We're Updating Our Table of Earnings Expectations and Potential Pick-Up Points

We plan to revisit the portfolio Bullpen as well as some current position ratings.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

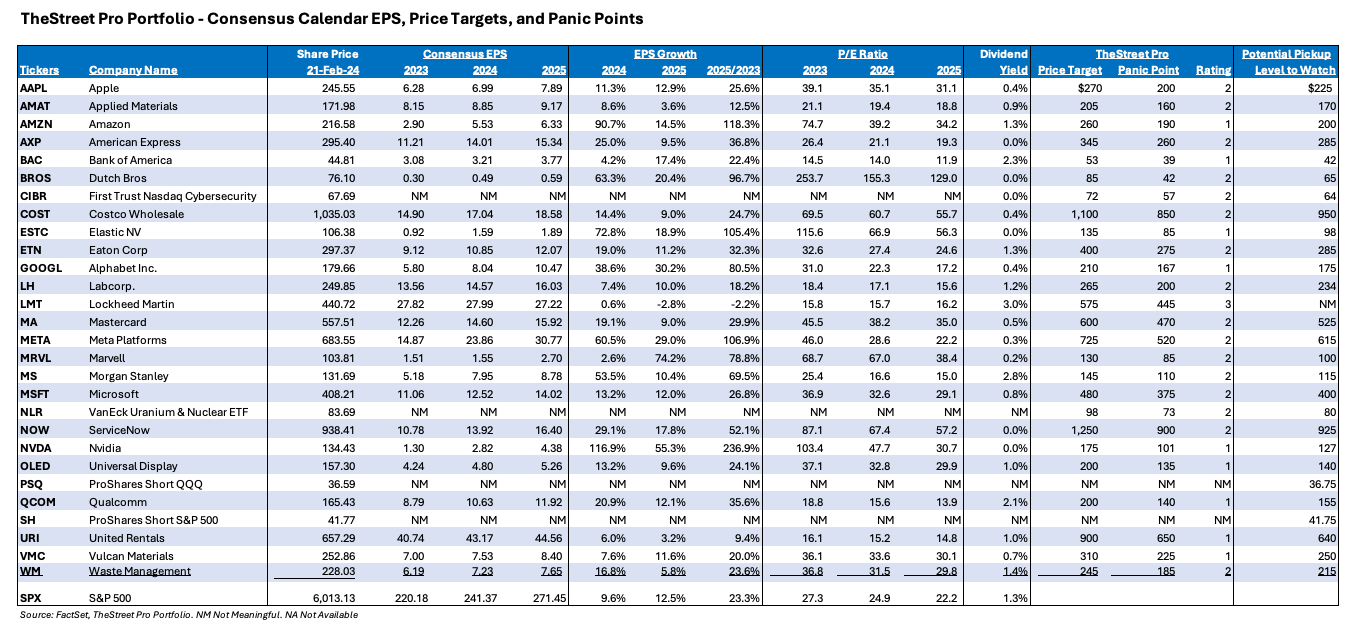

We are updating our table of consensus EPS growth expectations for TheStreet Pro Portfolio holdings, and following the market selloff over the last few days, our pick-up price levels for those positions. As we do this, we would remind you that, like our panic points, these are not hard lines but ones based on what we know as of today make for favorable entry point levels. As we saw last week, fresh data can alter expectations and that’s why we will continue to update this table on a more frequent basis in the coming weeks.

Setting the stage for you examining the table, consensus 2025 EPS expectations for the S&P 500 now call for a slower rate of growth this year compared to forecasted levels at the start of January. Several weeks, ago the market forecast was for that market basket to deliver EPS of $274.19 this year, and $311.44 in 2026. Crunching the numbers that’s 14.5% growth this year, and 13.5% next year. However, the latest figures, which do not reflect Walmart’s WMT softer-than-expected guidance, call for that growth to be more like 12.5% this year. Keep in mind, that even though these figures reflect 77% of the S&P 500 that reported through February 14, the mix of names to come, including retailers, could lead to another round or two of further growth expectations reductions.

This likely means our EPS growth hurdle for newer portfolio candidates will inch lower, but even so we will still focus on companies with superior growth prospects as they benefit from multi-year structural tailwinds.

With that in mind, we will use the time between now and potentially market-moving developments later this week and next to revamp the portfolio Bullpen. Alongside that, we will also revisit our ratings for some of the portfolio’s holdings. For example, comparing the potential upside to our price targets vs. incremental downside for a few holdings suggests current Two ratings need to be adjusted. Needless to say, more to come on both of these fronts.