We're Adding This Name to the Portfolio Bullpen as Consumers Get Selective

While still early, we’re laying the groundwork for later this year.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Consumers are becoming increasingly cost-conscious and selective in their spending, and this means they are more prone to trading down and shopping at off-price retailers as well as continuing to frequent Costco COST and Amazon AMZN. We’ve seen this before during periods of economic uncertainty and given the findings of recent consumer inflation expectations data and retailer guidance, it looks like that is where we are heading.

That’s the backdrop for the move we're making today.

We are adding off-price retailer TJX Companies TJX, the company behind TJ Maxx, Marshalls, and Home Goods, to TheStreet Pro Portfolio Bullpen. The shares have fallen hard over the last few weeks following the company's downside guidance for its April 2025 quarter and for its current fiscal year, which ends in January 2026.

Baking into that guidance is same-store sales comps of 2%-3% for both periods compared to 5% posted in the January 2025 quarter. Alongside that guidance, TJX also upped its quarterly dividend to $0.425 per share and plans to buy back $2.0 billion-$2.5 billion between February 2025 and January 2026. TJX hasn’t formally announced that dividend increase, but when it does it will continue the upward trajectory in its dividend over the last 20 years.

Retail Landscape

In our February Retail Sales comments, we pointed out how two more retailers, Canada’s Hudson Bay and Forever 21, are both succumbing to hard times. Hudson is moving into liquidation while Forever 21 is once again declaring bankruptcy. Both likely mean the selling of assets and inventory, usually at steeply discounted prices and this plays right into TJX’s stated strategy of being an opportunistic buyer. At the same time, other retailers were holding higher year-over-year inventory levels closing out the holiday shopping season as they face a more choosey consumer while having to make room for the spring season. This suggests a potentially more fertile environment for TJX’s buying associates and a better selection for its shoppers.

Picking Our Spots

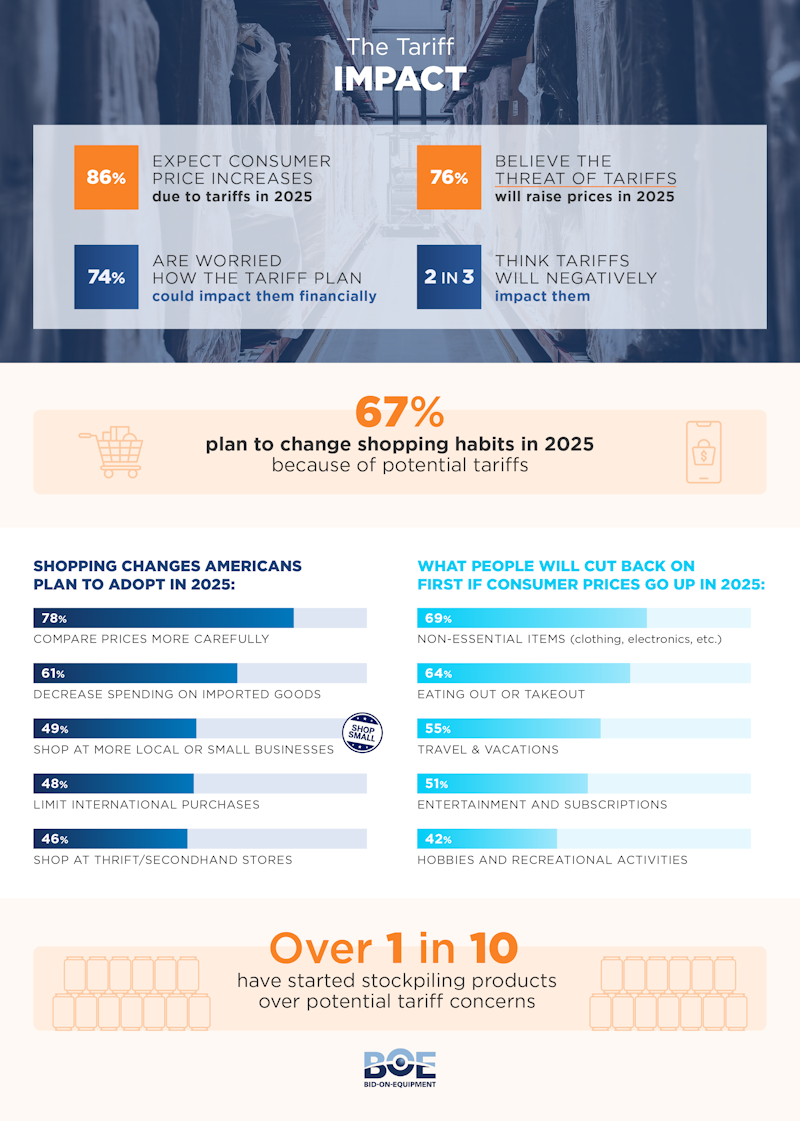

While we like TJX's positioning, as we discussed in Friday’s Weekly Roundup, headwinds remain, including additional tariffs that could pressure consumer sentiment even more so. Meanwhile, the pop in layoffs detected by the February Challenger Job Cuts report and subsequent layoff announcements suggest further belt-tightening is ahead.

As we shared in today’s video, we will need to pick our spots and that’s why we are only adding TJX shares to the Bullpen for now.

We suspect we’re likely to get some questions as to why TJX, instead of Ross Stores ROST. It boils down to the following.

First, TJX is the largest off-price retailer in the U.S. Second, its merchandise array is larger. Third, EPS growth prospects at TJX are greater than those for Ross, and fourth, TJX offers digital shopping.

At the time of publication, TheStreet Pro Portfolio was long COST and AMZN.