What Does the August Services PMI Tell Us?

Meanwhile, ADP’s August Employment Report misses expectations.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Following up on my appearance on the Schwab Network this morning, in which I discussed the expectation-missing August Employment Report from ADP, let’s dig into the August Services PMI numbers. And with inflation at lofty levels, we discuss why Friday’s August Employment Report may only be one more piece in the rate cut puzzle.

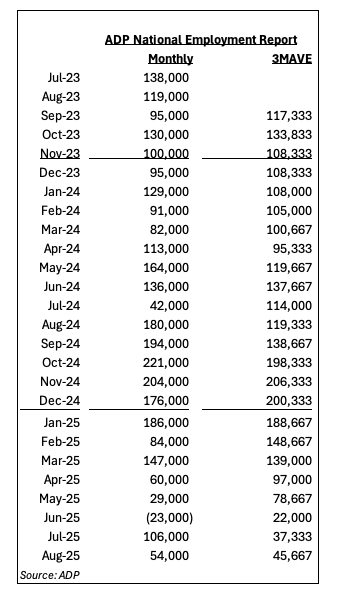

First ADP’s August Employment Report.

ADP’s August Employment Report

ADP found 54,000 jobs were added during August, below the 65,000 that were expected and dramatically slower than the revised 106,000 created in July. Looking back over the last few months, we can see marked volatility in the monthly figures, which is why we’ve examined the data through a three-month moving average.

As you can see below, it shows a dramatic slowdown in job creation in June of this year (22,000 jobs), followed by more restrained growth than we’ve seen in some time. If you’re thinking that lines up with the impact of tariffs, we’re not one to disagree all that strongly.

When we look at the three-month trailing figures, we remember words from Fed Chair Powell about how there may need to be some pain to return inflation to the Fed’s 2% target.

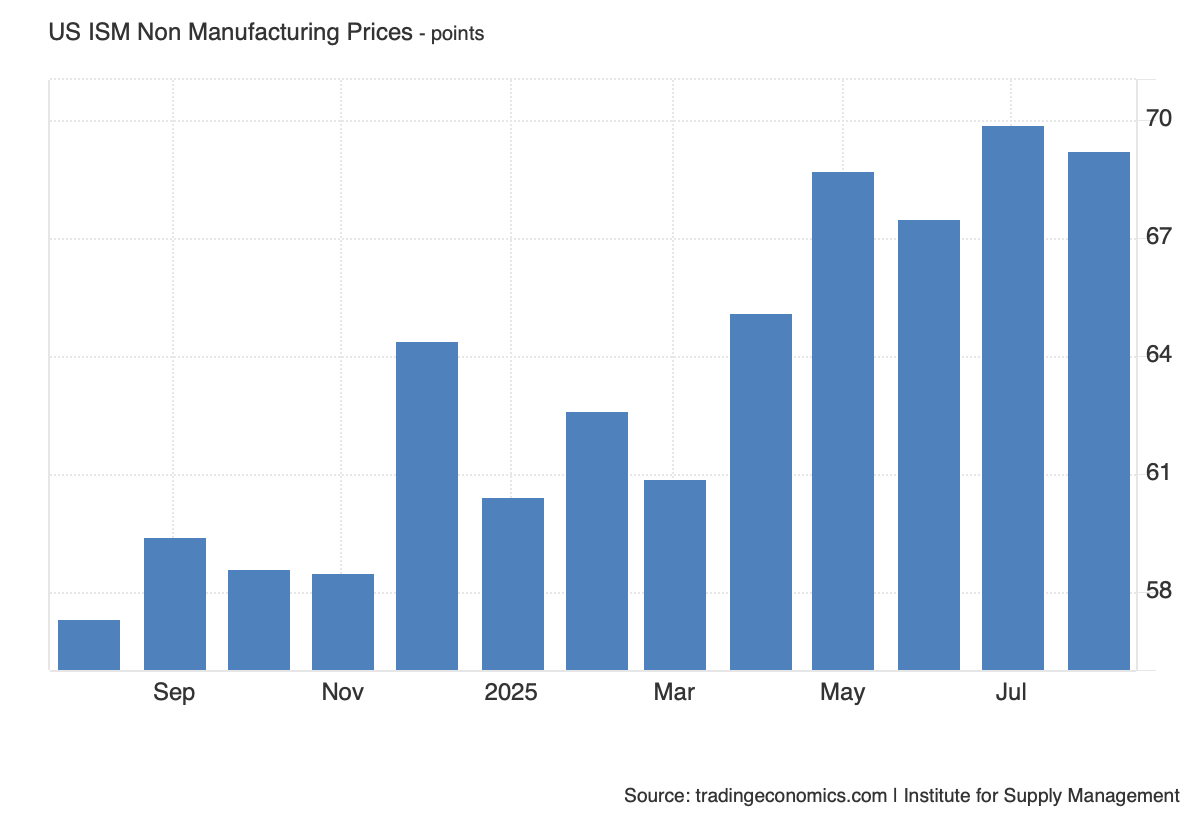

Services Sector Inflation Remains at Lofty Levels

That brings us to today’s back-to-back August Services PMI reports from ISM and S&P, which shows inflation pressures continued to rise in August.

S&P Global found:

Service providers noted that payroll expenses helped to push up their overall operating costs in August. Tariffs were also frequently mentioned as a driver of inflation, with suppliers reported to be raising their charges accordingly. Latest data showed an ongoing pass-through of these higher operating expenses to clients via an increase in selling prices. Although down a little since July, output price inflation remained elevated and amongst the steepest recorded by the survey in the past three years.

In the chart below, we see that while ISM’s Price sub-index for its August Services PMI declined sequentially, it remained at rather lofty levels compared to earlier this year.

What Does It Mean?

Trading volumes so far Thursday are once again below average, like they have been the last few days, even though the probability for a September rate cut has climbed to more than 95% vs. just under 87% a week ago. That seems to be a bit of a disconnect to us, and we interpret it to mean that despite today’s ADP data, the market is still unsure about either a September rate cut or multiple ones across the Fed’s September, October, and December policy meetings.

Some suspect Friday’s August Employment Report will be a defining moment for upcoming rate cuts. The report is expected to show 75,000 jobs created and the Unemployment Rate ticking up to 4.3%. However, September 10 and 11 bring us the August PPI and CPI data, and as of now, market forecasts for both show core inflation figures holding steady with year-over-year July figures of 3.7% and 3.1%, respectively.

Given the inflation comments found in the collected August PMI reports, barring a substantially weaker-than-expected August Employment Report, we are likely to see the market’s attention shift to next week’s inflation data. For that reason, and because we continue to hear differing views from Fed heads about the number of rate cuts, we could very well see the potential for a September rate cut and multiple rate cuts between now and year-end come down to the wire.

All we can do is follow the data, and that’s what we intend to do.