Weekly Roundup: Widening Our Lead... But Storm Clouds Are Brewing

Caution is warranted following the market’s surge to new highs and a deepening overbought condition. Here's our navigation plan.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

To say the last five days were strong for the stock market is something of an understatement, as the S&P 500 and the Nasdaq Composite both soared to fresh record highs. Those moves, recently culminating in double-digit gains for both market indexes off their late-March, early April lows, were fueled by de-escalation between the U.S. and Iran, and Israel and Iran. Ceasefires are fueling hope that more lasting peace deals will emerge, and developments over the last several weeks, from higher energy and petrochemical prices and fuel costs, will begin to fade.

Despite overbought conditions for both the S&P 500 and Nasdaq Composite that initially developed and deepened as the week went on, there is, arguably, a wee bit of hopium in the air when it comes to how quickly those headwinds could fade. The market’s reaction to quarterly results this week, which were impacted by first-quarter 2026 winter weather, tariffs, and the Iran War reinforce that thinking. To that, we can add the market’s reaction to corporate guidance that was not raised but reiterated from earlier this year, or fell short of consensus expectations.

We discussed this in our analysis of Netflix’s (NFLX) Q1 2026 earnings report, noting that because of the market’s rally and overbought condition, for individual stocks to push sustainably higher from current levels, companies will need to deliver beat-and-raise quarterly results that best Wall Street’s whisper numbers. With first-half 2026 consensus EPS figures for the S&P 500 having moved higher in March and April despite the war and other factors, and now the market’s overbought condition, the bar to clear is that much higher.

There are sectors of the market, many of which the Pro Portfolio is investing in, that are poised to deliver strong quarterly results and favorable guidance. However, from time to time overexuberance creeps into the market, raising questions about even stellar results and guidance. We’re mindful that even great numbers may not be enough to satisfy the current market mood, and less-than-expected ones could punish a company’s shares.

With that in mind, while the market strength propelled the Portfolio ahead of the S&P 500 on a year-to-date basis this week, we closed out the week by taking some disciplined action. On Friday we prudently and profitably trimmed a few positions that catapulted higher over the last several trading sessions and were in a deeply overbought condition. Should the market continue to power higher, more of that prudent action may be called for, but outside of one or two exceptions, the overbought nature of the market likely means we’re not going to put much capital to work near-term.

As we discuss below in The Week Ahead, weekend developments between the U.S. and Iran will be on our watch list, for they will likely shape how next week begins. And that means you’ll want to read our opening comments on Monday.

Enjoy your weekend and Saturday's Signals Alert. See you back here, bright and early Monday.

Catching Up on the Portfolio This Week

The Pro Portfolio made great strides this week, benefiting from double-digit gains in shares of Arista Networks (ANET) , Axon Enterprise (AXON) , Microsoft (MSFT) , Palantir (PLTR) , and SuRo Capital (SSSS) . Other outperformers this week relative to the S&P 500 included Broadcom (AVGO) , American Express (AXP) , Alphabet (GOOGL) , Meta (META) , Marvell (MRVL) , Morgan Stanley (MS) , and Nvidia (NVDA) . Those gains outweighed the late-week fall in Netflix (NFLX) shares as well as the market's resulting drag on our inverse market ETF positions.

Looking at the EPS Diplomats basket, the tremendous moves in Credo Technology (CRDO) , Bloom Energy (BE) , Rocket Companies (RKT) , Micron (MU) , and Hudbay Minerals (HBM) , expanded its lead over the S&P 500 as well.

On an aggregate basis, the Portfolio widened its lead over the S&P 500 on a year-to-date basis. That is a welcome development, of curse, but let’s remember it is but a snapshot in time, and we must remain vigilant, follow the data, and take advantage of opportunities if and when they present themselves. Rest assured, we’ll keep our eyes on the ball.

On Monday, we picked up more shares of Palantir (PLTR) near $130, and the following day, added further to our position at Axon (AXON) , buying that slug of shares near $378. On Friday, we used the continued market melt-up that deepened its overbought condition to prudently ring the register on shares of Amazon (AMZN) , Arista Networks (ANET) , Broadcom (AVGO) , and Marvell (MRVL) . Relative strength index levels for each of those positions flashed a deeply overbought condition following their outsized moves to the upside quarter to date.

As we made those very profitable trim trades, we also downgraded our ratings on AMZN, ANET, and AVGO shares to Twos from Ones, where they joined MRVL. We also noted that we are keeping a close eye on a few other positions that are approaching an overbought condition, and that if we see the market rally continue, we may be inclined to make a similar move with them.

The net combination of those moves lifted the Portfolio’s cash position ahead of the Q1 2026 earnings season, which kicks up a few more notches next week and the week after. Next week, more than 90 S&P 500 companies will be reporting, including seven Dow 30 components. In our comments throughout the week, and early Friday morning, we reviewed company commentary about Q1 2026 headwinds, including winter weather, tariffs, higher energy costs, and other impacts from the U.S.-Iran conflict.

Odds are we’re likely to hear more about that next week, and that has the potential, especially with the market’s elevated RSI levels, to throw some cold water on the market’s impressive rally. With that in mind, even though our market hedging, inverse ETF positions have restrained the Portfolio’s gains to some extent, we’ll stick to our plan and hold them as Q1 2026 earnings season moves beyond bank and financial stocks. As we navigate those results and how they influence the market, we’ll review their standing in the Portfolio.

With that in mind, following the late-in-the week pullback in Netflix post earnings, we discussed what we’re watching to pick up more shares of that streaming content company. We are going to patiently wait for an opportunity in a more balanced risk-to-reward market environment. If we see a bout of market softness near-term, NFLX shares have solid support near $92.

Now let’s see what others on Wall Street had to say about the Portfolio’s holdings during the week:

Monday: B. Rily increased its Marvell (MRVL) price target to $156 from $135 and took its Applied Materials (AMAT) target to $485 from $450. Citigroup lifted its Eaton (ETN) price target to $464 from $435.

Tuesday: Mizuho reset its Palantir (PLTR) target at $185, while KeyBanc upped its target for Netflix (NFLX) to $115. Citigroup opened an “upside 90-day catalyst watch” on shares of Alphabet (GOOGL) and boosted its target to $405 from $390. BofA upped its Apple (AAPL) target by $5 to $325.

Wednesday: Oppenheimer boosted its Marvell (MRVL) target to $170 from $150.

Thursday: Piper Sandler and Truist raised their Bank of America (BAC) price targets to $59 and $61, respectively, from $53 and $57. TD Cowen trimmed its Microsoft (MSFT) target to $540 from $610 while JPMorgan took its Arista Networks (ANET) target to $200 from $190. Wells Fargo and Goldman Sachs lifted their Morgan Stanley (MS) targets to $200 and $205, but BofA and Barclays took theirs to $225 and $230. Baird upped its Waste Management (WM) target to $260 from $248, and Stifel increased its Marvell (MRVL) target to $140 from $120.

Friday: JPMorgan raised its Costco (COST) target price to $1,110 from $1,060. Piper Sandler raised its Netflix (NFLX) target to $115 from $103, JPMorgan reiterated its $118 target and Overweight rating, Needham did the same with its Buy rating and $120 target as did Morgan Stanley with its $115 target and Buy rating. Guggenheim lowered its price target on Netflix to $120 from $130 but kept its Buy rating on the shares. BNP Paribas upgraded Apple (AAPL) to Outperform from Neutral.

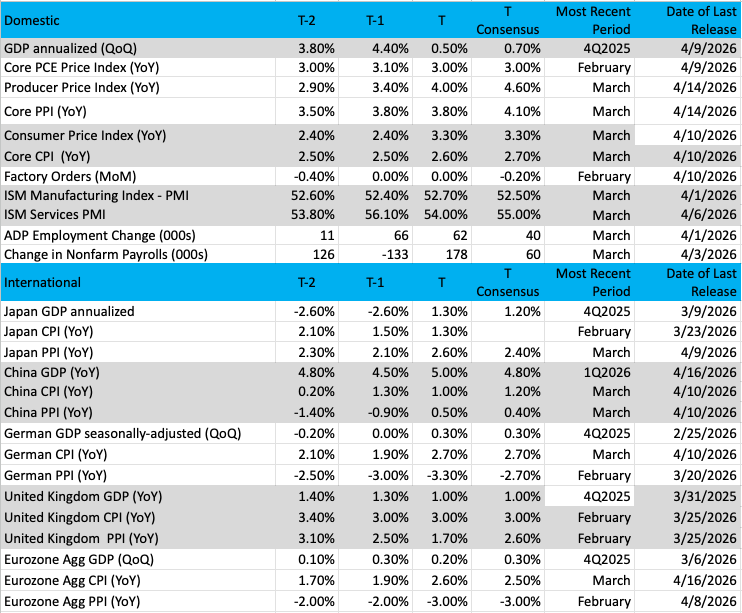

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading, and T-2 is two periods back, the intent being to illustrate any trends.)

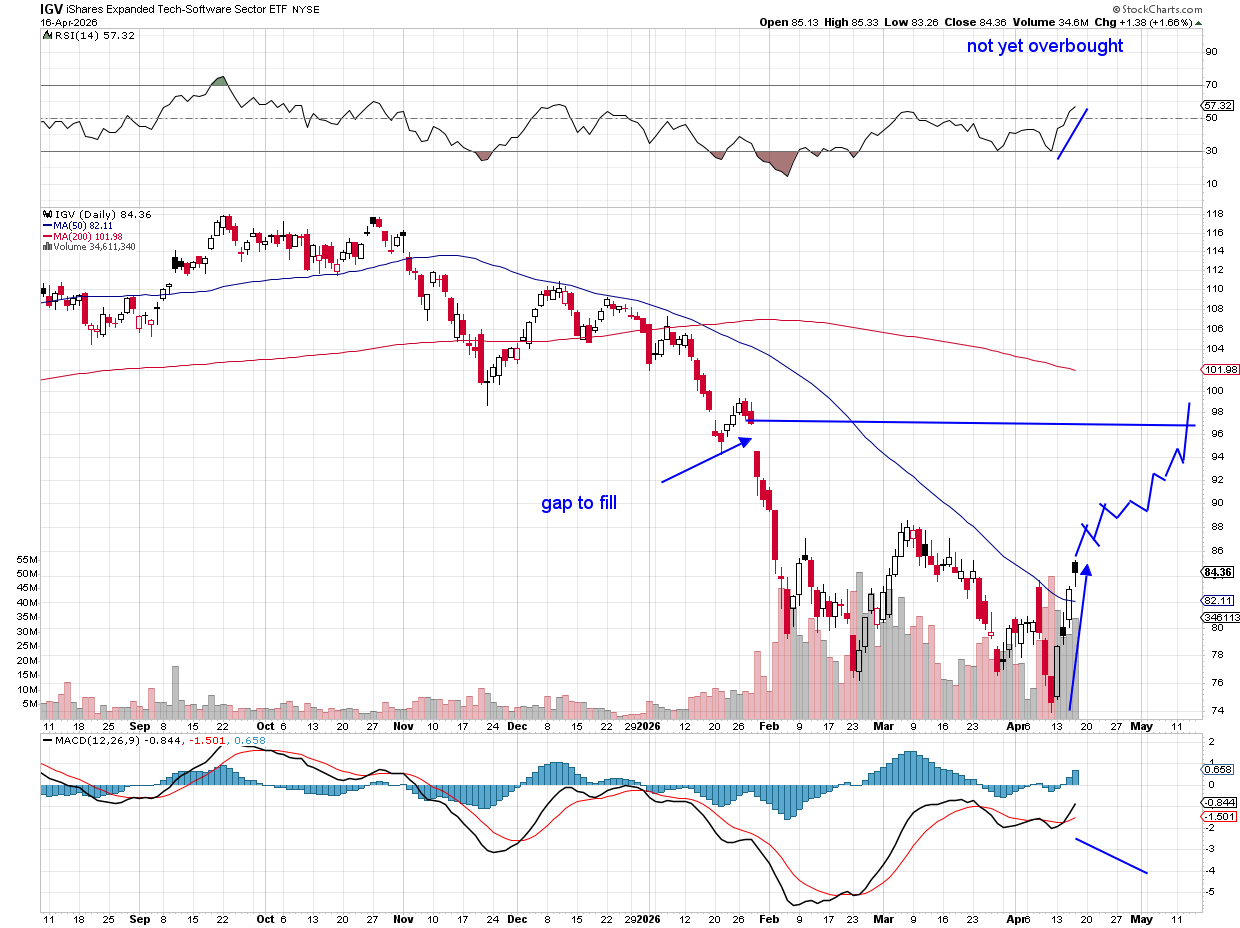

Chart of the Week: iShares Expanded Tech-Software Sector ETF

We are going to take another look at the software sector through the lens of the iShares Expanded Tech-Software Sector ETF (IGV) . We spoke about the difficulties this group was facing with a potential threat from AI and, even worse, "demand destruction." The question being, "Does a company need to invest in both AI and software/services if they are duplicates?”

It is a valid concern for big companies like Microsoft (MSFT) , ServiceNow (NOW) , Workday (WDAY) , Datadog (DDOG) , and Oracle (ORCL) . The investment in AI has become quite large across the spectrum and there just aren't enough dollars to spend for everything to be covered.

The investment community showed its discontent with software names and really took the IGV to the woodshed. Since peaking twice in fall 2025 at $118, the ETF took a sharp leg down, with lower highs and lower lows. You can see on the chart that the month of January was the worst, with a staggering decline of 14%. The selling continued in February and March, but it seems the bargain hunters are at it again this month.

While we are not calling a bottom here, it is fascinating to see the strength in this group over the last few sessions, led by Microsoft, Oracle, and some others. The chart is still bearish, but a close above that 50-day moving average (blue line) for the first time since October is very encouraging.

The question one asks is if 10 weeks of basing is enough. We’ll have to see, but the IGV is on a roll and not overbought here. Heavy resistance at $88 is dead ahead and will be a decision point (does the big money sell or continue buying?). Ultimately, if the chart turns bullish, the next objective would be the 200-day moving average at $102, a nice 20% gain from current levels.

Lastly, earnings will hit for many of these companies over the next few weeks. This group may have overshot to the downside as estimates were revised downward (happened several times since December). If a bit of good news appears, this group may start to perform better, and then we might have a strong rally on our hands.

Other charts we shared with you this week were:

Monday, April 13: S&P 500 - Bulls Make a Stand, But There Is an Issue

Monday, April 13: Hudbay Minerals (HBM) - This New Diplomat Is an Earnings Delight

Tuesday, April 14: Morgan Stanley (MS) - We're Banking on Morgan Stanley to Lead the Pack

Wednesday, April 15: Netflix (NFLX) - Netflix Soars After Walking Away From Warner Bros.

Thursday, April 16: SuRo Capital (SSSS) - Surging SuRo Capital Is Attracting More Attention

The Week Ahead

Over the weekend, we will be looking to see what developments emerge between the U.S. and Iran, and how they may shape expectations for firmer peace talks. Heading into the weekend, several issues between the two remain, including the subject of uranium enrichment. Based on how the market closed the trading week, it’s fair to say expectations are high, and what we learn will shape how we begin the upcoming trading week.

That’s especially the case given the lack of fresh economic data and a rather sparse earnings calendar on Monday. Tuesday will see the March Retail Sales report published, and while that will bring some nice context for Costco’s (COST) latest monthly sales report, we’ll be more focused on what is revealed in Thursday’s Flash PMI data from S&P Global. Activity in the manufacturing and service sectors, new order growth, job creation and inflation pressures remain a regular item on our punch list for that report. This time around, what the report reveals about how the U.S.-Iran conflict shaped the data, and how long that impact may last will be on our minds as well.

Here's a closer look at the economic data coming at us next week:

U.S.

Tuesday, April 21

ADP Employment Change Report – Weekly (8:15 AM ET)

Retail Sales – March (8:30 AM ET)

Business Inventories – February (10:00 AM ET)

Pending Home Sales – March (10:00 AM ET)

Wednesday, April 22

MBA Mortgage Applications Index – Weekly (7:00 AM ET)

EIA Crude Oil Inventories – Weekly (10:30 AM ET)

Thursday, April 23

Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

Chicago Fed National Activity Index – March (8:30 AM ET)

S&P Flash Manufacturing & Services PMI – April (9:45 AM ET)

EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, April 24

University of Michigan Consumer Sentiment Survey (Final) – April (10:00 AM ET)

International

Tuesday, April 21

Japan: Imports/Exports - March

UK: Employment Change, Unemployment Rate – February

Eurozone: ZEW Economic Sentiment Index - April

Wednesday, April 22

UK: Inflation Rate, Producer Price Index, Retail Price Index – March

Eurozone: Consumer Confidence (Flash) - April

Thursday, April 23

Japan: S&P Flash Manufacturing & Service PMI – April

Eurozone: S&P Flash Manufacturing & Service PMI – April

UK: S&P Flash Manufacturing & Service PMI - April

Friday, April 24

Japan: Inflation Rate - March

UK: Retail Sales - March

As we mentioned above, more than 90 S&P 500 companies will be reporting next week, and among them will be United Rentals (URI) and American Express (AXP) . Also, the SpaceX analyst day is on April 21, and that will be of keen interest to us given the pending IPO, but also the background it may provide on Amazon’s (AMZN) Amazon Leo project and its pending acquisition of Globalstar (GSTR).

Next week will be one of collecting data points and connecting them back to the Portfolio’s holdings, but we will also be closely tracking the market's reaction to quarterly results reported and guidance issued.

Here's a closer look at the earnings reports coming at us next week:

Monday, April 20

Open: Cleveland-Cliffs (CLF)

Close: Alaska Air (ALK), Steel Dynamics (STLD)

Tuesday, April 21

Open: 3M (MMM), DR Horton (DHI), Danaher (DHR), GE Aerospace (GE), Northrop Grumman (NOC), Quest Diagnostics (DGX), Synchrony Financial (SYF), United Health (UNH)

Close: Capital One (COF), Interactive Brokers (IBKR), United Airlines (UAL)

Wednesday, April 22

Open: AT&T (T), Boeing (BA), GE Vernova (GEV), NVR (NVR), Philip Morris International (PM)

Close: Crown Castle (CCI), CSX (CSX), IBM (IBM), Lam Research (LRCX), Las Vegas Sands (LVS), Tesla (TSLA), Texas Instruments (TXN), United Rentals (URI)

Thursday, April 23

Open: American Airlines (AAL), American Express (AXP), Dow (DOW), Helen of Troy (HELE), Honeywell (HON), Keurig Dr Pepper (KDP), Mobileye (MBLY), NextEra Energy (NEE), PulteGroup (PHM), SAP SE (SAP), STMicroelectronics (STM), Union Pacific (UNP)

Close: Ameriprise Financial (AMP), Digital Realty Trust (DLR), Intel (INTC)

Friday, April 24

Open: Charter Communications (CHTR), HCA (HCA), Norfolk Southern (NSC), Procter & Gamble (PG), Sensient (SXT)

Portfolio Investor Resource Guide

Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

Investing Terminology: 16 Key Terms Club Members Should Know

10-Ks: Want to Know About a Stock? Read the Company's Reports

10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

Income Statement: Our Cheat Sheet to Understanding This Financial Document

Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

Thematic Investing 101 Webinar

Like the Benefits of ETFs? Let’s Talk About Models

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.

Stocks & Markets Podcast Links

Some helpful links if you prefer to catch the podcast on the go, in the car, or wherever. Be sure to give it a like or thumbs up and leave a review if you’re so inclined. We’d appreciate it.