We're Adding a Semi-Cap Play to the Portfolio Bullpen

Ramping chip demand and tight industry capacity levels is a nice pain point.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

3-19-26-AMAT-shutterstock_723035209

3-19-26-AMAT-shutterstock_723035209

While the market’s resetting of expectations continues, let’s put together a few pieces of data and add some perspective around recent comments from Nvidia (NVDA) CEO Jensen Huang.

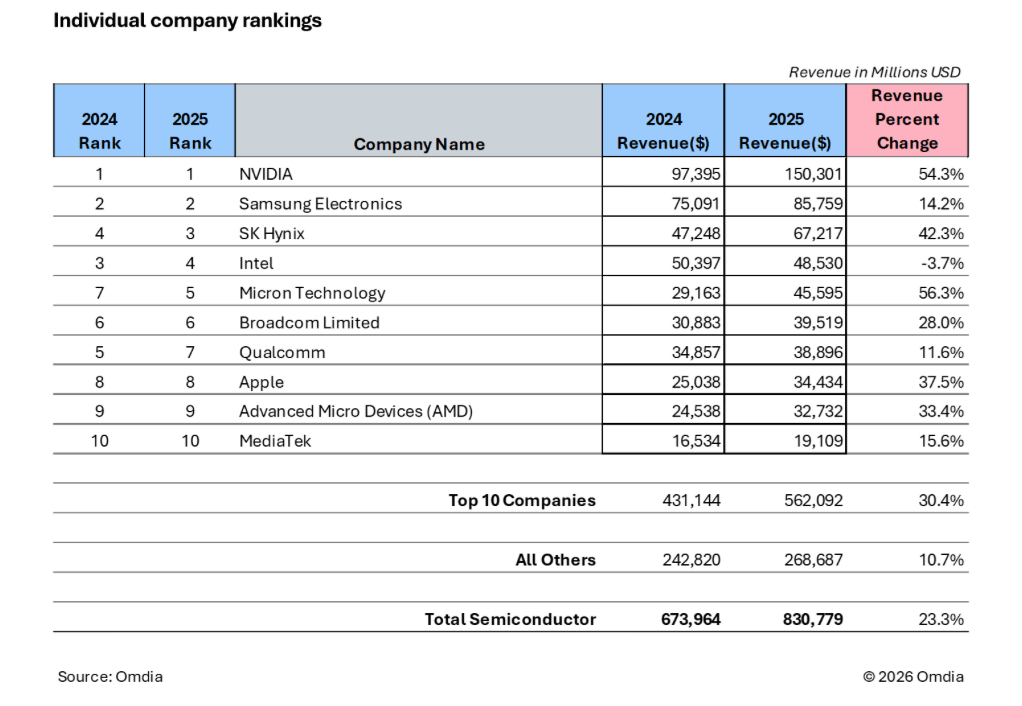

Per the Semiconductor Industry Association (SIA), global semiconductor industry sales hit a record $791.7 billion in 2025, up a staggering 25.6% compared to the year before. Another research firm, Omdia, pegs 2025 industry chip sales around $830 billion, up more than 20% year over year.

Note: It appears Omdia is using calendar figures, which means some adjustments were made for companies that do not report quarterly results on that timeline.

Leading that surge, as you’re likely to guess, was AI and higher performance computing (data center) demand. Omdia sees that figure topping $1 trillion this year as does SIA, and based on their respective tallies for 2025, implies year-over-year growth of 20%-25%. Per SIA’s findings that $82.5 billion was sold in January 2026, more than 46% higher than in January 2025, we see the potential for those industry forecasts to be conservative.

On Monday, Jensen Huang shared that he sees $1 trillion in demand for Nvidia’s Blackwell and Rubin chips alone between this year and next.

Wednesday, reports indicated Nvidia won Beijing's approval to sell its H200 AI chips to China, which previously accounted for around 13% of its total revenue. Nvidia is also preparing a version of the Groq AI chip that can be sold to the Chinese market.

In recent weeks, Broadcom’s (AVGO) Hock Tan said he sees the company benefiting from accelerating custom AI chip demand to $10.7 billion in the current quarter, up 140% year over year. Tan also noted he has a “line of sight” to that business to be more than $100 billion in 2027. And let’s remember that Broadcom also offers chips for other applications, including networking, servers, and storage, that are also benefiting from the AI and data center buildout.

On its recent earnings call, Marvell (MRVL) telegraphed that its year-over-year revenue growth will accelerate each quarter in the coming year, given many of those same factors. For the current fiscal year, Marvell sees its revenue clocking in near $11 billion and, as we discussed in assessing its recent quarterly results, $15 billion next year.

The gist of the comments from those companies and even from Micron (MU) last night is that demand outstrips supply in a meaningful way. Factor in consensus revenue estimates for the others on Omdia’s list above, and industry capacity is poised to remain tight in the coming quarters. If we layer on forecasted AI and data-center spending forecasts and consider the accelerating adoption of AI we are seeing, odds are that capacity is going to remain tight, but need to be addressed.

One That Got Away

That brings us to the outlook for semiconductor capital equipment, an industry that delivered ~$133 billion in 2025. SIA sees it rising to $145 billion this year and $156 billion in 2027, and others expect a continued step function higher through 2030. Underpinning that forecast is continued spending on AI and data centers, and corresponding equipment, as well as other connected devices, including appliances as well as cars and trucks.

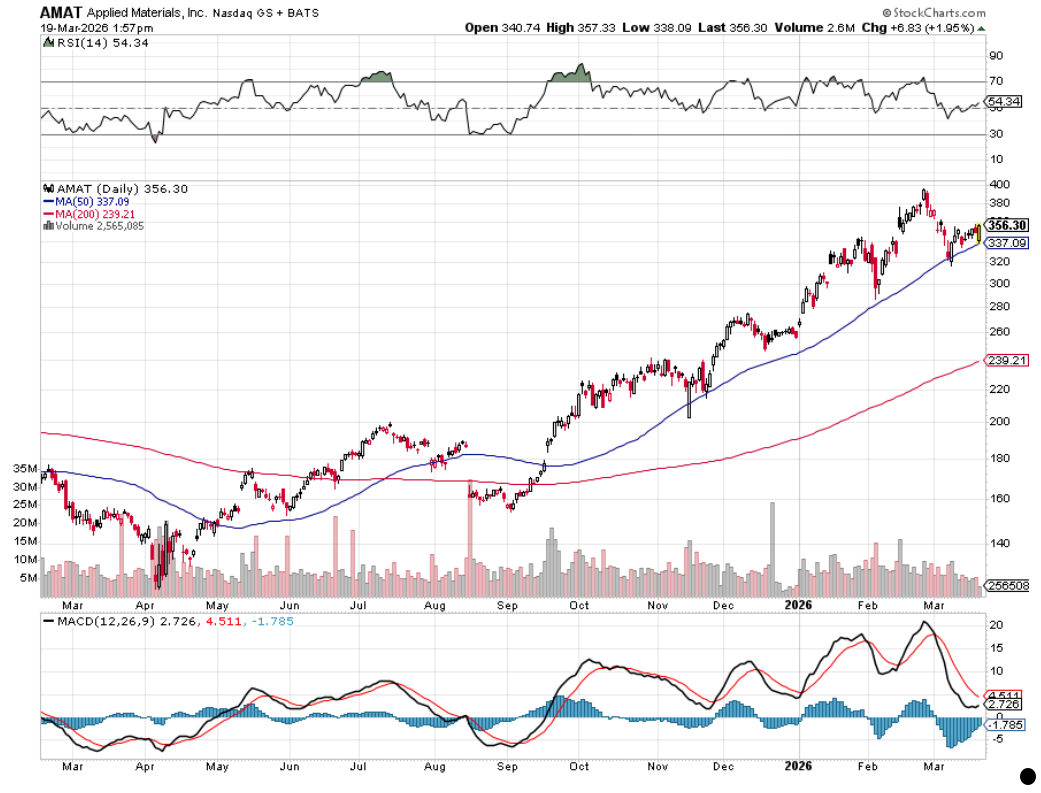

That backdrop, the recent market pullback, and following where capital is being spent have us bringing shares of Applied Materials (AMAT) into the Pro Portfolio Bullpen. Candidly, if there was one former position we shouldn’t have let go, AMAT is it. The learnings from that will be with us for some time, but it can also be paralyzing to play those "coulda, shoulda" games, as they can lead to miss opportunities. The recent pullback in AMAT looks like it could be one of them.

The consensus Wall Street price target for AMAT, depending on the source, is $410 to $425, which implies a P/E around 30x expected fiscal 2027 EPS near $13.85. That’s in line with where the shares peaked on a P/E basis back in 2024, when the company delivered EPS growth of just 7%. Based on the outlook for semi-cap equipment spending this year and next, that growth rate is expected to be more like 17% this year and 25% next year.

We’d also note Applied recently announced another 15% increase to its quarterly dividend, which brings it to $0.53 per share per quarter. In our view, that increase on top of the ones in the last few years speaks to the company’s longer-term demand outlook.

Given our concerns with the overall market, we will watch this one closely in the coming days. And we’ll note the shares appear to have once again bounced off the 50-day moving average , while what we see with its MACD is very constructive.

Related: Wall Street Turns on India as Oil Shock Drives 'Unprecedented Crisis'

At the time of publication, TheStreet Por Portfolio was long NVDA, AVGO and MRVL.