Why Powell Could Quash Renewed Market Hope for Rate Cuts

Let's connect the dots from ISM’s March Services PMI report and other indicators.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Following up on our opening comments, let’s dig into today’s big piece of economic data, which is the ISM March Services PMI report.

Setting the table for that report, Tuesday’s March Manufacturing Services PMI showed a slowdown in that part of the economy, with inflation picking up, and employment falling. ADP’s upside surprise in its March Employment Change Report was largely on the services side of the equation.

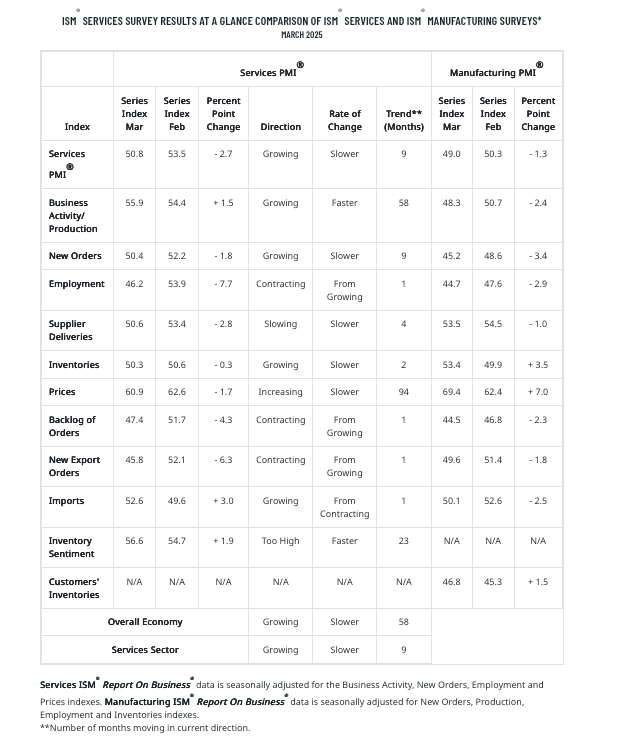

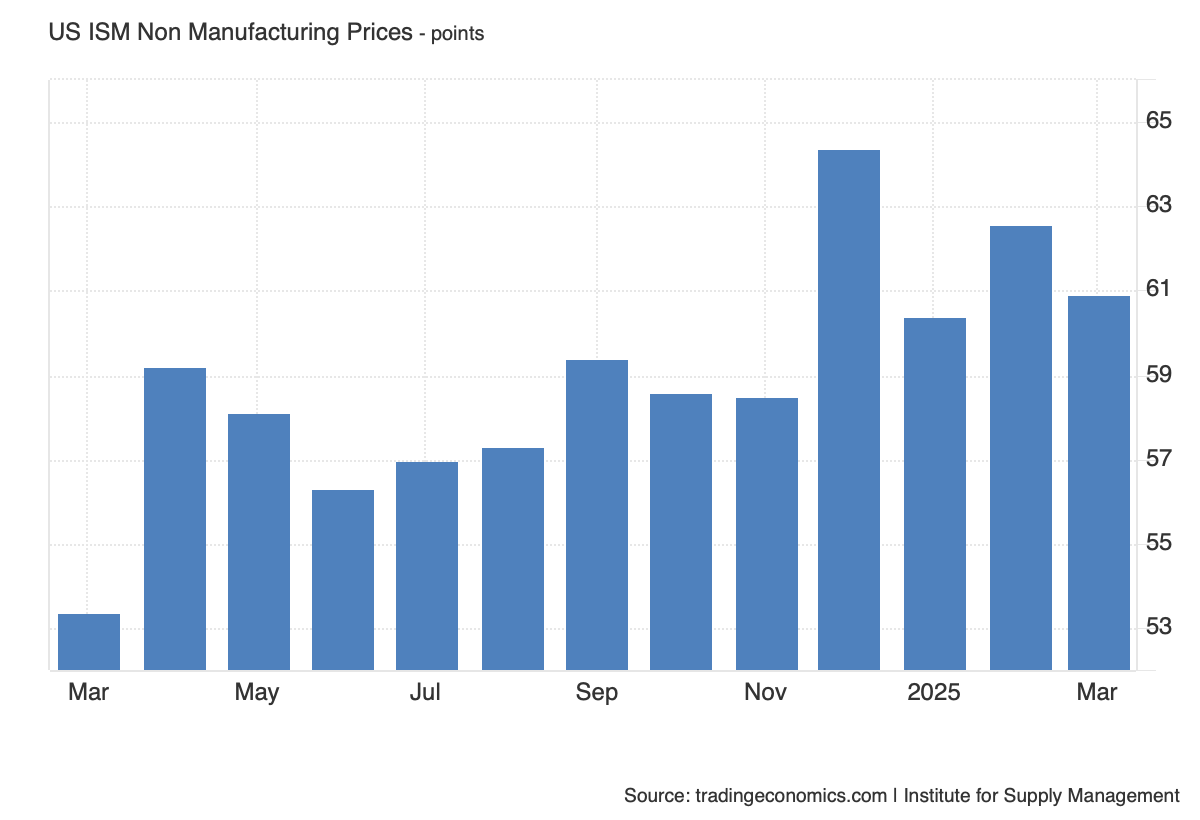

As we can surmise in the table below, while business activity in the Services sector picked up in March it was more than offset by declines in new orders, new export orders, and employment. And while the Prices line item dipped, it remained at its third highest level over the trailing 12-month period, indicating prices were still on the upswing just not as fast as in February.

Connecting the Dots

Our first reaction in parsing the data is that we are going to see GDP expectations for the March quarter revised lower from the Atlanta Fed, New York Fed, and others. Following Tuesday’s data, the Atlanta Fed’s GDPNow model moved to -3.1% for Q1 2025, but it will be the change in the New York Fed’s Nowcast model that we are more interested in seeing. We say that because its last update on March 28 pegged Q1 2025 GDP at 2.86% and that means its next one will include this week’s March data. Based on what we’ve seen so far, it’s a pretty safe bet to say that the 2.86% figure will be moving lower. How much lower, well, that’s the question.

Friday’s March Employment Report will shed more light on that potential answer. Looking back at the ISM table above, it shows a sharp drop in the Employment sub-index for both Manufacturing but also Services. In the Manufacturing PMI report the comment we called out was “destaffing” and in today’s Services PMI one it is “not adding headcount or resources.”

Balancing those findings with 155,000 private sector jobs found in ADP’s March Employment Change Report and the planned 275,240 job cuts in the March Challenger Job Cuts Report, we could see a disappointing March jobs report Friday. As of now, the market forecast calls for 135,000 nonfarm payrolls to have been added in March, with 127,000 in the private sector. The delta between those two figures implies a modest gain in government or public sector jobs. The odds of that are rather low, in our view, but here too we have to be careful not to read too much into the March Challenger Job Cuts figure because it is for planned layoffs, not reported ones.

The Challenger Report also saw a sharp decline in corporate hiring plans to 13,198 in March from 34,580 in February. That’s a small snapshot relative to what’s captured in the overall monthly Employment Report, but paired with the Manufacturing and Services new order declines found in the March ISM data, it points to a slower-revving economic engine at the start of the current quarter. And that’s before any real impact is felt from Trump’s reciprocal tariffs and the potential response to those from other countries.

What Could Powell Say Friday?

Lining up GDP prospects for the current quarter and those for inflation, we are likely to hear "stagflation" being slung around quite a bit in the coming days. Our suspicion in Fed Chair Powell will stick to the data like he usually does, but even more so because we are in between Fed meetings. Recalling Powell’s past comments, there could be some pain on the road to getting inflation back down toward the Fed’s 2% target, and it’s more likely than not his comments tomorrow will skew incrementally hawkish given the data.

We’ve already seen other Fed officials deliver more hawkish comments, including Atlanta Fed President Raphael Bostic saying on March 24 that he sees just one interest rate cut this year. And that was before the March ISM data, and the larger-than-expected Trump reciprocal tariffs.

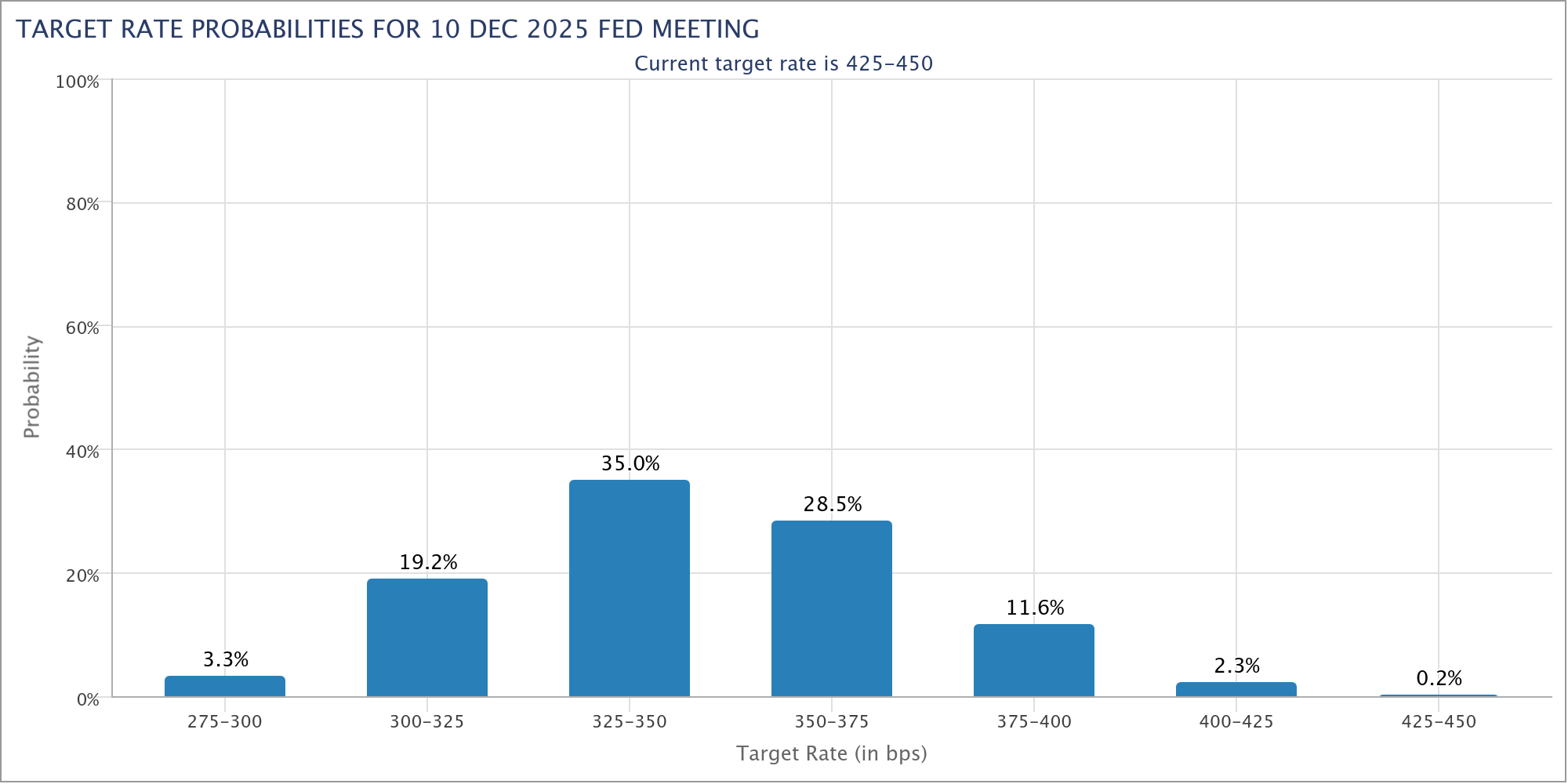

Where we’re going with this is the market is once again expecting the Fed to deliver multiple interest rate cuts this year. Per the CME FedWatch Tool, those multiple rate cuts equate to four 25-basis points by the end of this year. While data over the next few months could reverse recent hawkish Fed comments to something more dovish, based on what has been received thus far there is room for Powell to disappoint the market tomorrow.

The removal of that proverbial punch bowl would only keep the market in a sour mood as we wait for more on potential responses to Trump’s reciprocal tariffs, brace for negative earnings pre-announcements, and the start of the March-quarter earnings season.

For now, we’ll continue to stay on the sidelines, preferring not to get head faked, but we will continue to watch for a spike in the Volatility Index (VIX) and a steep enough drop in market oscillators to warrant putting some cash to work like we did last August. So far, we’re not there yet, but as you know, things can change, hence our continued focus.