Cleveland-Cliffs Steel Stock Might Have Hit Bottom After Decisive Loss

I will buy the name if shares can make this move next.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Not so bad. OK, kind of bad, but better than feared.

Cleveland-Cliffs CLF, which was up on Friday, is up yet again on Monday morning. Are you long this name? Me neither, after having been in and out of the shares more than once. Hey, it could be worse. You could be JP Morgan analyst Bill Peterson, Peterson initiated CLF a week ago with a "hold" rating while setting a target price of $7.50.

Needless to say, Peterson is ranked by TipRanks at one half of one star out of five. He is seen by that service as the 9,215th best analyst out of the 9,891 that they track. The truth is, though, that he is not alone. There are not many "buy" ratings on CLF. The most recent instance that I saw of a new or reiterated "buy" rating was more than two months ago. Let's explore.

On Monday morning, Cleveland-Cliffs released the firm's second quarter financial results. For the three-month period ended June 30, CLF posted an adjusted EPS of -$0.50 (GAAP EPS: -$0.97) on revenue of $4.934 billion. The top and adjusted bottom lines both beat Wall Street, despite the fact that the firm still recorded a decisive loss for the period as revenue generation contracted by 3.1% year over year.

Quarterly Notables

- Record steel shipments of 4.3 million net tons

- GAAP net loss includes $323 million worth of previously disclosed non-recurring charge-offs

- Steel unit cost reductions of $15 per net relative to Q1 2015

The CEO

Lourenco Goncalves, who is president, CEO and chair at Cleveland-Cliffs, had a lot to add to the firm's press release.

On the firm's recovery, Goncalves commented, "Our return to generating meaningful free cash flow and rapidly reducing debt is in sight. Domestic steel pricing remains strong, we have visibility into our cost reductions, and our order book remains healthy. Very importantly, the end of the five-year contract to supply slabs from Indiana Harbor to one of our competitors comes in less than five months. Due to the abnormally low index-based prices for slabs we have been exposed to in the last few months, this contract became a negative contributor to EBITDA and will not be extended."

Goncalves also had a lot to say about the current state of tariffs.

He added, “Cliffs is a major supplier of steel to the automotive manufacturers, and the Trump administration continues to show strong support to both the domestic steel and the domestic automotive sectors. We have started to see the positive impact that tariffs have on domestic manufacturing, protecting domestic jobs and national security. We expect this trend to continue, promoting the resurgence of the American automotive industry supported by a thriving domestic steel industry.”

Finally, in conclusion, Goncalves struck an optimistic tone:

“Going forward, foreign competitors need to acquire steel capacity within the United States if they want to participate in this desirable market. As a publicly traded America-based company centered on automotive, electrical steels, stainless and plate, Cleveland-Cliffs’ assets, business and footprint are uniquely positioned to benefit from this new reality.”

Operations

As revenue contracted 3.1% to $4.934 billion, the cost of goods sold increased 4.3% to $5.143 billion. This took gross profit from $162 million for the year ago period to -$209 million. After accounting for all operating expenses, GAAP operating income/loss printed at -$498 million, down from $6 million a year ago. Once interest, non-operating income and expenses and taxes are factored in, GAAP net income/loss attributable to shareholders landed at -$483 million, down from the comp of $2 million for the same period last year. That works out to a GAAP EPS of -$0.97, which compares poorly to the year ago comp of $0.00.

Once adjusted for that previously mentioned $323 million in charge-offs (for idled facilities) and a number of lesser items, net income/loss attributable to shareholders becomes -$247 million, down from $50 million. After these adjustments, EPS printed at -$0.50, down from $0.11.

Guidance

For the full year, Cleveland reduced its expectations for capex spending from a rough $625 million to $600 million. Expectations for operating expenses were cut from about $600 million to $575 million. Finally, projections for depreciation, depletion and amortization were increased to a rough $1.2 billion from $1.1 billion due to the accelerated depreciation of the firm's idled facilities.

Fundamentals

For the period reported, Cleveland generated operating cash flow of $45 million, down from $519 million a year ago. The firm spent $112 million on property, plant and equipment, leaving free cash flow of -$65 million, down from the year ago-comp of $362 million. Obviously, the firm is in no position to return capital to shareholders.

Glancing at the balance sheet, at quarter's end, CLF ran a cash position of just $61 million and inventories of $4.699 billion placing current assets at $6.687 million. Current liabilities add up to $3.277 million, which is mostly accounts payable. That puts the firm's current ratio at a quite robust 2.04, but its quick ratio at a much less muscular 0.61.

Total assets amounting to $20.471 billion, of which $2.999 billion or 14.7% is in goodwill and other intangibles. That is not an issue. Total liabilities less equity comes to $14.429 billion, of which $7.727 billion is in the form of long-term debt. That's a bit tough to look at, but it should be a driving force in returning the firm to positive free cash flow.

My Thoughts

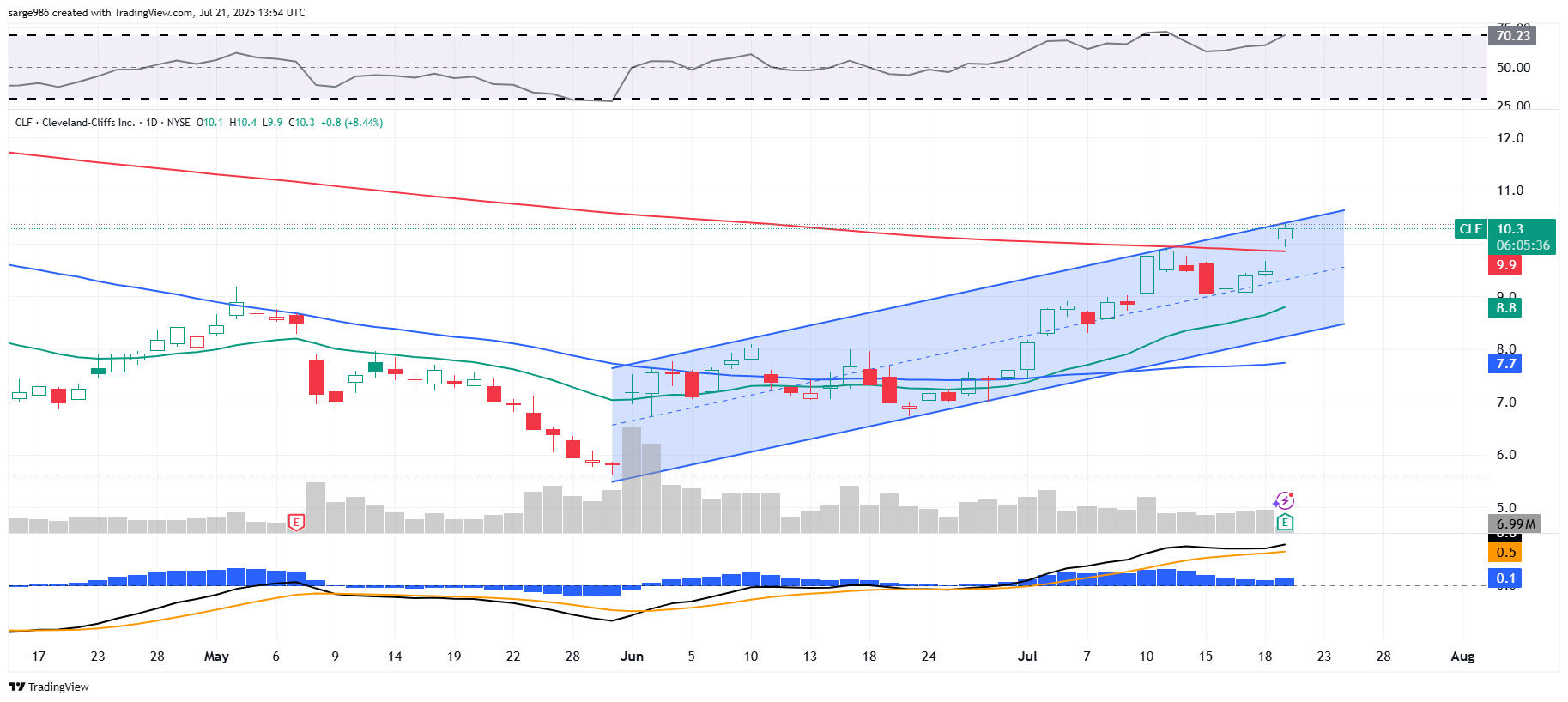

There's not a lot to like in the quarter reported. There is some welcomed guidance on the firm's ambitions to cut costs and become more efficient. The CEO seems to be relying as much upon the president's trade policy as anything else in order to help right the ship at CLF. I do see what young Peterson, mentioned at the top of the page, saw when he took a negative view of the name. That said, there is a chance that the stock has bottomed, at least for now. Let's take a look at the chart:

Readers will see that since late May when the shares hit a near five-year low, CLF has developed an upward sloping trend well defined by an ascending channel. At first I thought I saw a rising wedge pattern of bearish reversal, but upon prolonged analysis (and some measuring), I just do not think it's there. Unlike wedges, channels are patterns of continuance, unless of course something breaks and that something can break in either direction.

Readers will also note that relative strength is powerfully strong, but not yet technically overbought, while all three components of the daily MACD are exhibiting signs of bullishness. The histogram of the nine-day EMA is above zero, while the 12-day EMA is above the 26-day EMA with both of those lines also above zero and rising.

Lastly, but probably most importantly, the stock has just retaken its 200-day SMA. If held, this could force portfolio managers to increase long-side exposure. In addition, should this line hold, the stock will be making a third attempt to break out from the channel to the upside. That's my signal. Don't worry about missing the $5.63 low or the massive (in percentage terms) gains missed. This stock holds the 50-day line and breaks from the upper trendline of the channel, this stock will find a spot in the Sarge-folio.

At the time of publication, Guifoyle had no positions in any securities mentioned.