A Small-Cap Worth Shorting?

I've got an idea. Hear me out.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

As I was meandering my way around a couple of stock screeners that I use looking for opportunity, I came across a name that I had never considered before. I am speaking of Turning Point Brands TPB. The stock, with a market cap of just $1.8 billion and trading at 34 times forward-looking earnings, currently trades with a $98 handle down from a recent high of $102.90.

It's not like Turning Point is not profitable.

For the company's fiscal second quarter, which was reported on August 6, it posted adjusted EPS of $0.98 (GAAP EPS: $0.79) on revenue of just $116.634 million. Those top-line and adjusted bottom-line numbers both easily beat expectations, while the revenue print was good for annual growth of 25.1%. Yes, despite the fact that those sales only amounted to less than $117 million. Turning Point did increase guidance for full year adjusted EBITDA at that time.

What Do They Do?

Turning Point Brands is a Louisville, Kentucky-based manufacturer, marketer and distributor of branded consumer products.

What kind of products?

Under the brand names Zig-Zag and Stoker's, the company principally markets and distributes rolling papers, tubes, finished cigars, make-your-own cigar wraps and related accessories. It also manufactures moist snuff tobacco under the Stoker's name and does contract work for loose-leaf tobacco products.

The company's products are available at roughly 220,000 retail locations throughout the U.S. and Canada.

What I Noticed

I noticed that while Wall Street is still projecting 23% sales growth for the current year, sales growth for next year is just expected to present at just 8.9% or so. I also noticed that the company has $109.9 million in cash on hand and a debt load of more than $293 million.

I also noticed that more than 35% of total assets were labeled as either goodwill or intangible. I thought that maybe that was a bit on the high side for a company most folks never heard of without a whole lot of revenue.

The company does produce positive free cash flow, about $52 million over the past 12 months, and is profitable, but is it overvalued? The S&P Small Cap 600 is currently trading at close to 16 times forward-looking earnings. As mentioned above, this stock is trading at 34 times. The company reports in early November.

My Thoughts

TPB is up 64% year to date, up 152% over 12 months and 315% over three years.

Am I willing to get short a name like this though I do see the bear case? I don't think so.

Am I relatively certain that TPB will move sharply one way or the other? Probably.

The stock broke out from this Regression model post Q2 earnings. For about three weeks now, the share price has been in a state of consolidation.

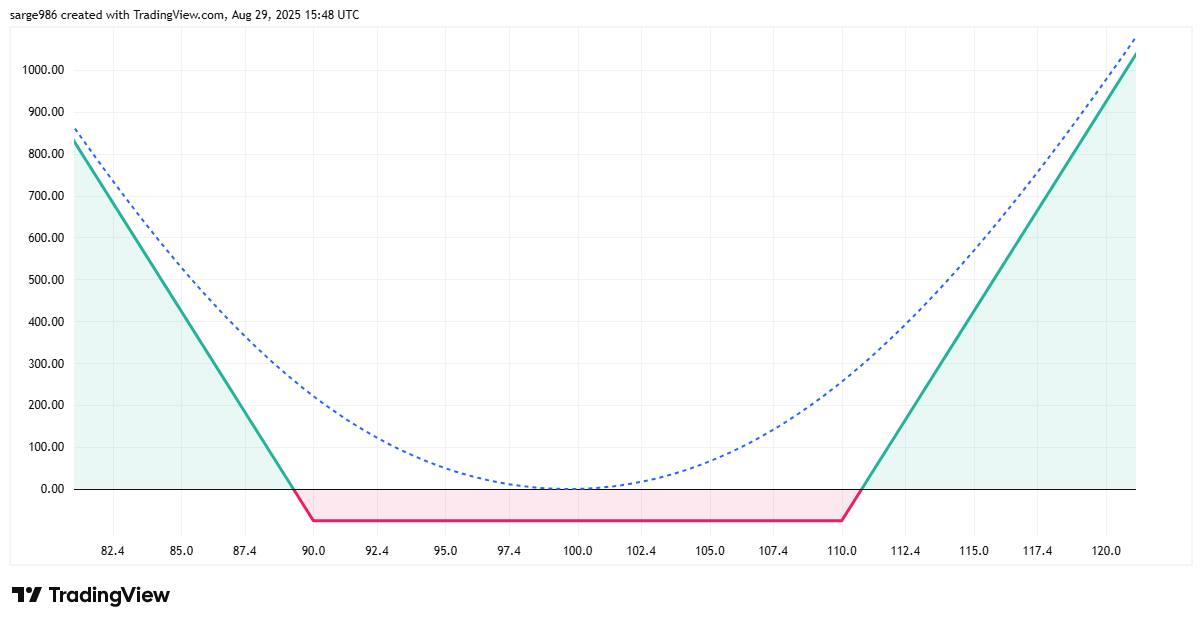

A trader could get long a $90/$110 options strangle expiring on September 19 for roughly $1.05. That's the risk-averse way to play any coming volatility in this name.

However, if said trader takes that strangle out to November 21 (after earnings), with the lack of liquidity in this market, the strategy could cost the investor as much as $10.20. If one works the order a little, he or she might shave about $2.00 off of that net debit.

Is it worth $8 to $10 ($1,000 per contract spread) to potentially capitalize on coming volatility? Perhaps. That's up to the trader, but at least the max risk is fixed.

Just an idea on pre-holiday Friday afternoon. Mulling it over myself.

At the time of publication, Guilfoyle had no positions in any securities mentioned.