Whatever Powell Says Today, Tomorrow Is Likely More Important

Let's check the key line item in the Fed’s updated set of projections and what we're really watching for ... on Thursday.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

We are in a bit of a waiting game today until the Fed’s 2 p.m. ET policy decision, which is not expected to deliver a rate cut, but what the policy statement says -- and an updated set of economic projections -- will set the tone for Fed Chair Powell’s press conference that follows. When we last heard from the Fed Chair a few weeks ago, his comments helped soothe the market, as he indicated the economy remained on solid footing, even as he admitted inflation was not cooperating. Ultimately, Powell said the Fed will continue to digest incoming information and adjust policy accordingly, and absent any March facing data we suspect that will be the message he reiterates this afternoon.

Following yesterday’s economic data that showed a pick up in housing starts and manufacturing activity during February, the Atlanta Fed’s GDPNow was updated and now the rolling forecast pegs gross domestic product contracting during the current quarter at -1.8%. Better than the recent figure of -2.4%, but still in the red and that could prompt some questions to the Fed chair this afternoon about the vector and velocity of the economy. Powell may point to other models, like the New York Fed’s Nowcast model, which as of March 14, sees the economy growing at 2.69% for the current quarter.

To us, given Trump tariffs and reciprocal measures so far, we will be interested in what the Flash March PMI has to say about the manufacturing and services economies, inflation, and job creation. That report will be published on Monday, March 24.

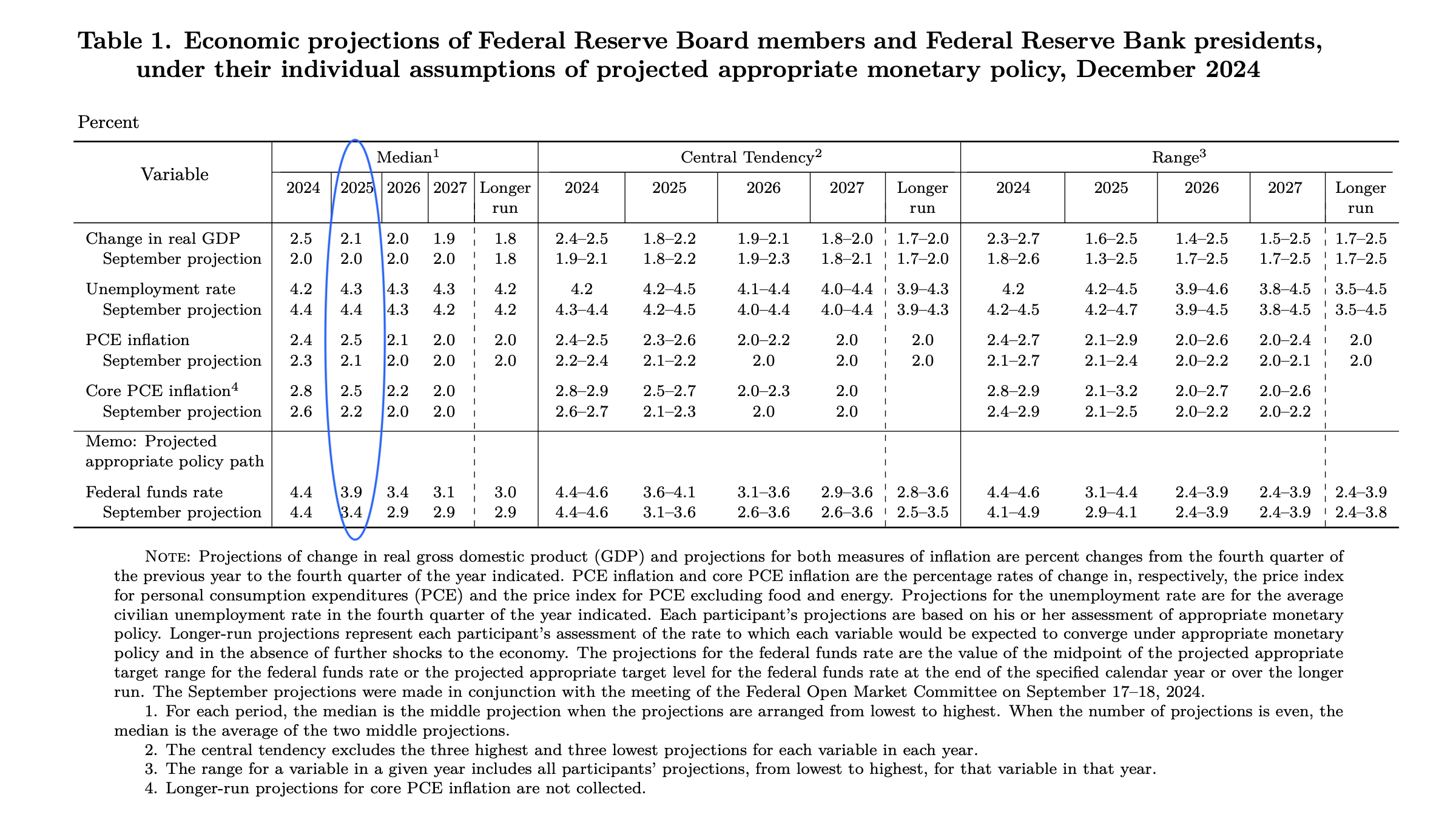

Fed’s Updated Economic Projections

When we examine the Fed’s updated set of projections that will accompany its policy statement, the figures we will be examining will be those for GDP, the unemployment rate, and the Fed funds rate. While we will need to take all three in concert, odds are the number of rate cuts implied by the Fed’s Federal funds rate projection will be the one the market focuses on the most.

As we can see in the table above, with its December 2024 set of projections the Fed telegraphed a total rate cut of 50-basis points for this year. But, as we’ve discussed numerous times, inflation data since the start of the year, but even more so since the start of Trump’s leaning into tariffs, has been sticky -- moving in the wrong direction. While the data is just for the first two months of 2025, given the recent start of tariffs and the likelihood for more come in April, absent a collapse in the economy, it’s harder to see the Fed delivering multiple rate cuts this year.

Where we’re going with this is if the Fed’s updated set of projections shows fewer than two rate cuts, that will disappoint a market that sees two to three rate cuts in 2025 per the CME FedWatch Tool. If the Fed stands pat and Powell leans into the Fed continuing to be data-dependent, we could see the market move higher in another sigh of relief move.

As we discussed in Friday’s Weekly Roundup, however, we have our concerns with June-ending quarter guidance as companies report their March quarter. For us, that means what we hear from FedEx FDX, Micron MU, Nike NKE, Darden DRI, and others tomorrow will be as important as what Powell shares this afternoon.

For the Portfolio that means, at a minimum, we will likely be on the sidelines today and tomorrow. As we digest those earnings reports and what they suggest lies ahead for June quarter guidance from more companies, we’ll plot our next move.

At the time of publication, the Pro Portfolio had no position in any security mentioned.