Buy or Hold? Strategies for 3 Energy Giants With Rich Yields

Enbridge, Energy Transfer and Enterprise Products Partners offer rich yields, but only two are priced for new money.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

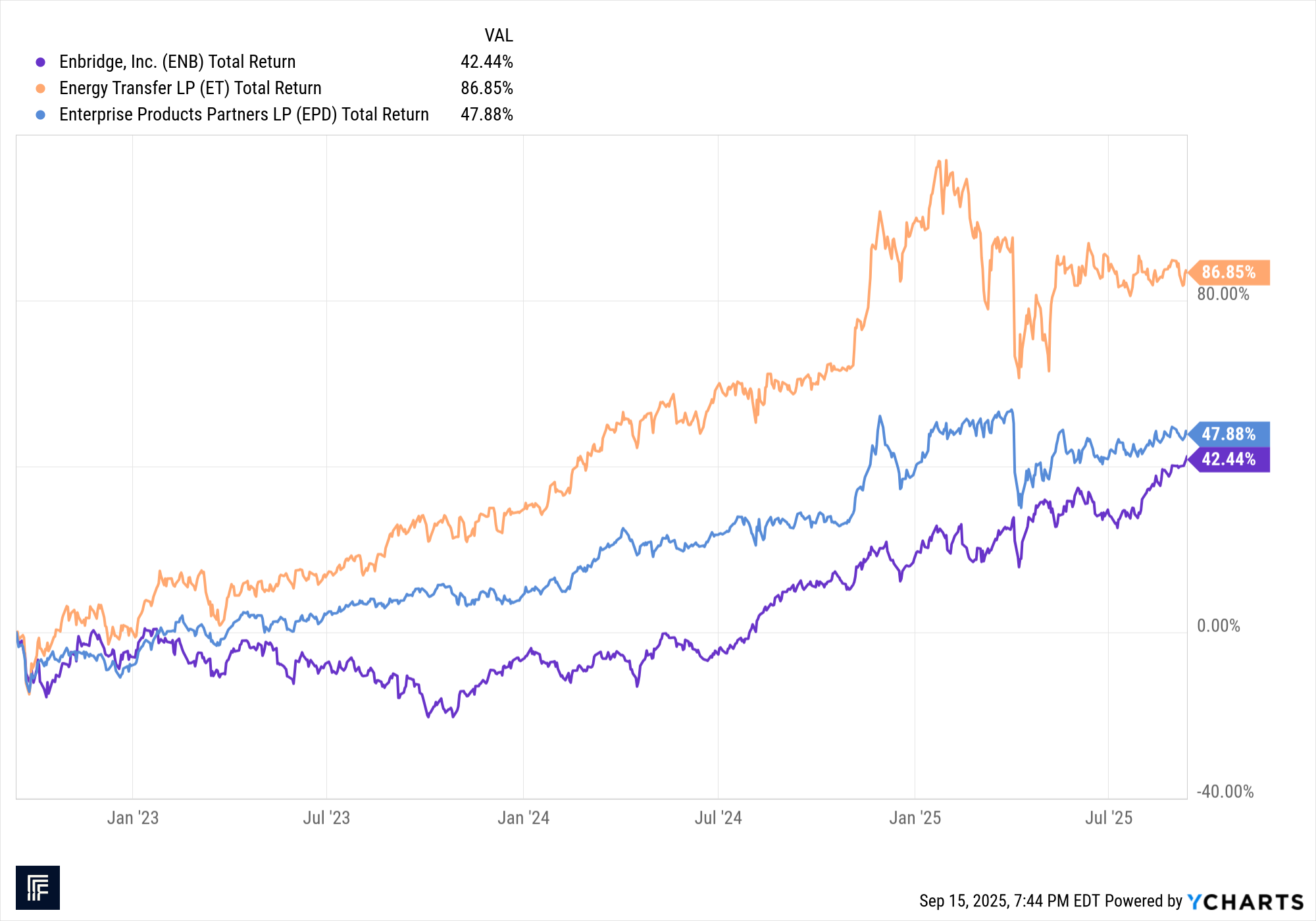

If you’re hunting for reliable income, it’s easy to get drawn to the biggest names in pipelines — Enbridge ENB, Energy Transfer ET and Enterprise Products Partners EPD.

They all throw off hefty yields and run vast networks that power the economy. But while the dividends look similar on the surface, the value story doesn’t. Right now, only two of these stocks are offering both strong income and upside. The other is a great company — just not at the right price yet.

Enbridge (ENB): Quality, But Fully Valued

Yield: 5.7%

Dividend Growth: 3%

My Take: Hold

Enbridge operates Canada’s Mainline crude network, major U.S. gas pipelines and the largest natural gas utility in North America. About 95% of its cash flow is tied to long-term contracts, which makes it dependable.

The company has raised its dividend for more than 30 years and plans to keep it growing modestly. Large new gas utility acquisitions and LNG pipeline projects should support steady earnings growth.

But there are headwinds. Enbridge carries heavy debt, faces legal risk on its Line 5 pipeline in Michigan, and could lose volumes to the new Trans Mountain Pipeline.

At around $49 a share, ENB looks fully priced. It’s a solid income stock to hold, but I’d wait for it closer to the low $40s to build a new position.

Energy Transfer (ET): High Yield With Room to Run

Yield: 7.5%

Distribution Growth: 3% to 5%

My Take: Buy

ET runs one of the largest midstream systems in the U.S., spanning pipelines, storag, and export terminals. Most of its revenue comes from fee-based contracts, which cushions cash flow from energy price swings.

ET has the highest yield of the group and strong coverage, and management is still raising distributions. Analysts see double-digit return potential combining that payout with growth projects coming online in 2026 to 2027.

Risks include legal noise around the Dakota Access Pipeline, high debt and execution risk on large projects.

Still, for investors seeking income with upside, ET offers the most compelling blend of yield and growth — and it still trades below fair value.

Enterprise Products Partners (EPD): The Durable Core Holding

Yield: 6.9%

Distribution Growth: 2% to 4%

My Take: Buy

EPD is the most conservative of the three. It dominates the natural gas liquids market, owns massive Gulf Coast export terminals, and has 28 straight years of distribution hikes.

Over 80% of its revenue comes from fixed-fee contracts, and it carries low debt with long-term fixed interest costs. That gives it resilience in both rising-rate and weak-energy environments.

Its growth is slower but steady. With a $7.6 billion project backlog coming online through 2026, EPD should keep growing its payout from a very solid base.

This is the “sleep well at night” choice — the one I’d anchor an income portfolio around.

A Quick Word on Taxes

ENB is a Canadian corporation that pays regular dividends reported on a 1099-DIV. In taxable accounts, Canada withholds 15%, but U.S. investors can usually claim that back as a foreign tax credit, and the dividends qualify for lower U.S. tax rates.

In IRAs, many brokers can avoid the Canadian withholding if they file the right forms. In contrast, ET and EPD are U.S. master limited partnerships (MLPs). They issue a Schedule K-1 instead of a 1099, and most of their payouts are tax-deferred return of capital — not taxed when received, but they reduce your cost basis and create some ordinary income on sale. Holding MLPs inside IRAs can trigger UBTI tax if income tops $1,000 per year, so most investors prefer to hold ET and EPD in taxable accounts and ENB in either taxable or IRA accounts.

Bottom Line

- Want stability? ENB fits — but wait for a better price.

- Want income with growth? ET is the standout.

- Want safety and consistency? EPD is your anchor.

In my view, ET and EPD are the two most compelling at today’s prices. ENB is a great business — just not a buy until it gets cheaper.

I encourage your feedback and comments. Happing investing!