What the Softer-Than-Expected May CPI Means for the Market and Economy

Here's what we’re likely seeing in the data. Meanwhile, Trump’s 55% China import tariff figure isn’t an inflation panacea.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

If you missed our reaction to the lower-than-expected May CPI figures on the Schwab Network this morning, we too were surprised by the lower-than-expected figures published by the Bureau of Labor Statistics.

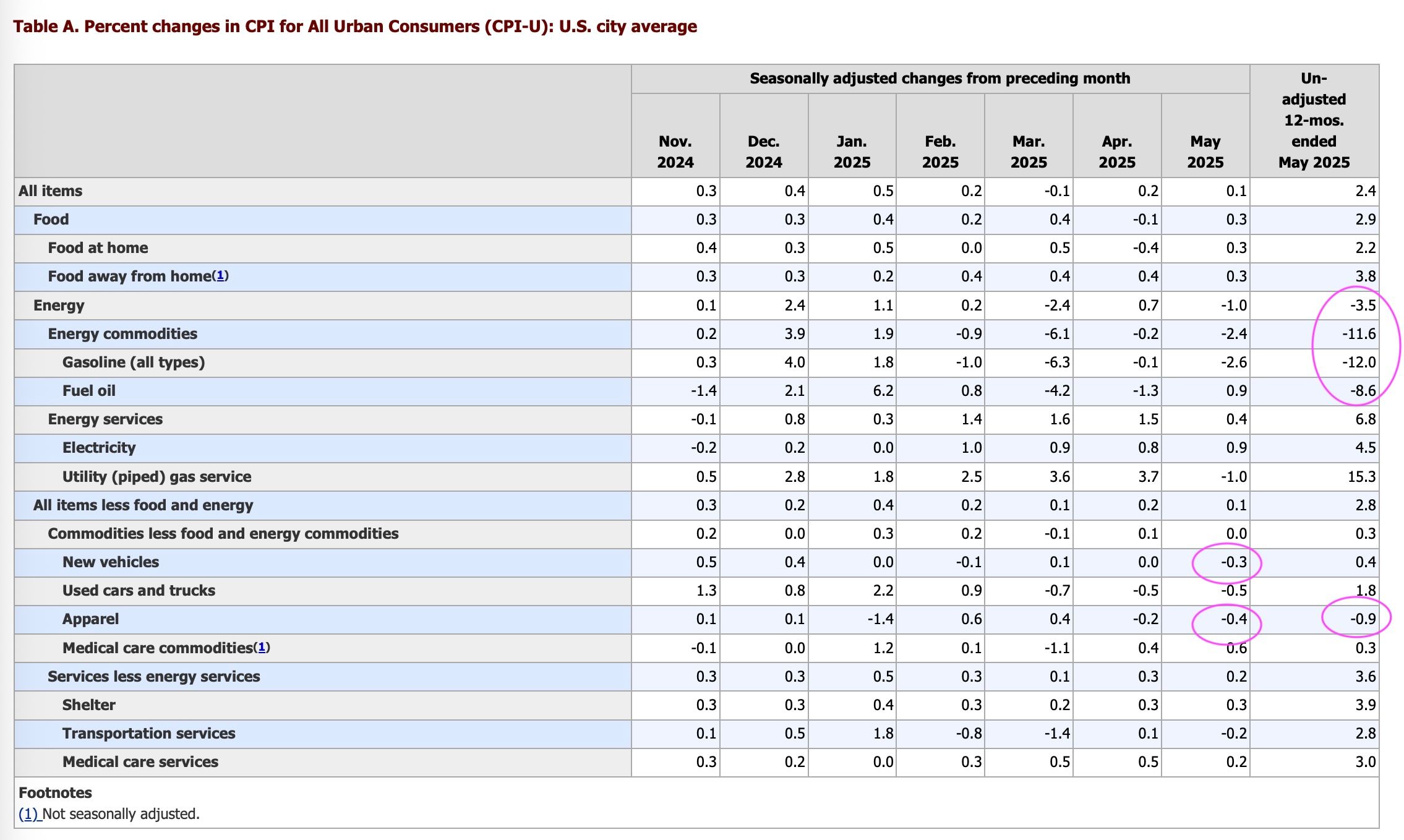

Instead of seeing sequential increases on a month-over-month basis for both headline and core CPI, the published figures showed not only sequential declines, but increases of just 0.1% for both headline and core. The year-over-year figures were also lower than the market expected, with May core CPI at 2.8%, unchanged compared to April, while the headline figure ticked up to 2.4% from 2.3% in April, but less than the 2.5% expected by the market.

To say those cooler figures were not expected by the market, would be an understatement. As we discussed in Monday’s video, falling energy prices were a contributor, but we also saw declines in new car and apparel prices, which is counter-intuitive given implemented tariffs. What we’re likely seeing in the data is a combination of companies chewing through existing inventories, and some retailers leaning into promotions and discounting to drive comp sales. Walmart WMT, e.l.f. Beauty ELF, Best Buy BBY, Ford F, Procter & Gamble PG, Macy’s M, and Mattel MAT have either recently enacted tariff-related price hikes or plan to do so.

In keeping with our comments this morning, the longer we go without trade deals and their agreed-upon and final details, the more likely we will see a more pronounced impact of existing tariffs in the data, on the economy and earnings.

That’s what JPMorgan JPM CEO Jamie Dimon was getting at in the comments we shared with you this morning. So, while the market’s initial reaction to the May CPI report was a positive one, as folks think it through with a critical eye, the more likely they will weigh the June CPI data.

On the subject of pending trade deals, yes, President Trump posted on social media that a U.S. trade "deal with China is done" but the president went on to acknowledge that both he and Chinese President Xi Jinping had yet to formally sign off on the agreement. Trump went on to say that the deal would see China maintain its current 10% tariffs on goods imported from the U.S., while the U.S. would keep 55% tariffs on Chinese imports.

Per data from the Peterson Institute for International Economics, the average effective tariff rate on Chinese goods was 20.8% in January 2025. If Trump’s 55% figure holds, that would mean incrementally higher costs in the next few quarters, keeping concerns for inflation and margin pressure alive.

Now we'll watch the Trump and Xi trade deal approval process and see if there are any other late-in-the-game negotiation attempts. We would not be surprised to see Xi make a move to reduce that 55% figure. Near-term will continue to tread carefully with the Pro Portfolio, especially since any last-minute U.S.-China or even U.S.-EU trade deal saber-rattling could unsettle the market.

More Pro Portfolio:

- We're Initiating a Position in This CoreWeave, OpenAI, ServiceTitan Play

- Weekly Roundup: Widening Our Lead and Adding a New Position

- Chocolate Inflation, a Tear in My Non-Alcoholic Beer, AI Everywhere and More News for Investing

At the time of publication, TheStreet Pro Portfolio had no positions in any securities mentioned.