AT&T's 'Out of Control' Debt Makes It Un-Investable

As the stock rises after earnings results, I'm planning a short‑term short position on today’s strength.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Wednesday morning, AT&T (T) released its fourth-quarter financial results. For the three-month period ended December 31, AT&T posted adjusted EPS of $0.52 (GAAP EPS: $0.53) on revenue of $33.466 billion.

These top and bottom-line numbers both beat the Wall Street expectations, while the sales print was good enough for year-over-year growth of 3.7%.

Operations

While AT&T was growing revenue 3.7% to $33.466 billion, total operating expenses were up 2.6% to $27.678 billion. That left GAAP operating income at $5.788 billion (+8.7%). After accounting for interest other income and expenses and taxes, the company was left with GAAP net income of $3.788 billion (-7.2%). That decline was largely due to a change in the equity value of the net income of AT&T's affiliates.

This all works out to GAAP EPS of $0.53, down from the year-ago comp of $0.56. After adjustments, the EPS print landed at $0.52, up from the year-ago comp of $0.43.

Guidance

For the fiscal year just started, AT&T is projecting wireless service revenue growth in the low single digits (percentage-wise) and broadband revenue growth of 7% plus. Capital expenditures are seen at $23 billion to $24 billion with free cash flow of $18 billion. That is in line with expectations.

The company also sees adjusted EPS of $2.25 to $2.35. Wall Street was looking for something down around $2.23 and that is the primary reason for the stock's upward thrust on Wednesday.

Fundamentals

For the period reported, AT&T generated operating cash flow of $11.32 billion. Out of that came capex spending of $6.781 billion and payments of vendor financing of $358 million. After that, free cash flow landed at $4.181 billion. Out of this number came cash dividend payments of $2.169 billion.

Moving on to the balance sheet, the company ended the period with a cash position of $18.234 billion and inventories of $2.42 billion. This left current assets at $48.732 billion.

Current liabilities add up to $53.78 billion, including $9.011 billion in debt maturing within a year. That looks awful, but advanced billings and customer deposits (deferred revenue) came to $4.266 billion. At the headline, the current ratio stands at 0.91, which is awful.

Adjusted for those deferred revenues, that ratio rises to 0.98, which is still awful. That said, this adjusted ratio stood at 0.73 a year ago, so this weak balance sheet is indeed much stronger than it was 12 months ago.

Total assets amount to $420.198 billion, including goodwill and other intangibles of $68.679 billion. That's just about 16% of the whole, so not a concern in my book. Total liabilities less equity comes to $293.707 billion, including long-term debt of $127.089 billion. That's not only daunting, but it's also up almost $9 billion over 12 months. Yikes.

My Thoughts

Cash flows are strong. The balance sheet is weak, but less weak than it was. The company's debt load is out of control and getting worse. That cash flow should be put to better, more responsible use.

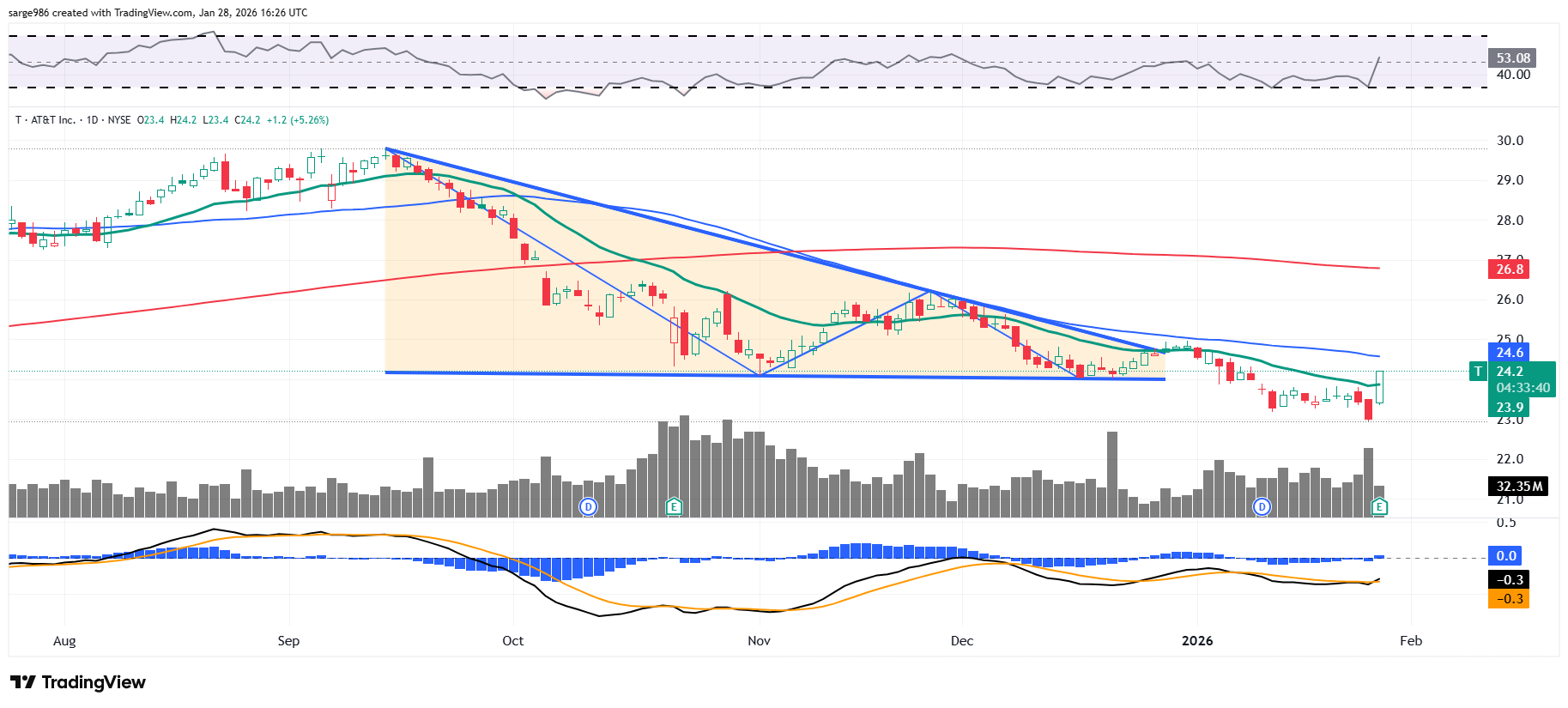

In the chart above, readers will see a very visible descending triangle of bearish continuation that appeared to work quite well until Wednesday morning's rally.

I don't see the positivity in Wednesday's report that others apparently are. The stock is up around 5% on Wednesday as I type. If it is still trading there when this article becomes public information and I am free to trade, I will be taking a short-term short position in the stock. As I have said for several quarters now, for me, AT&T remains un-investable.

At the time of publication, Guilfoyle had no positions in any securities mentioned.