08:30 - Core CPI (Jul): Expecting 0.3% m/m, Last 0.2% m/m.

08:30 - CPI (Jul): Expecting 2.8% y/y, Last 2.7% y/y.

08:30 - Core CPI (Jul): Expecting 3.0% y/y, Last 2.9% y/y.

08:55 - Redbook (Weekly): Last 6.5% y/y.

2:00 p.m. - Federal Budget Statement (Jul): Last $27B.

4:30 - API Oil Inventories (Weekly): Last -4.2M.

The Fed

(All Times Eastern)

10:00 - Speaker: Richmond Fed Pres. Tom Barkin.

10:30 - Speaker: Kansas City Fed Pres. Jeffrey Schmid.

Today's Earnings Highlights

(Consensus EPS Expectations)

Before the Open: CAH (2.03)

After the Close: CRWV (-.20)

At the time of publication, Guilfoyle was long NVDA, AMD, PLTR, TTD, MNDY equity.