What Might Move Our Google Rating as Shares Dip on Mixed Results

We're sticking with our price target but here’s our thinking about our rating.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

In our preview comments on Tuesday, we shared the run-up in Alphabet’s GOOGL shares set a high bar for the company’s December quarter earnings report.

On Tuesday night, the company delivered mixed results with EPS that rose 31% year over year to $2.15, which was better than the $2.13 consensus, but revenue for the period of $96.47 billion came up a wee bit shy of the expected $96.68 billion.

Alphabet also outlined a far larger capital spending plan for this year of $75 billion, well ahead of the near $60 billion expected and the $52.5 billion spent in 2024. The bulk of that more-than-40% increase is targeted for “technical infrastructure,” including servers and data centers as the company continues to invest in AI and cloud. This makes that another positive data point for our shares of Nvidia NVDA and Marvell MRVL.

That combination along with a modest miss on cloud revenue for the quarter is weighing on GOOGL shares this morning. Reading between the December quarter Cloud revenue and the company’s capital spending outlook, the likely scenario is that, like Microsoft MSFT, Google Cloud is capacity-constrained. Both companies, and others most likely including Meta META and Amazon AMZN, are investing to capture the expected rise in AI spending. A new report from consulting firm McKinsey finds that over the next three years, 92% of companies plan to increase their AI investments. However, only 1% of leaders call their companies “mature” on the deployment spectrum, meaning that AI is fully integrated into workflows and drives substantial business outcomes.

There were several positives found in Alphabet’s results. Probably the biggest was the continued climb in the company’s operating margin, which hit 32% up from 27% in the year-ago quarter. That jump reflects continued gains at Google Services and Google Cloud in the face of ongoing AI and cloud investments to drive future revenue. Absent the losses from Alphabet’s other bets, the combined operating margin of Google Services and Google Cloud were over 36% in the December quarter, up 400 basis points year over year. Similar to our comment for Meta, that improvement reflects a combination of disciplined investing and a good mix of productivity and cost reduction efforts that should drive further margin gains as the investment phase ramps down several quarters from now. Third, despite the modest shortfall in cloud revenue for the quarter, YouTube and cloud revenues combined ended the year at a $110 billion annual run rate.

While the market reaction we are seeing in GOOGL shares is a setback for the Portfolio, rising AI adoption and the continued shift to digital advertising means we will remain owners of GOOGL shares.

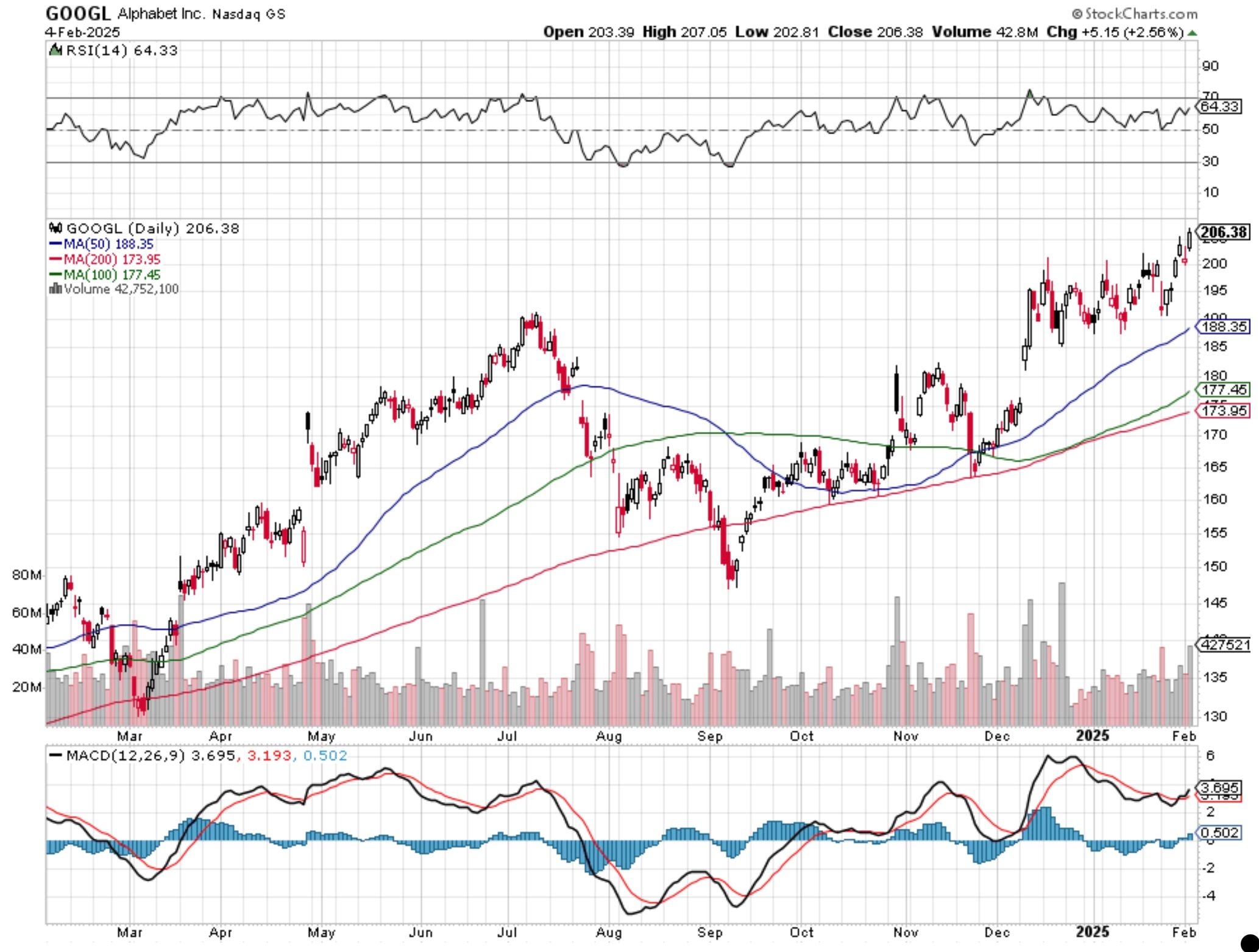

While others are trimming price targets to $210 to $230 from higher levels, we are maintaining our $210 target for GOOGL shares. Rather than whip our GOOGL rating around, we’ll look to see where the shares settle out as the market digests the details and other learnings from Tuesday night’s earnings call. In recent weeks, we’ve seen shares of companies that have just missed expectations plummet to the low double-digits. If we see that with GOOGL shares, that would bring them to levels that could close the December gap seen in the stock chart, but it would also bring strong support for the shares between the 100- and 200-day moving averages. That would offer enough upside to maintain our current One rating.

However, if we see a more modest pullback in GOOGL shares, one that only offers less than 10% upside to our $210 target, we would be inclined to lower our rating to a Two from One. Helping limit the potential downside in the shares, after repurchasing $15 billion in stock during the December quarter, the company has roughly $45 billion left under its current program.

As Alphabet shifts from investment to harvest mode, we’ll revisit our price target as needed.

Related Thoughts: Marvell and Trade Desk

During its earnings call, Alphabet shared that it saw strong uptake of its proprietary Trillium AI chipset, another positive data point for Marvell. When Amazon reports Thursday night we’ll be looking for similar comments about its latest Tranium chipset.

In discussing its YouTube segment results, management noted YouTube’s advertising revenue rose 14% in the quarter driven by strong spend on U.S. election advertising as well as brand and direct response advertising. That along with the continued adoption of advertising models on streaming platforms argues for a solid December quarter earnings report from Trade Desk TTD when it reports on February 12. We do expect to see Trade Desk’s outlook for 2025 reflect the fade in political advertising, but Trade Desk remains well positioned for the ongoing shift to digital advertising, especially for video and connected TV.

More Pro Portfolio

- We're Adding Back These Two ETFs to the Portfolio Amid Uncertainty

- Monthly Roundup: Starting 2025 Off Strong as Potential Tariffs Add Uncertainty

- Charting the Markets: S&P 500 Looks to Be Running Out of Steam

At the time of publication, TheStreet Pro Portfolio was long GOOGL, NVDA, MRVL, MSFT, META, AMZN and TTD