A Stock Priced Well Below Worst-Case Scenarios — And for Outsized Gains

Buying shares when they are depressed, due to temporary problems, is one of the surest ways to make great long-term returns.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Even excellent companies can run into unexpected business hurdles over the years. Buying their shares when they are depressed, due to temporary problems, is one of the surest ways to make great long-term returns.

A glance at Helen of Troy’s HELE major bands (see graphic below) suggest most of us have at least some of their products in our homes right now.

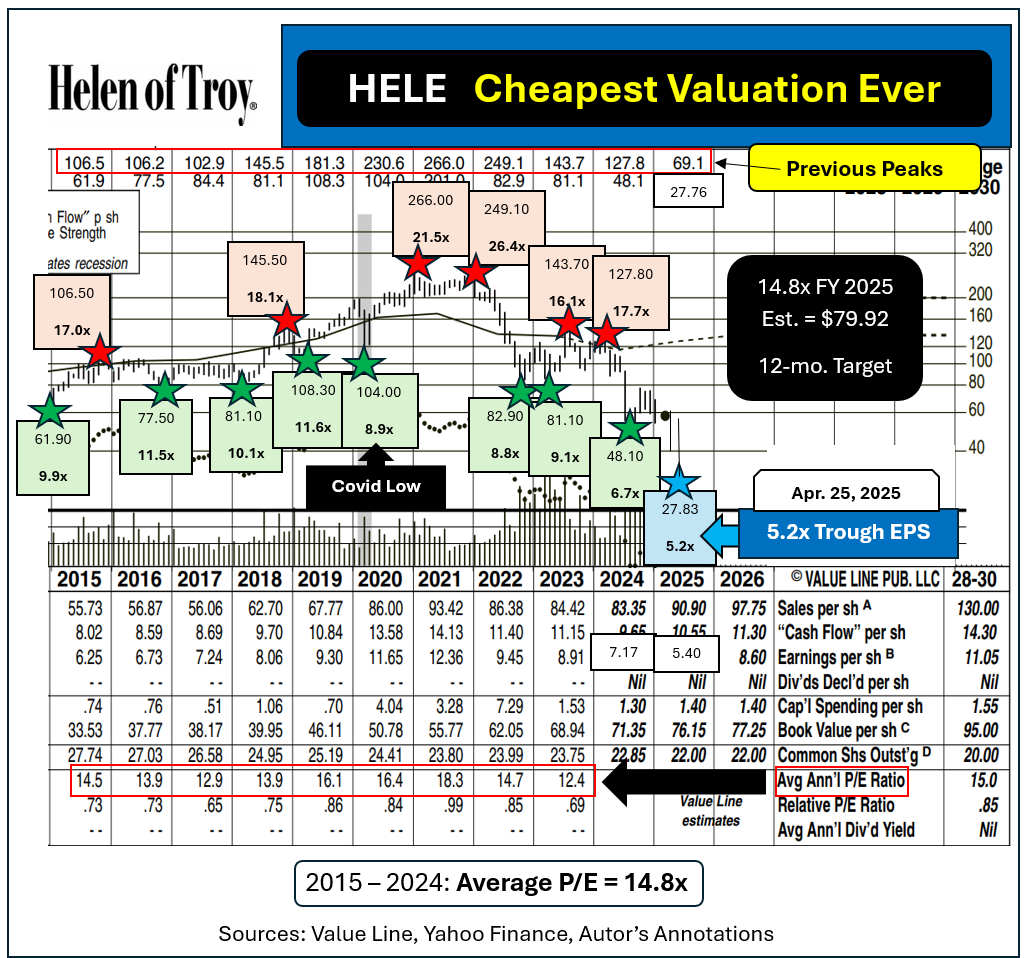

HELE sold for peak share prices well above $200 during each of the three years 2020 through 2022. It offered traders exit points of between $102.90 and $266 during each full calendar year from 2015 right through 2024.

As of April 25, 2025, the stock was offered at a post-2012 low of $27.76 intra-day.

That price was just 3.9 times HELE’s adjusted earnings per share of $7.17 in FY 2025 (ended Feb. 28, 2025).

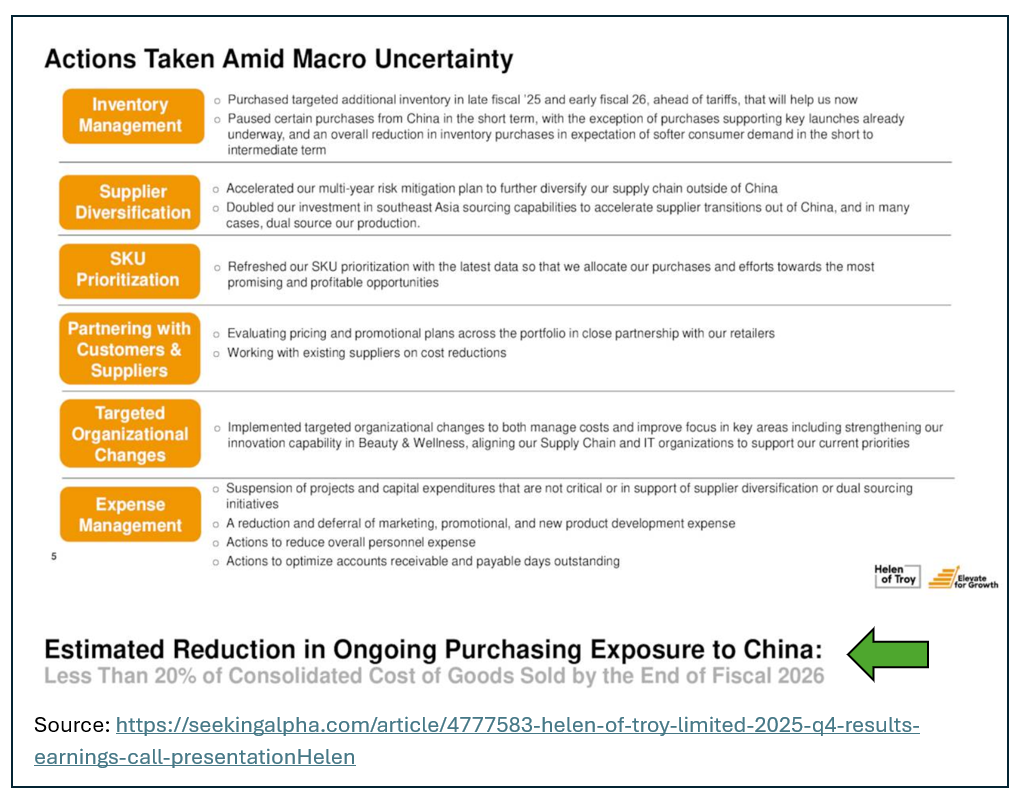

Why have the shares been hit so hard? Uncertainty over tariff policy concerns.

Management is doing everything possible to minimize any short-term damage from this source as noted below.

With the stock down 89.5% from its all-time peak of $266 I am willing to bet the price is below any worst-case scenario that is likely to unfold.

My previous article titled, "Revenge of the 'Dumb Money' Nerds," noted that the Covid-panic market decline hit bottom on March 23, 2020. That was significant as government-imposed business and civil shutdowns had just begun, rather than ended.

Smart buyers did not wait for good news to start accumulating shares. They bought at fabulous prices that would not be available when everybody else could see that “the coast was clear.”

Stock price action tends to lead business cycles by at least six to 12 months. April’s extreme plunge has likely already considered the effects of a possible recession.

Owning Helen of Troy now means accepting that we cannot be sure what FY 2026 EPS will be. In its March 7, 2025 issue Value Line projected adjusted EPS of $7.90 for HELE in the current fiscal year.

FASTgraphs still uses $8.00 as its FY 2026 estimate for HELE’s year ahead.

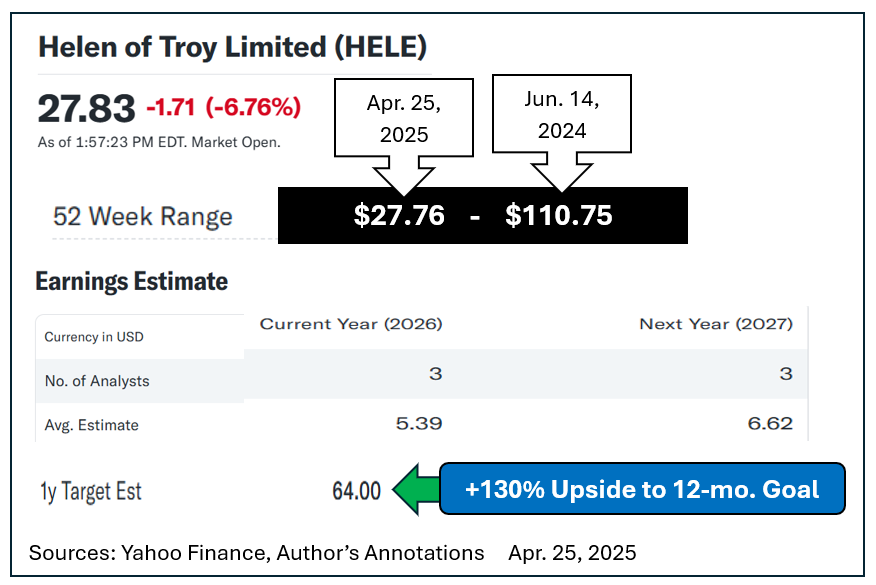

Yahoo Finance has reduced its forward estimate for the firm to $5.39 per share.

United Airlines UAL issued both a recession estimate, and a non-recession estimate for this year on its recent quarterly earnings call.

To be conservative I am penciling in $5.40 for the current year’s adjusted earnings even though it could very well prove too low if tariff issues get solved before long.

What is HELE worth based even on that tepid EPS assumption?

From FY 2016 through FY 2025 (ended Feb. 28, 2025) HELE carried an average P/E multiple of 14.8x. Simply bouncing back to that typical valuation suggests a 12-month target price of nearly $80.

From $27.83 that implies around 187% in year-ahead upside potential.

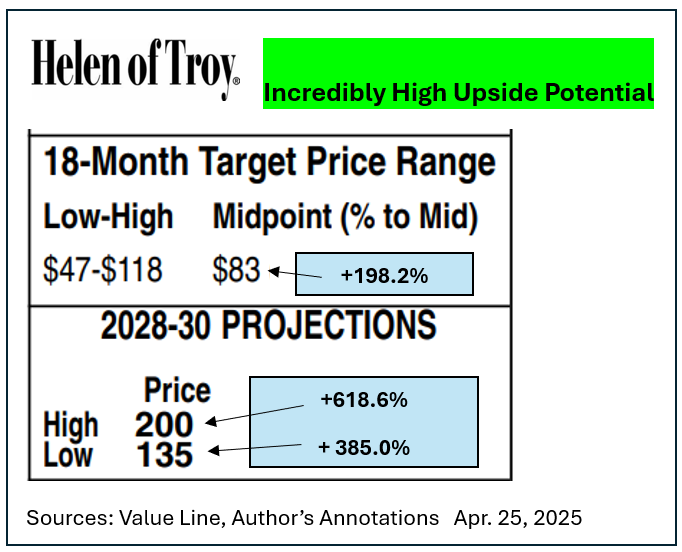

Just six weeks ago this was what Value Line was looking for on HELE over the coming 18 months and three- to five-year periods.

Those assumptions might need to be pared back while tariff levels are being renegotiated but they leave plenty of room for outsized gains regardless.

Yahoo Finance, the most pessimistic source I found of HELE’s near-term EPS, still projects the stock to reach $64 by this time next spring.

That goal price would deliver about a 130% gain from last week’s closing quote.

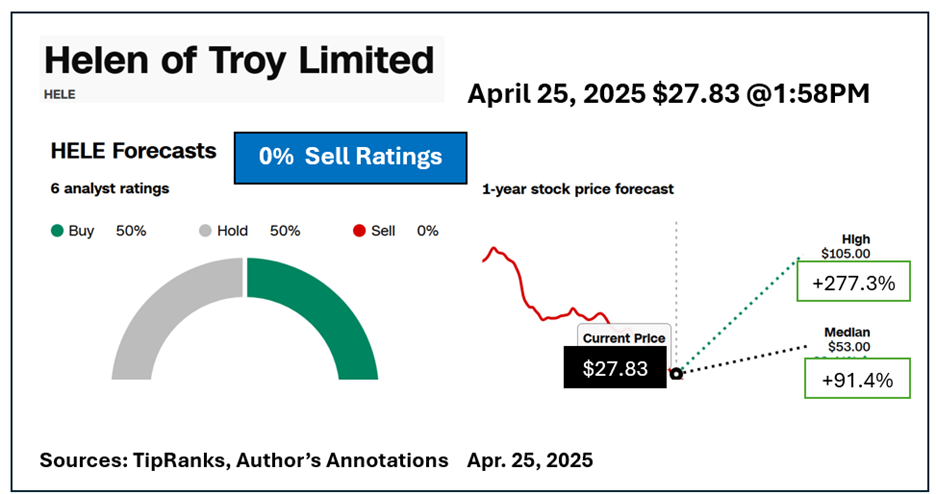

Tip Ranks research’s consensus of six analysts found three buy and three hold recommendations on HELE. Not one analyst called it a sell.

The median 12-month target was $53. The high-end goal was $105. Both are well within the stock’s trailing 52-week range of from $27.67 (set last Friday) to $110.75 (hit on Jun. 14, 2024.)

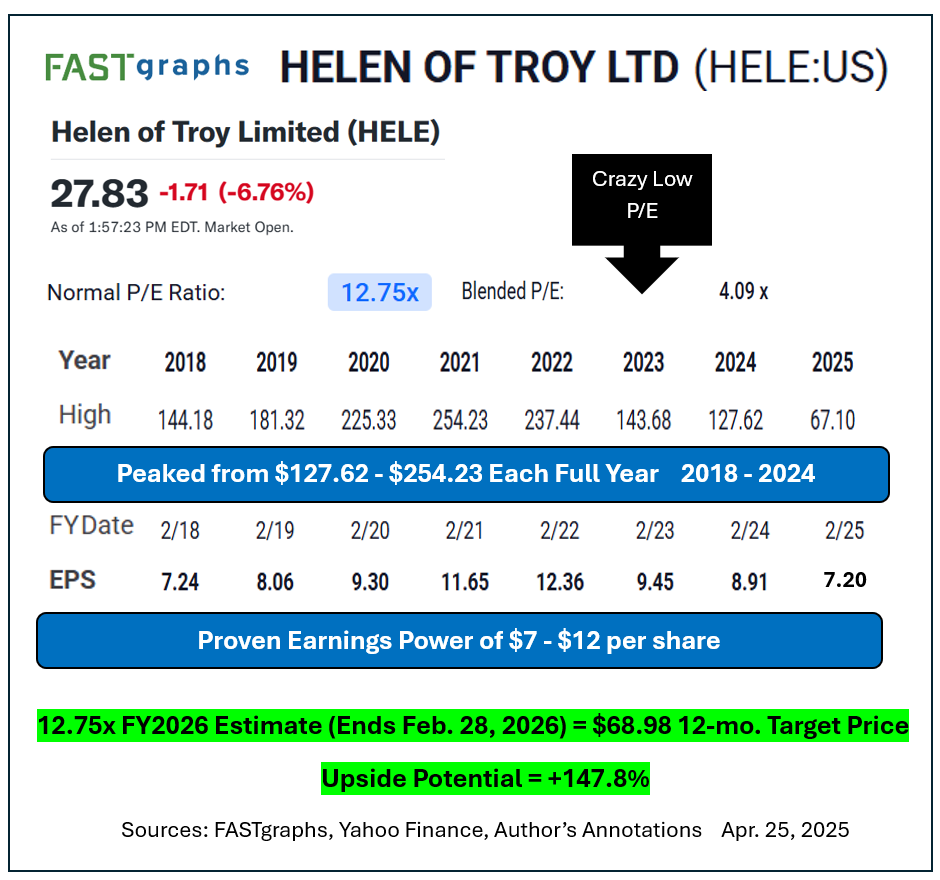

Quantitatively focused FASTgraphs is so far sticking with its $8 per share FY 2026 estimate for HELE. It calls a normalized P/E for the shares as 12.75x.

The data show HELE has proven earnings power of from $7-$12 per share. Applying 12.75 times $8 generates a year-ahead target price of $102, plus 267% from $27.76.

Using the more conservative $5.40 in EPS still produces a $68.98 one-year goal that is 147.8% above the current quote.

My belief is that the world’s tariff situation will be ironed out quicker than most people expect.

If that occurs, Helen of Troy could be an enormous winner for anyone buying at today’s absurd low price.

If things take longer to reach a definitive settlement there are almost certainly big gains to be made anyway. As noted earlier HELE has not changed hands at last Friday’s price since 2012.

HELE can be quite volatile. That is a good trait when you are purchasing near a 13-year low point. Its spring of 2018 low of $81.10 led to a quick rebound to $200 just ahead of the Covid period.

Panic selling in March 2020 then knocked the shares back to $104. By January 2021 Helen of Troy was selling for $266.

From under 4x trailing earnings and just 5.2x its lower-end estimate of the current year’s profits we could be in for a similar huge and fast rebound in price.

At the time of publication, Price was long HELE shares; and had positions in UAL shares or options.