We're Downgrading This Name and Could Accelerate Exit Despite AI PC Growth

We will begin our winding down of this position, but guidance from a key sector name could accelerate our exit.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Research firm IDC said this week that preliminary fourth-quarter global PC sales grew 9.6% year over year, to 76.4 million units. That was up slightly compared to the 75.9 million units shipped in Q3 2025, reaching a total of 76.4 million units.

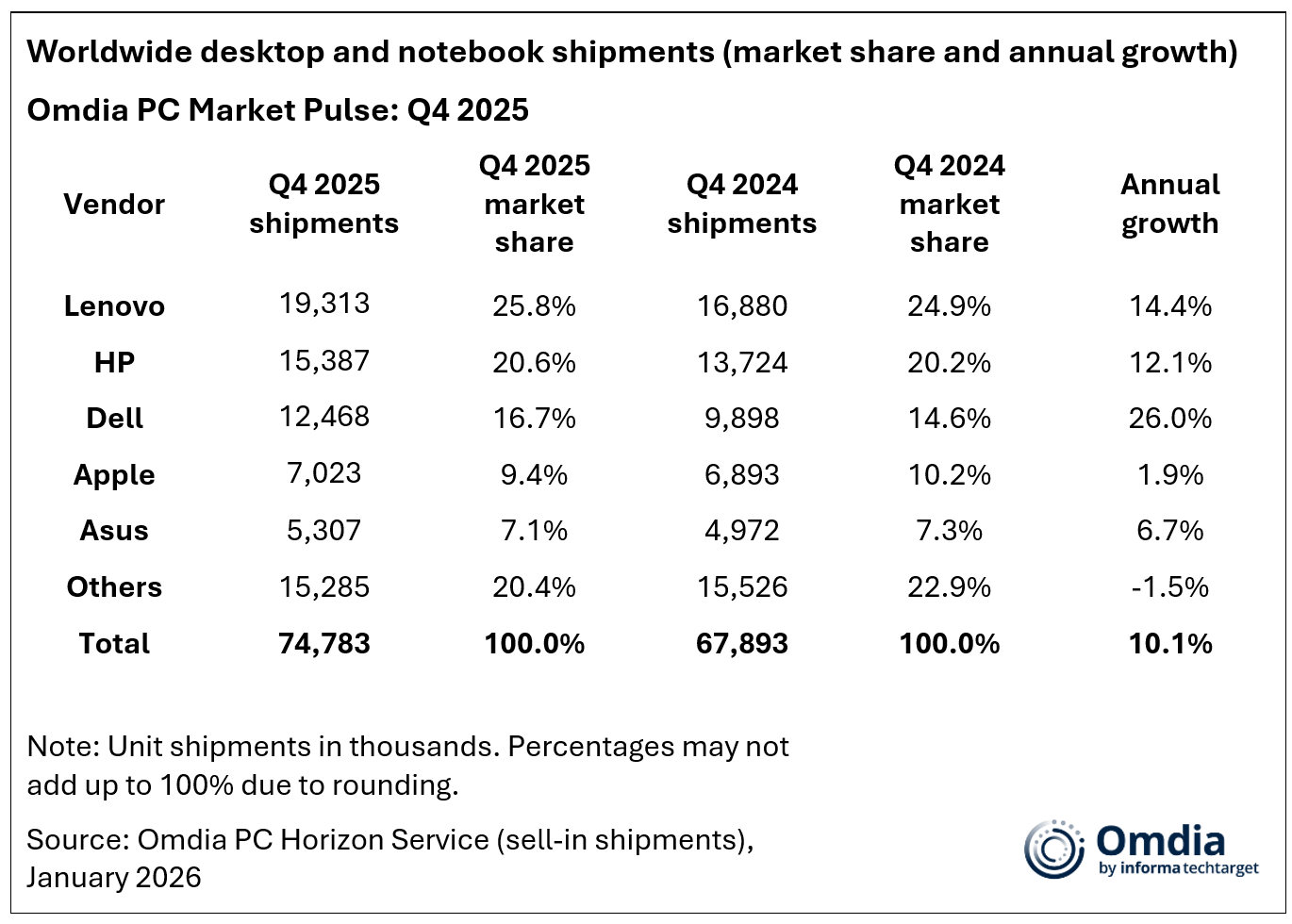

At almost the same time, another research firm, Omdia, shared its finding that total shipments of desktops, notebooks and workstations in Q4 2025 grew 10.1% to 75 million units. This brought full-year 2025 PC shipments to 279.5 million units, a 9.2% increase over 2024 volumes.

In the chart below, we can see the lineup of what we’ll call the usual suspects with HP (HPQ) , Dell (DELL) and Lenovo picking up market share during the quarter.

Those share gains are a positive for Qualcomm (QCOM) as its chips are being used by the likes of Lenovo, Dell and HP, and others, including Samsung, Acer and ASUS. This suggests we could see a somewhat stronger AI PC business for Qualcomm’s December quarter, which will be reported on February 4. On that date, we expect to hear Qualcomm discuss its expanding relationship with Alphabet (GOOGL) and Android for the smartphone market, but others as well.

However, we continue to see growing concerns about memory pricing and availability. That includes the following from Omdia:

"In December 2025, PC vendors began signaling their expectations of price increases. Coupled with the inability to secure sufficient supply, this has already dampened forecasted shipment expectations for 2026. 'Between Q1 to Q4 2025, mainstream PC memory and storage costs rose by 40% to 70%, resulting in cost increases being passed through to customers,' said Ben Yeh, Principal Analyst at Omdia. 'Given tight 2026 supply, the industry is emphasizing high-end SKUs and leaner mid to low-tier configurations to protect margins.'"

The wind-up, as we discussed last week, is that memory manufacturers are prioritizing high-margin server DRAM and HBM for data centers, and that mix shift in production has come at the expense of memory for PCs and smartphones.

With growing signs Qualcomm’s guidance could come up short relative to market expectations, we are downgrading the shares to a Four rating. We will begin to work on exiting the position in the very near term, and subject to the guidance from Taiwan Semiconductor (TSM) later this week, we may accelerate that exit.

More Pro Portfolio

- We're Locking in Big Gains on This Holding Reflecting Portfolio Discipline

- Consumers Are Spent, France Hack, U.S. of Old and More Investing News

- Weekly Roundup: Portfolio Gains Ground Amid Key Data and News

At the time of publication, TheStreet Pro Portfolio was long QCOM and GOOGL.