Why We’re Skeptical About That Surprising December Housing Starts Report

Let's look beyond the headline numbers for a more accurate picture of what's going on and where we're headed.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

We continue to think one of the more important pieces of economic data we’ll get this week is the Flash February PMI report from S&P Global this Friday. But a few other pieces of data have been reported Wednesday, and it would be a mistake not to walk through them.

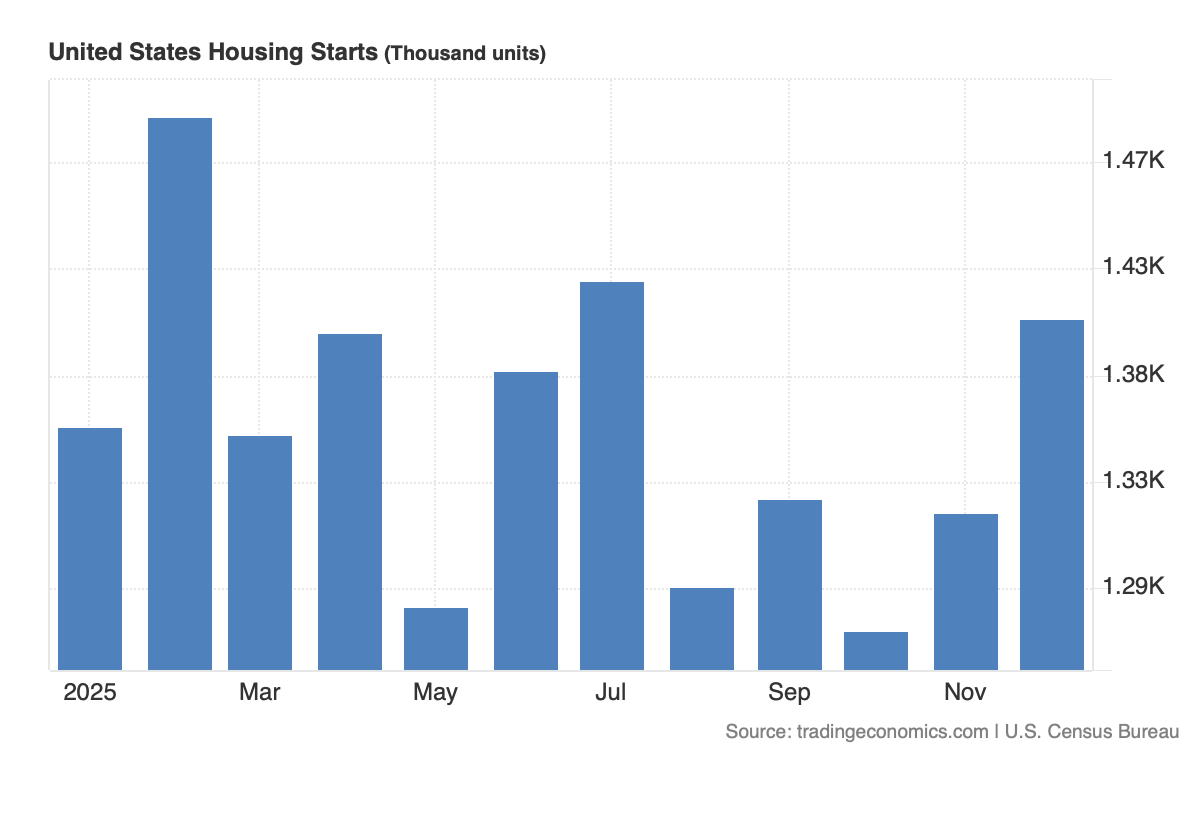

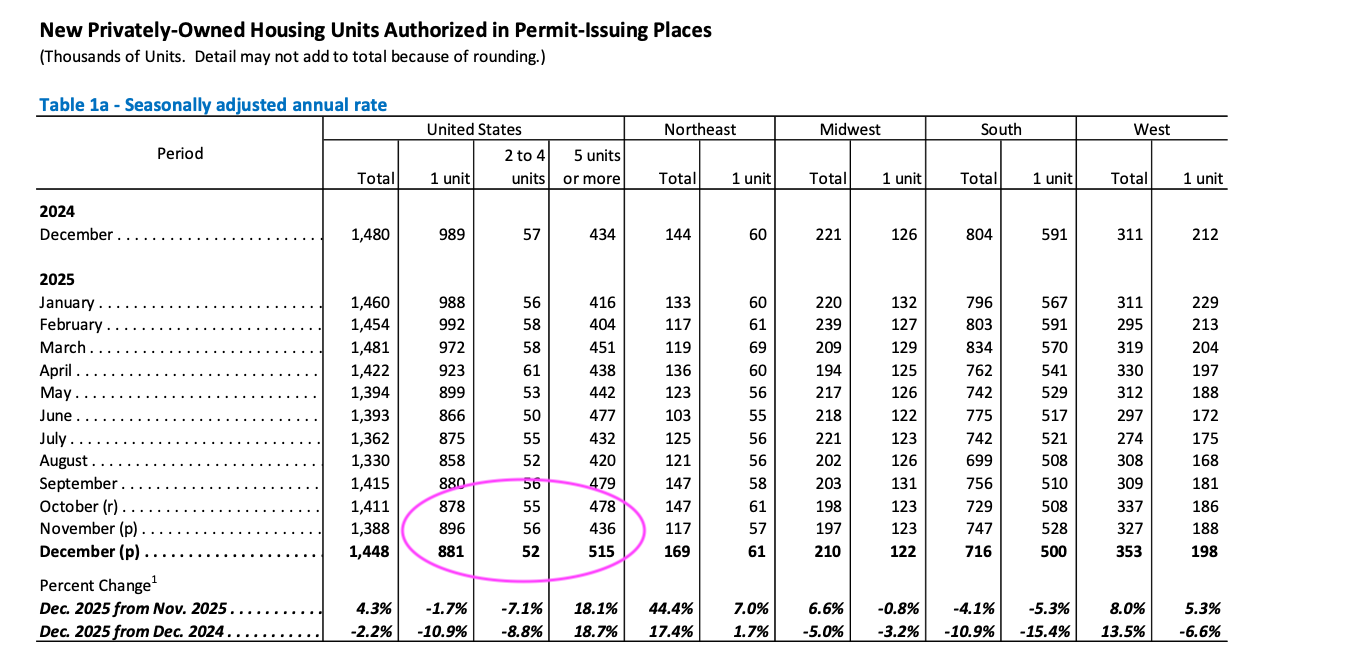

Wednesday's data for Housing Starts, like a few other pieces of late, catches us up on the tail end of 2025. What we see in the headline figure for November and December points to a rebound in total housing starts, but let’s remember there are two components for that headline figure — single-family housing and multi-family starts. Peering into that breakdown, we see the greater increase came in the multi-family category.

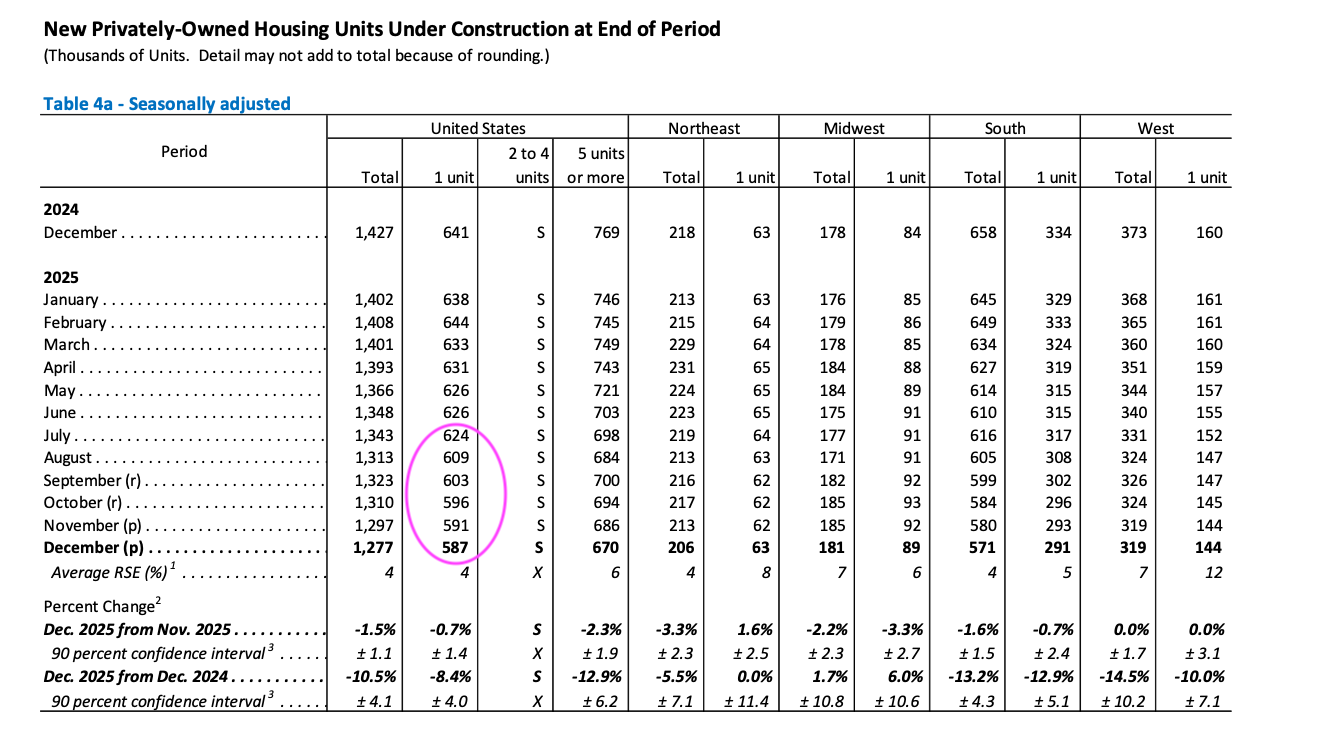

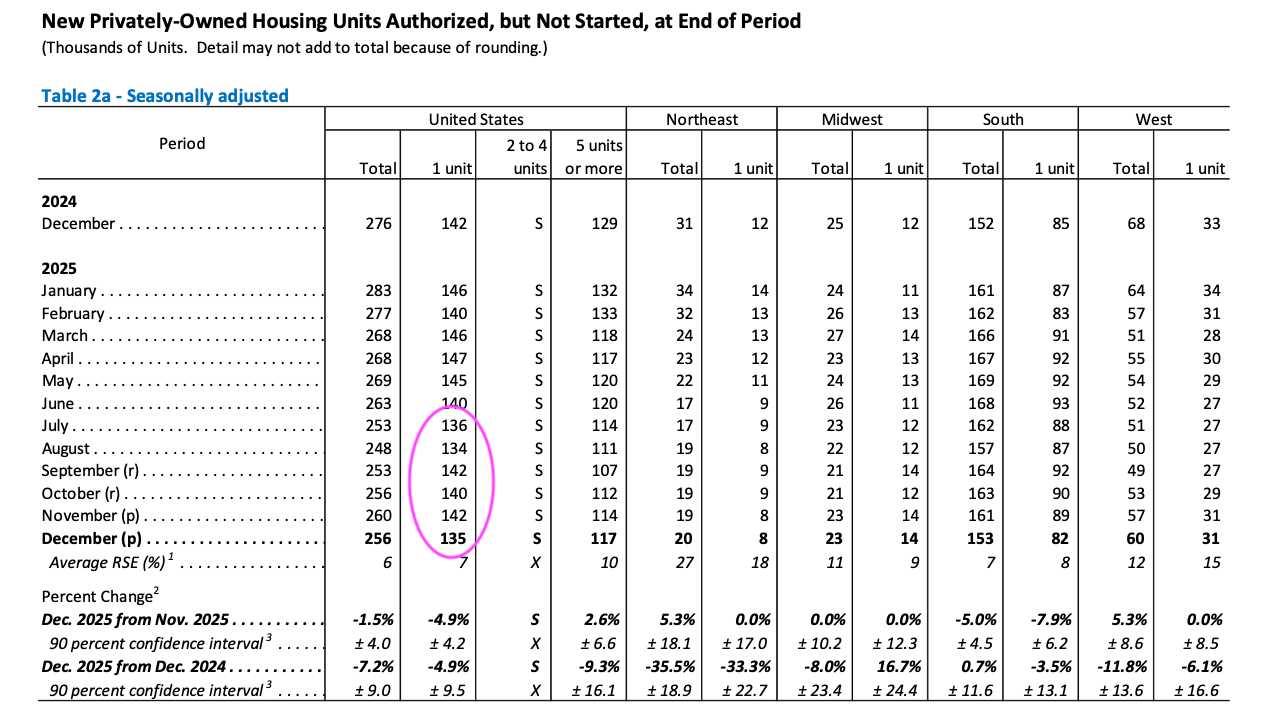

And then when we look at some other data in the report, namely the number of single-family housing units under construction at the end of December and the number of housing units authorized but not started at the end of December, we see a different picture.

This points to slow levels of single-family housing construction and weaker order levels, which explains the continued fall in single-family housing units not started amid the falling number of units under construction. We see that reflected in quarterly backlog levels reported by Toll Brothers (TOL) , which saw its December-quarter backlog fall to 5,051 units, from 6,312 in the December 2024 quarter.

Meanwhile, the recent bout of severe winter weather is going to throw a wrench into housing construction in the current quarter.

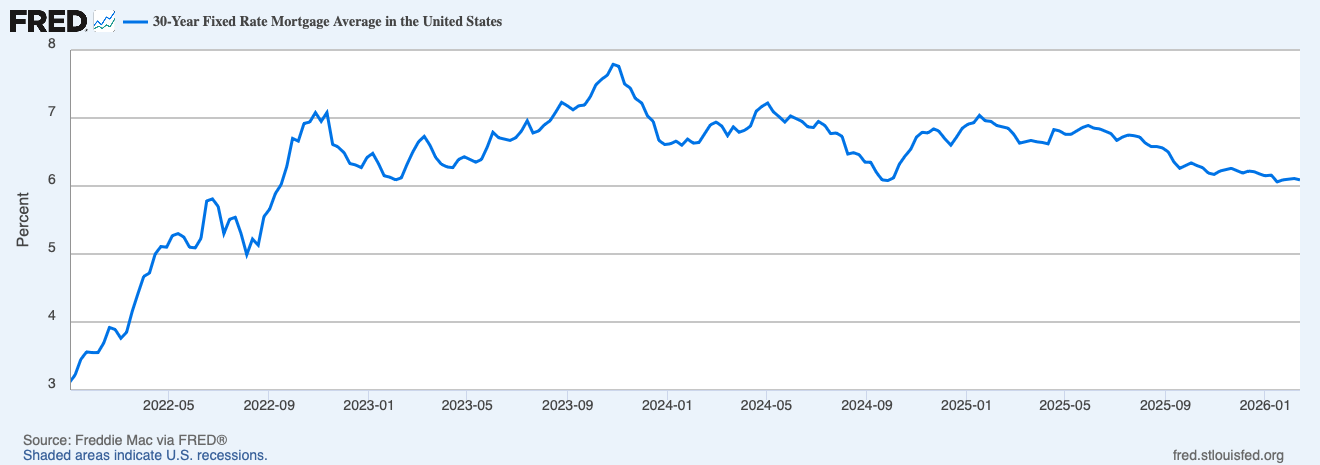

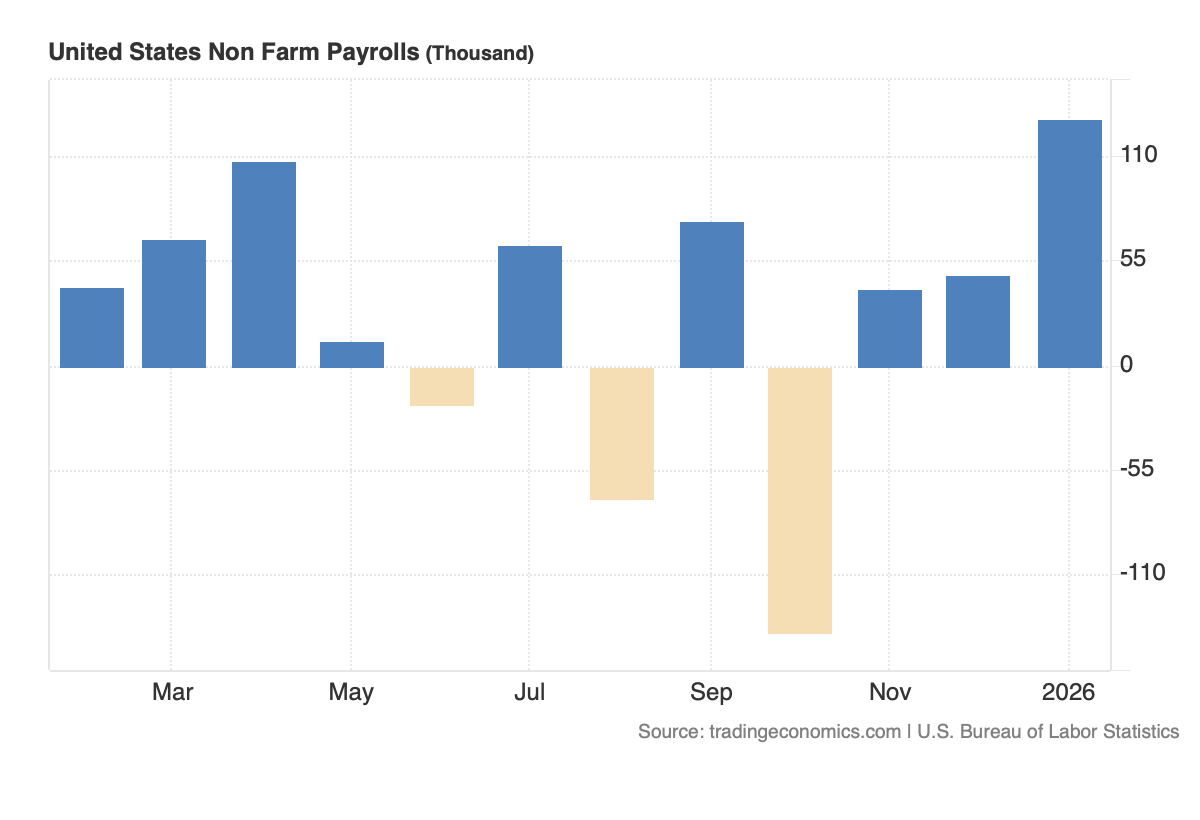

We’d also note the decline in those reported housing figures from the Census Bureau, shown above, relative to the decline in the 30-year mortgage rate during the second half of 2025. That reaffirms the relationship between the single-family housing market and the pace of job creation. Per the January Employment Report, just 19,000 jobs were added in H2 2025.

This means we will want to see a pick-up in job creation before adding a homebuilding play to the Pro Portfolio. Lower rates will be helpful, but it’s job growth and preferably wage gains we’ll want to see. The conundrum is that if we see an acceleration in job creation, it may take longer for those lower rates to emerge.

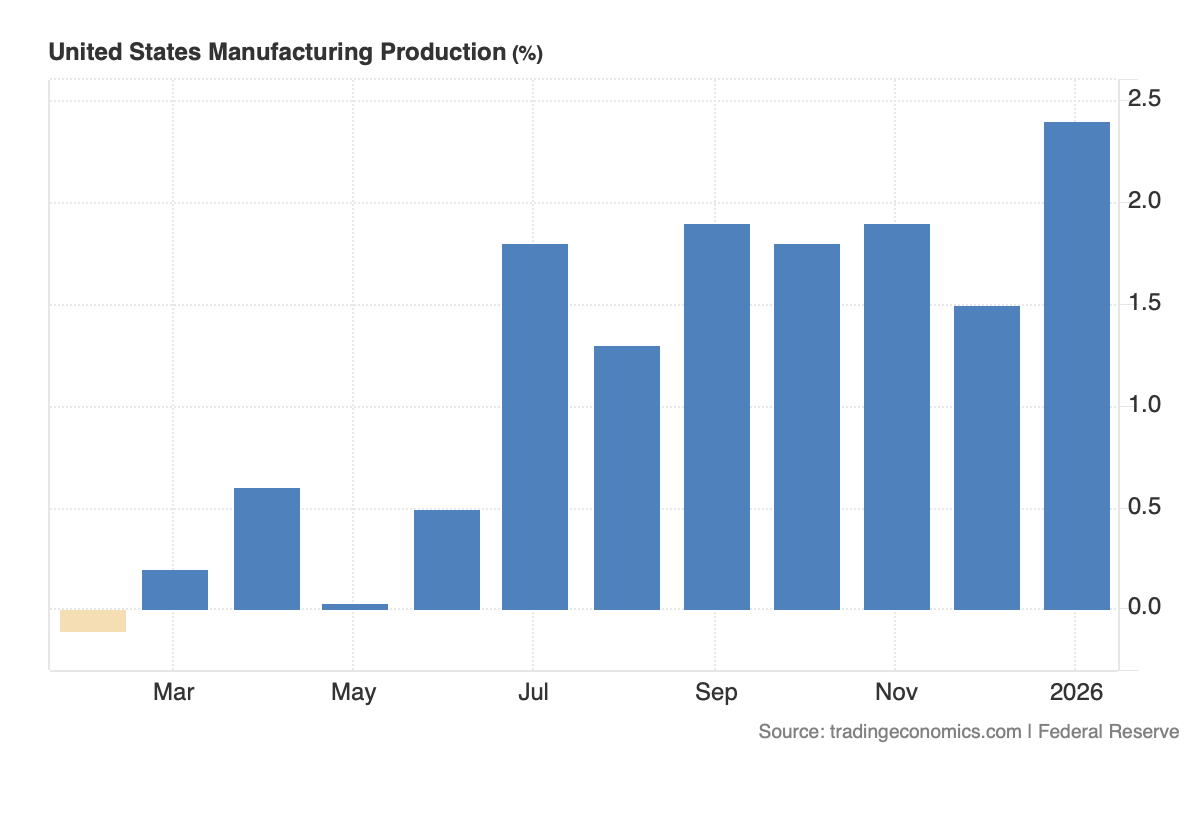

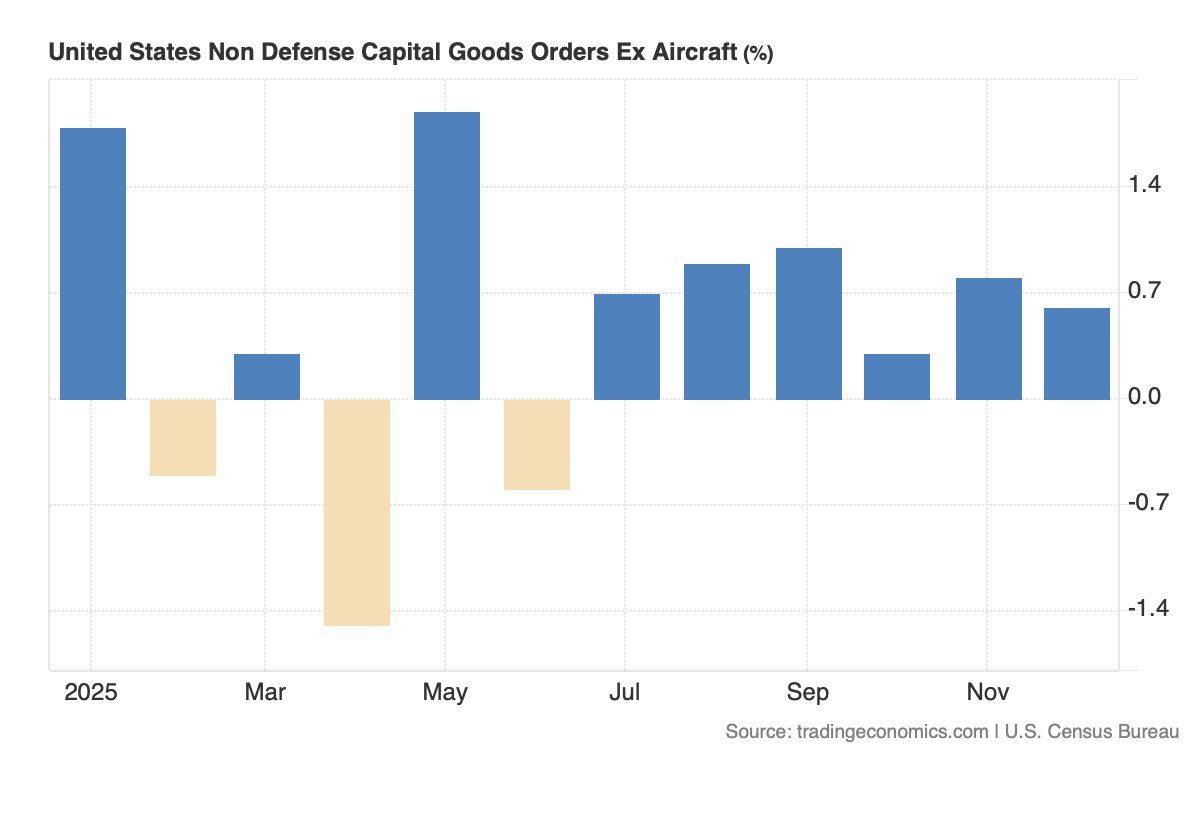

And when we look at the December non-defense capital goods orders ex aircraft, a proxy for business spending, and the January uptick in manufacturing production, it looks like that part of the economy is perking up. We’ll look for confirmation of that in Friday’s Flash PMI report, and if that is what we see, it would suggest the U.S. economy continues to hum.