We're Reiterating Our $200 Target for This Holding After Thesis-Confirming Results

Progress on the company’s diversification efforts is underway, with much more to come.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Alright, folks we are back in action after some interviews this morning

Now, let's get into last night’s earnings report from Qualcomm QCOM. In a upcoming Alerts we'll discuss results from Labcorp LH and Costco’s COST January sales report.

During yesterday’s Office Hours, we shared our initial reaction to Qualcomm’s report, which contained consensus-topping results for both the December quarter and the current one. By the numbers, Qualcomm delivered EPS of $3.41, $0.43 better than the $2.98 consensus, on revenue that rose 17.8%, year over year, to $11.7 billion, topping the $10.95 billion market forecast.

For the current quarter, the company guided its bottom line to EPS of $2.70-$2.90 on revenue of $10.3 billion-$11.2 billion compared to the market’s expectations for $2.69 and $10.3 billion. Breaking down that guidance, chip revenue is expected to be $8.9 billion- $9.5 billion, up 11%-18%, year over year, with gains across smartphones, IoT, and automotive. The balance of revenue will be from Qualcomm’s technology licensing business (QTL).

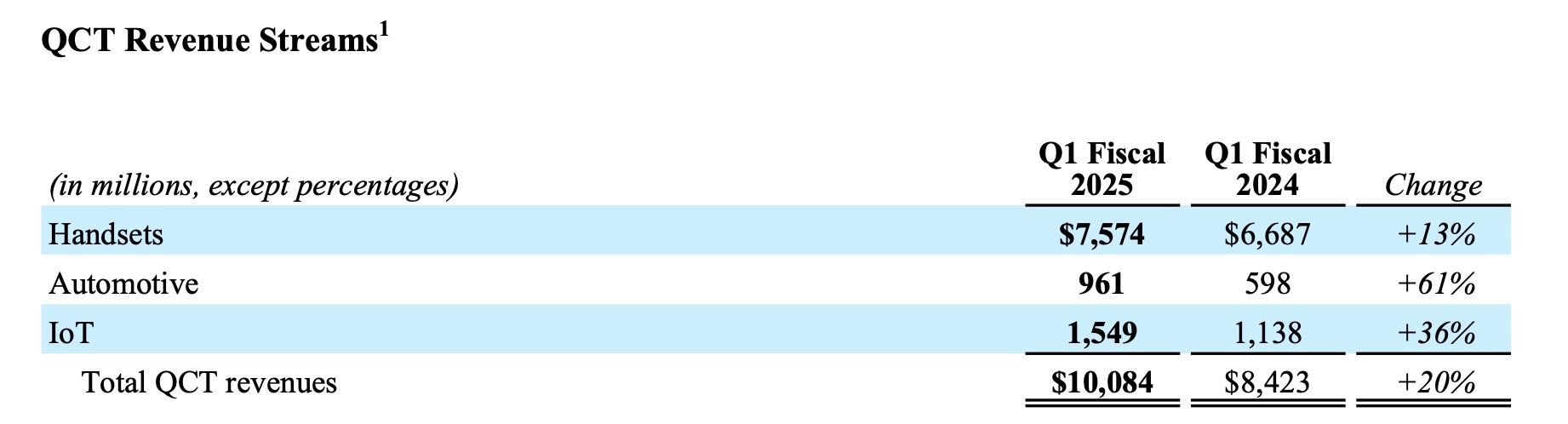

We like those figures, but digging into the company’s report we like what we see even more from its chip business, which it refers to as “QCT.” The segment benefited from record smartphone revenue, but more importantly, in our view, showed notable progress on Qualcomm’s efforts to diversify its revenue stream away from that end market. We see that in the table below from the company’s earnings report.

Granted, the Automotive and IoT business today are still relatively small compared to smartphone, but management reiterated its 2029 target of $22 billion in non-handset revenue. We should see continued progress toward that long-term goal in the coming quarters. Helping fuel that on the AI PC front, there are more than 80 designs in production or development, and management continues to target more than 100 designs to be commercialized through 2026 across leading PC OEMs such as Acer, ASUS, Dell, HP, and Lenovo. For the current quarter, Qualcomm sees its IoT revenue up 15% year over year and Automotive revenue up 50% as more platform wins matriculate, while smartphone revenue is slated to be up around 10%.

All in all, results and guidance were very confirming for our thesis on Qualcomm shares, and that leads us to reiterate our $200 price target. We continue to think that as Qualcomm delivers on its diversification strategy, Wall Street will revisit how it values the shares, and that is what we aim to capture by being long-term shareholders.

One addtional item we will call out is Qualcomm's renegotiation of its IP license with Huawei, and success on that front means upside for QTL revenues in the coming quarters.

So Why Were QCOM Shares Down This Morning?

In post-market trading last night and early this morning QCOM shares were trading off despite the wonderful results outlined above. We chalk that up to the extreme pressure put on the shares of Skyworks Solutions SWKS following its earnings miss and lowered guidance. The issue there is its largest customer, Apple AAPL, is moving from sole-sourcing on certain products with Skyworks to dual-sourcing with another vendor believed to be either Broadcom AVGO or Qorvo QRVO.

That extreme pressure was the weight on QCOM shares but it was a Skyworks-specific issue. We are starting to see some price target increases emerge, including to $195 from $180 from TD Cowen. We would not be surprised to see more as the day rolls on.

On a Side Note…

During its earnings call, Qualcomm said it is seeing a near doubling in the number of AI features in smartphones and it expects that trend to continue. That is in line with our thinking that AI smartphone adoption will be a driver of network congestion and foster incremental capital spending on carrier infrastructure. In other words, that reaffirms one of our thesis items for Marvell Technology MRVL shares and offers another positive data point heading into Marvell’s upcoming earnings report.

At the time of publication, TheStreet Pro Portoflio was long QCOM, AAPL and MRVL.